It’s been two years since the Bank of Canada started the most aggressive interest rate hike campaign in its history in a bid to tame rampant inflation, and the Canadian economy looks vastly different.

As the Bank of Canada delivered the first of what would be 10 interest rate hikes over the course of the tightening cycle on March 2, 2022, it flagged fresh concern about impacts from Russia’s unprovoked invasion of Ukraine, a conflict that was barely a week old at that point.

A central bank statement at the time noted the economy’s roaring recovery from the COVID-19 Omicron variant shutdowns and fears of what new mutations to the virus could bring.

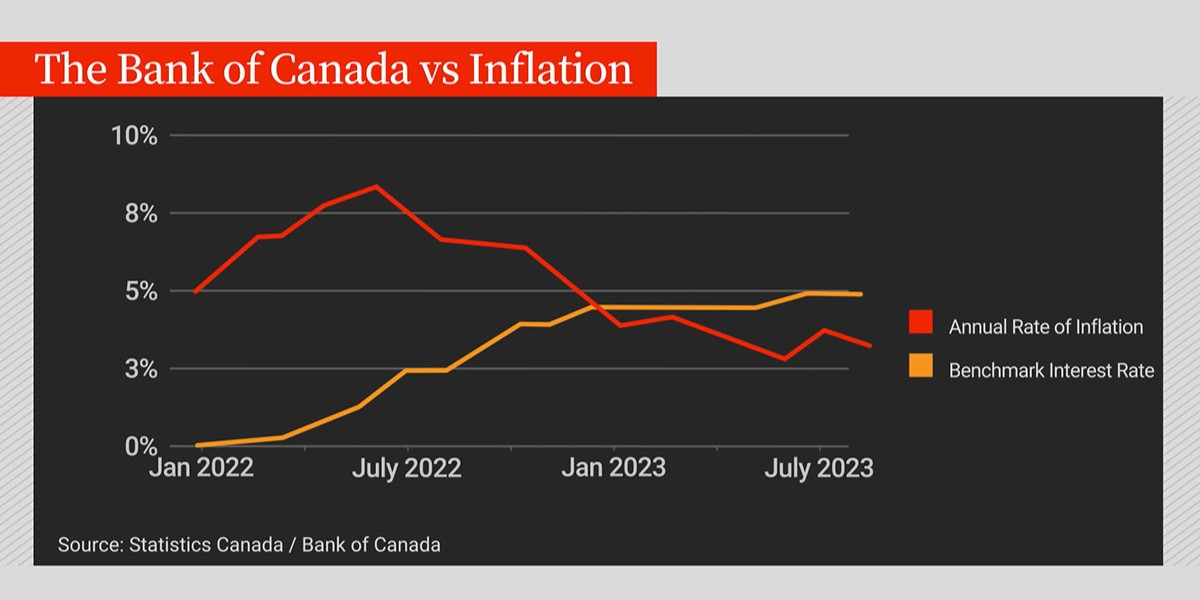

And as inflation was accelerating – it would rise from 5.1 per cent at the start of 2022 to a 41-year peak of 8.1 per cent in half a year – prices in Canada’s housing markets had hit an all-time high ahead of pronounced correction.

The substantial cooling of the economy has come thanks in part to the 4.75 percentage points of hikes to the Bank of Canada’s policy rate, which stands at 5.0 per cent.

Ahead of the Bank of Canada’s next rate decision on March 6 and on the second anniversary of the first rate hike of the cycle, Global News spoke to economists about what’s changed since the tightening began and where the central bank’s quest to tame inflation goes next.

While efforts to restore price stability without crashing the economy have largely been successful, experts – and the Bank of Canada’s top policymakers themselves – concede that the tightening cycle has not been perfect.

Inflation underestimated

Two years since the Bank of Canada’s initial 25-basis-point interest rate hike, inflation has cooled significantly. The annual rate of inflation last clocked in at 2.9 per cent in January, and the central bank’s latest forecasts have price pressures cooling back to the two per cent target sometime in 2025.

Those projections have been off-base in the past.

Think back to the summer of 2021, when the global economy was recovering from COVID-19 shutdowns and fervent consumer demand led to supply chain snarls that drove up prices on cars and other goods.

