When Tamara Saeed and her husband were looking for a way to save for their children’s education a few years ago, the allure of Airbnb caught their eye.

The family bought a cottage near Grand Bend, Ont., in late 2019, with plans to host the property on the short-term rental platform. They almost second-guessed the move when the COVID-19 pandemic struck, but the waves of Canadians looking to escape the city during lockdowns proved a boon for the new cottage owners.

“It’s been great. I honestly enjoy hosting, it’s just a great way to help people explore an area they might not otherwise have access to. Not everyone can own a cottage,” Saeed tells Global News in an interview.

She recently doubled down and bought a second cottage property in Selkirk, Ont. and has also put it up on short-term rental sites including Airbnb and Vrbo.

But now, with bookings slowing down heading into the holidays, mortgage costs rising and a possible recession on the horizon, she’s wondering whether she might be forced to sell her rental properties.

“It was a great idea and I still think it is. But the fact is things have changed,” Saeed says.

She cites new taxes from municipalities and rising interest rates from the Bank of Canada as hurting the business case and earning potential for her cottage properties.

Inflation is also drawing down revenues amid higher costs for cleaners and maintenance crews who rely on the cottage industry.

“We are worried that with the cost of everything, it might not be as feasible to hang onto these properties. We’re hoping that’s not the case,” Saeed says.

But it’s not necessarily today’s circumstance that could settle her future in the short-term rental game.

While business always slows down after the busy summer months, Saeed says bookings have seen a greater slowdown so far this fall.

Mortgage costs for property owners relying on short-term rentals like Airbnb are soaring at a time when experts say travel demand is projected to slow ahead of a feared recession.

“It is a little scarier,” Saeed says.

“We’re just thinking of the future, really. If this trend continues, is this something that we just feasibly continue to do?”

‘Airbnbust’?

Saeed isn’t alone in fretting about headwinds for the short-term rental industry.

The term “Airbnbust” picked up steam online recently with Twitter and Facebook posts showing hosts complaining about declining occupancy rates.

Airbnb has reported strong revenue growth through much of the year as consumers have rushed back to travel following the lifting of COVID-19 restrictions.

Get weekly money news

But the San Francisco-based company’s share price took a hit last week — despite posting record profits — as it fell short of analyst expectations and said it expected booking growth to moderate over the holidays amid high global inflation.

Competitors Expedia, which owns short-term rental platform Vrbo, and Bookings.com both said in their filings last week that near-term “uncertainty” meant they couldn’t accurately forecast how many bookings they’d see over the fall.

Kiefer Van Mulligen, an economist with the Conference Board of Canada, tells Global News that “demand for travel will be reduced” in the months ahead as high inflation and interest rates eat at consumer spending power and fears about job losses on the horizon push households to save rather than splurge.

“That matters for the tourism industry recovery. If people aren’t spending as much money, then it’ll be a more gradual path back to kind of pre-pandemic levels,” he says.

Short-term rental hosts in some cities across Canada are already reporting fewer bookings in their calendars compared to this time last year, according to one analysis.

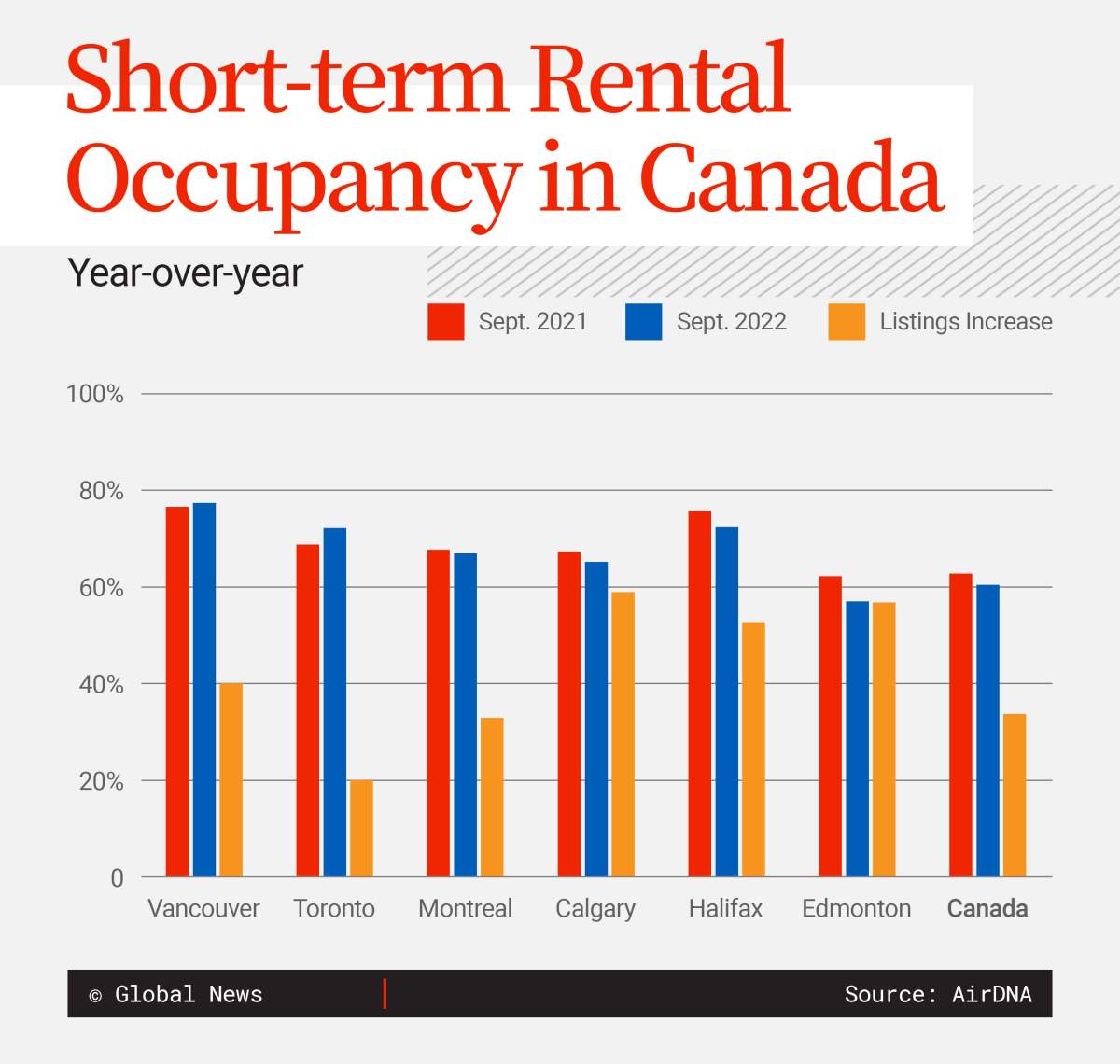

Data provided to Global News from AirDNA, a third-party company that tracks listings and occupancy of Airbnb and Vrbo units worldwide, shows that more hosts are joining the market in Canada to compete for travellers’ dollars even as demand is set to fall.

The number of available listings on the two platforms has risen year-over-year across the country and in six major markets tracked by AirDNA, but Vancouver and Toronto were the only ones included in the analysis that saw their occupancy rates increase over the same time.

Canada saw an overall 34 per cent bump in listings from September of this year compared to last, while the average occupancy rate dropped to 60.4 per cent, down 2.3 percentage points.

Edmonton, meanwhile, saw a 57 per cent jump in listings year-over-year, but recorded a five-percentage-point drop in occupancy over the same time.

AirDNA economist Bram Gallagher told Global News in an email that while the growth in short-term rental supply is still expected to outpace demand, the number of new units coming to the platform should also slow as rising interest rates discourage new investors from entering the market.

He also said that while today’s occupancy figures are falling off of 2021’s highs, those levels were “never sustainable.”

Rather than a bust, Gallagher said he sees the industry establishing a new “benchmark” after years of atypical trends in the pandemic.

For its part, Airbnb claims data about the platform’s bookings and occupancy can’t be reliably calculated by third parties.