“We expect the factors pushing up inflation to be temporary, but their persistence and magnitude are uncertain, and we will be watching them closely,” Bank of Canada governor Tiff Macklem said that July as he laid out the central bank’s forecasts.

At that time, the bank expected inflation would ease back to the two per cent target sometime in 2022 and maintained its commitment to Canadians that it would keep interest rates at rock-bottom lows in a bid to boost the pandemic recovery.

There were a few things that the Bank of Canada couldn’t have predicted then: global shortages of critical inputs like semiconductors, Russia’s invasion of Ukraine and the impact of future COVID-19 variants, to name a few.

But Stephen Brown, deputy chief North America economist at Capital Economics, says it’s clear today that the Bank of Canada underestimated inflation in the early going and waited too long to start its hiking cycle.

“It should have started six months earlier, to be honest. That was when inflation was picking up,” he tells Global News.

Avery Shenfeld, chief economist at CIBC, tells Global News that the strength of inflation globally in this cycle caught many central banks by surprise.

“We knew that some of it was caused by supply chain disruptions (and) the war in Ukraine. But perhaps it was a little too much confidence that all of that would disappear on its own accord,” he says.

Had the Bank of Canada started its hiking cycle earlier, it’s possible the benchmark interest rate would not have needed to rise quite so high to effectively tame inflation, Shenfeld adds.

“But I think it’s fair to say that that same mistake was made by central banks around the world,” he says.

Criticisms that the Bank of Canada waited too long to raise the low interest rates that stimulated the economy during the pandemic are not controversial today – even Macklem agrees.

He acknowledged that, with the benefit of hindsight, the central bank was indeed slow to start raising interest rates in an appearance before the House of Commons finance committee in late 2022.

“If we knew everything a year ago that we knew today, yes I think we should have started tightening interest rates sooner to withdraw the stimulus,” he told MPs at the time, adding that stimulus was “an important factor that generated a very strong recovery.”

Housing market fluctuations

One of the starkest differences in the Canadian economy since the start of the tightening cycle is the strength of the housing market.

In the first two years of the COVID-19 pandemic, the Bank of Canada’s rock-bottom interest rates offered buyers cheap access to financing, helping to spur a monumental run in the housing market.

That peaked in February 2022, just before the tightening cycle began, with the Canadian Real Estate Association saying the average price of a home hit the all-time high of $816,720. The most recent CREA data for January of this year shows average home prices have fallen to $659,395, a decline of 19 per cent.

CREA’s home price index, a more like-for-like property comparison, shows an overall price drop of 12.1 per cent between January 2022 and 2024 across the country.

But the housing correction has not been linear. This time a year ago, the market was heating up amid a “conditional pause” in the Bank of Canada’s rate hike cycle as the central bank waited to see whether it had raised interest rates enough to tame inflation.

Brown says the run-up in housing market activity last spring sent prices shooting back up another 10 per cent or so before the Bank of Canada returned to the hiking table with a pair of back-to-back increases of a quarter-percentage point in June and July.

“I think the real surprise was the extent of that rebound,” he says.

But Shenfeld says it’s even “debatable” whether those two so-called insurance hikes were really necessary.

When the Bank of Canada came off the sidelines in June, it was responding to strong economic data from the first quarter of 2023, he says. That proved to be a “one-quarter wonder,” he says, and the economy was in fact already starting to slow amid lagged impacts from previous rate hikes before the 50 basis points of additional tightening.

Shenfeld says he doesn’t think an extra half-percentage point on the policy rate did “tremendous harm,” with the economy still proving resilient today. He says it’s even possible that the extra tightening will mean the Bank of Canada can pivot to rate cuts sooner than if it had left the policy rate at 4.5 per cent – a scenario monetary policymakers have also pitched during the cycle as “front-loading” rate hikes.

Economic strength holds up

While inflation and higher interest rates have stung many Canadians, particularly the most vulnerable, Shenfeld says households in general are holding up well in the face of tougher economic conditions.

Homeowners who have had to renew their mortgages in the higher interest rate environment have largely been able to find extra money to make those payments so far. Shenfeld cites this a significant reason why “prices haven’t plunged” in the housing market, with owners not forced to sell their homes en masse.