The company also said in its earnings last week that overall demand from guests was rising last quarter, especially in cities.

“In one city alone – Toronto – we’ve seen a 60 per cent year-over-year growth in bookings over the last 12-months as of October 1, 2022,” the company said in a statement to Global News.

Airbnb is also rolling out new features early next year that will give hosts more insight into the fees guests pay and more options to discount and set competitive prices.

One feature rolling out widely on the platform, which shows users the total price they’ll pay as they’re exploring booking options, is already available in Canada.

- Major changes in store for Memorial Drive as part of east Calgary development

- Addiction experts say recent flood of gambling ads a problem for some Albertans

- Clinics, technicians unsure of Alberta’s new self-referral method for health tests

- Investors want ‘real proof’ AI spending is paying off, new report suggests

Rental mortgages more vulnerable as rates rise, expert says

New hosts are joining the platform today, Airbnb argues, as a way to earn extra cash and offset high inflation. A survey from Airbnb itself claimed that 44 per cent of Canadian hosts said the money they’ve earned through the platform has helped them stay in their homes as costs rise.

But homeowners who bought properties in order to rent them out on platforms like Airbnb could also be more at risk in today’s rising rate environment.

New and existing mortgage holders alike are set to feel the pain of rising interest rates, either when they purchase or renew their loans, but homeowners who take out a mortgage on a rental property are often more vulnerable to rate hikes, according to Shubha Dasgupta, CEO of Toronto-based brokerage Pineapple.

While standard residences can see an owner put down amounts like five or 10 per cent to buy a property, rental purchases must have a 20 per cent down payment on hand, raising upfront costs, Dasgupta notes.

Mortgages on rentals also tend to have higher interest rates, as lenders view these properties and the need to find tenants for cash flow as inherently more risky, he says.

This can push many landlords and short-term rental hosts to the alternative mortgage market to get qualified with more flexible loan conditions and shorter terms, Dasgupta says.

The result? Owners who rushed out to buy when interest rates were low over the pandemic are now finding themselves with much higher monthly costs on their properties.

“Clients that took like a one-year term, as an example, last year at lower interest rates, are going to be much more susceptible to higher interest rates today,” Dasgupta says.

Those with variable mortgages are also immediately paying more as the Bank of Canada raises interest rates. The central bank has increased its policy rate 3.5 percentage points so far this year and has signalled it’s not done yet.

Saeed says she has fixed rates on her home in Brantford, Ont. and her property near Grand Bend, but her Selkirk cottage is on a variable rate and she says payments have increased “exponentially” this year.

While she’s actively looking for solutions that can keep her long-term savings goals for her kids on track — a more traditional Registered Education Savings Plan is one she’s floated — she says she’s not feeling “oh, poor me” about her situation.

“There are many people who unfortunately have it a lot worse than we are, but we do feel the pinch. We’re not multimillionaire corporations. We’re just your average mom and pop just trying to get a little ahead and leave something for their kids,” she says.

There are a few options out there for short-term rental hosts like Saeed who want to hold on to their properties through the economic uncertainty.

Dasgupta says demand for long-term rentals is high right now in most Canadian housing markets, and extra units would be “welcomed” back into the stock.

He also says there’s a hybrid model that he’s seeing growing in popularity, dubbed “Airbnb arbitrage,” wherein an owner takes out a long-term tenant who continues to run the short-term rental on their own but takes on the burden of finding guests and running the day-to-day operations.

Alternatively, Dasgupta recommends reaching out to your mortgage agent or broker if you need a bit of flexibility on your payments. If you set up a plan pre-emptively, you can often extend the amortization period of the loan or set up a schedule to return to regular payments when your cash flow is back on track, he says.

For those hosts who are able to stretch their dollars and make it to the other side of the economic downturn, Gallagher said he expects short-term rental business will return when consumers feel they can take their vacations again.

“Yes, in a recession, people pull back on travel, but it’s short-lived, and they want to take their vacations: they won’t skip multiple vacations unless we’re in a deep recession and seeing long-term unemployment, which is not what most economists expect today,” he said.

Comments

Want to discuss? Please read our Commenting Policy first.