The households that took out the cheapest fixed mortgages on five-year terms in 2020 and 2021 have yet to face the renewal shock, he notes, and may skirt the worst of it if the policy rate drops before their contracts are up.

The latest real gross domestic product (GDP) data from Statistics Canada on Thursday shows that the country has, at least so far, avoided falling into a recession.

Brown says that’s a remarkable feat, given the growing chorus of forecasters this time last year who were expecting the Canadian economy to tip into recession under the weight of higher interest rates.

He says the Bank of Canada “got lucky” with a boost in population during the tightening cycle as processing the backlog of visa applications from the pandemic brought a surge of newcomers into the country, helping to keep the economy from a more severe downturn. But he also offers the central bank kudos for a job well-done to date.

“It appears we’ve achieved a soft landing and inflation will be heading back to two per cent by the end of this year,” Brown says. “So it’s certainly performed quite well on any objective scorecard.”

Much of the relief in inflation has come from the unclogging of supply chains that drove the initial spike in prices two years ago, Shenfeld says. But he also adds that higher interest rates have helped to relieve some of the tightness in the labour market, alleviating inflationary pressures.

Shenfeld also says the Bank of Canada did a “reasonably good job” taming inflation, which historically has required a “big recession” to put the lid back on price growth.

“They would certainly get no worse than a B-plus. Maybe if they’d started a little earlier, we’d be giving them an A,” he says.

But Shenfeld also notes that we’ll have to see how the central bank sticks the landing before handing out final grades.

Where do inflation and the policy rate go from here?

Where the cost of living continues to pinch Canadians most of all is on the shelter side of inflation, Brown notes, with higher mortgage payments and climbing rents continuing to put pressure.

Shelter inflation accelerated in the latest reading from StatCan, up to 6.2 per cent in January from 6.0 per cent the month earlier.

But Brown says that without the impact of mortgage interest costs – tied to the Bank of Canada’s own higher policy rate – inflation would already be back at the two per cent target.

“It just shows you that the bank’s job really is done on everything else. We’re not seeing much in the way of inflation pressures elsewhere,” he says.

Brown forecasts shelter inflation will cool meaningfully by 2025 amid expectations that immigration will slow from the record highs of previous years, taking some of the pressure off rents.

The Bank of Canada has maintained that it expects inflation to return to its two per cent target next year. Conversations at the central bank have started to shift from whether the policy rate is high enough to how long it needs to remain elevated before policymakers can consider cuts.

Macklem has said the Bank of Canada is looking for confidence that inflation will continue to decline all the way back to target, but he said annual inflation doesn’t have to be at exactly two per cent before the central bank can consider lowering the policy rate.

Despite January inflation figures coming in well below expectations, the Bank of Canada is widely expected to hold rates steady at its upcoming decision on March 6.

- As Canada’s tax deadline nears, what happens if you don’t file your return?

- Do you need to own a home to be wealthy in Canada? How renters can get ahead

- Posters promoting ‘Steal From Loblaws Day’ are circulating. How did we get here?

- Investing tax refunds is low priority for Canadians amid high cost of living: poll

After Thursday’s GDP print showed weak but still positive growth in the economy, most big bank forecasters have called for interest rate cuts to begin in June, though some projections still have an April cut in the cards and others see July as more likely.

When the easing cycle does begin, Macklem has warned Canadians that the days of ultra-low interest rates seen during and before the COVID-19 pandemic are not likely to return.

Brown and Shenfeld say the Bank of Canada is likely to deliver roughly two percentage points of cuts in the years ahead before holding at a “neutral rate” of around three per cent at the end of the cycle.

For Canadians seeing the economy slow around them and anxiously awaiting interest rate cuts, Shenfeld advises patience. Two years in, the Bank of Canada’s tightening cycle has come a long way, but it’s not over yet.

“First, the economy slows, the unemployment rate moves up a little bit, and the lower inflation is the reward that comes last in that process,” he says.

“We don’t want to conclude that it’s not working because we don’t yet have two per cent inflation. It’s just going to take a little longer to get there.”

Comments