Graham Isador says it feels strange to think about himself as one of the “lucky ones” in Toronto’s notoriously unaffordable housing market.

The 35-year-old freelance writer is a renter, and pays just under $2,000 for a two-bedroom apartment in the city’s downtown core. That’s well below the market rates his friends in the neighbourhood are paying, Isador says.

It’s a relatively affordable apartment, but it’s also become something like a pair of “golden handcuffs,” he tells Global News.

Isador says he’s only been able to hold on to a steady rate of rent because he’s been in the same unit for the past six years. But paying for that apartment on his own is already eating up a “pretty big portion” of his monthly expenses, and the prospect of having to move and probably see those payments spike hundreds of dollars fills him with a certain dread.

“The biggest thing that characterizes my relationship with renting is just a nervousness that what I have right now won’t last forever or might go away,” Isador says.

That anxiety comes as the cost-of-living crisis appears to be getting more bleak for young Canadians, with groceries and housing becoming more expensive in the past year.

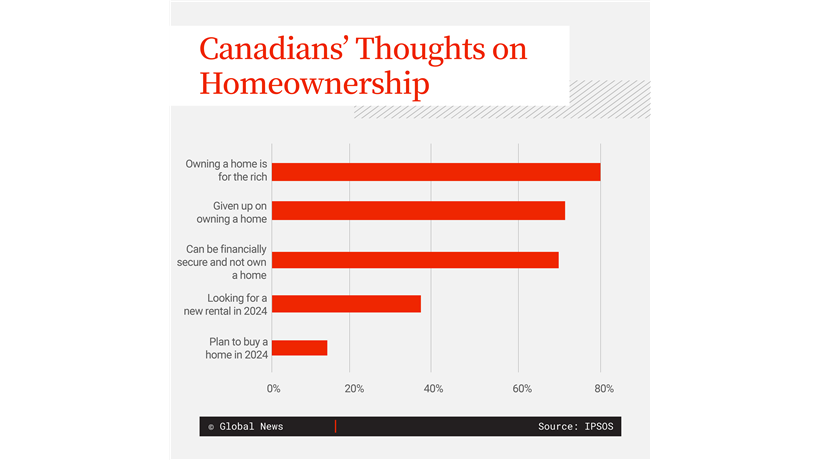

Recent Ipsos polling conducted exclusively for Global News shows that while owning a home feels further out of reach, more Canadians feel it’s important for their financial security.

According to the polling released Friday, 71 per cent of respondents said they felt it’s possible to be financially secure without owning a home, but that figure is down nine percentage points from a similar survey in March 2023.

Some 72 per cent of non-owners said they’ve “given up” on ever being able to afford a home, while 80 per cent said home ownership was now a privilege reserved for the rich.

Isador says that while he’d like to buy a home one day and he’s been able to put aside savings on a monthly basis, it “doesn’t begin to approach” what he’d need for a down payment in Toronto.

“I’ve been grateful to be able to stay in this apartment, but I’ve also contributed a significant amount of money into the equity of this house, which isn’t something that’s going towards my future,” he says.

The idea that owning a home and paying down a mortgage to build equity is a common strategy for Canadians looking to grow their wealth, says Jason Heath, managing director of Objective Financial Partners.

Buying a home can act as a “forced savings” tool in that way, he explains, whereas renters have to be more deliberate about putting away extra money every month on top of their rent.

But Heath also disagrees that living as a renter is any less financially viable than owning a home just because those monthly rent payments don’t go towards an individual’s own savings.

“I genuinely think that in some circumstances, a renter, particularly if they’re diligent with their saving, can come out ahead of a homeowner in the long run, financially,” Heath says.

Home ownership comes with unexpected costs

Heath says there’s a “recency bias” to discussions around home ownership as the value of real estate has largely surged over the past two decades.

Get weekly money news

But he warns that, taking a wider historic view of housing markets including and beyond Canada, home prices have tended to appreciate in line with wages – a trend that domestic values have largely outpaced in recent decades.

There’s simply no guarantee that home prices will continue to appreciate unabated in the coming years, which adds to the risk for homeowners who are banking on rising property values to grow their wealth, he argues.

“Anyone that’s counting on their home appreciating at a 10 per cent rate of return and downsizing and using it to fund their retirement, I’d be hesitant to think that’ll happen over the next generation,” he says.

Owning one’s home has often been a “fallback” for Canadians building their wealth, says Allan Small, senior investment adviser with the Allan Small Financial Group, part of iA Private Wealth. The proceeds from disposing of a principal residence in Canada are exempt from capital gains taxes, providing an advantage to homeowners when or if they choose to sell.

But Small, too, cautions clients who are planning for retirement about what wealth tied to the real estate market can do for them.

Costs in retirement can vary based on whether someone is renting or buying again after selling their home, he says. In the case of downsizing, someone selling a home that’s jumped in value could similarly end up buying something else that’s also surged in price – limiting the net return on the sale.

Rather than rely on the equity from home ownership, he advises thinking of rising home values as the “gravy on top” of a wealth-building strategy and relying on other savings and investments to fund the bulk of a retirement plan.

“I think if you look at it that way, I think you’ll be in better shape,” he says.

Small says many clients opt to become renters again after selling off their family home, keeping the proceeds of the sale liquid or reinvesting them and enjoying the lower monthly costs that typically come with a renter’s lifestyle.

Heath says that some Canadians who are renting today but aspiring to buy a home might underestimate the costs that come with home ownership.

Home insurance, property taxes, repairs and maintenance all become ongoing costs on top of the mortgage, he notes, which could well push monthly expenses for owners past those of renters.

For homeowners, that can mark an opportunity cost – money going towards the upkeep of a home that could otherwise be put into investments and come back at a higher return, Heath explains.

Isador agrees that if he did have a mortgage right now, he’d likely be paying more every month – not to mention on a smaller unit in a less desirable part of the city.

But as a renter for half his life, he says it’s only in the past five years or so that he’s gotten to a point where he has money left over at the end of the month to put towards longer-term savings. And knowing how to grow wealth as a renter isn’t always as straightforward as it is for homeowners, he says.

“That means trying to navigate markets that I don’t really understand as well, that are more complicated than just putting money into your house each month,” Isador says.

How to save and invest as a renter

For renters who do have money to save, Heath and Small say there are plenty of strategies to grow wealth outside the housing market.

“I think if somebody is a disciplined saver, they by all means can be a wealthy renter as well,” Heath says.

Without the forced savings of home ownership, renters have to be “consistent” about saving each month, Heath says, and need to choose the appropriate investment vehicles for them.

Canadians can open a registered retirement savings plan (RRSP) to benefit from income tax deferrals on contributions, which Heath says is ideal for individuals who currently have a high income.

A tax-free savings account (TFSA) is another option to shelter investments from tax at withdrawal; Heath argues this is best suited for early-career individuals who get less benefit from deferring income taxes.

He adds that the new first home savings account (FHSA), which allows Canadians to save and invest tax-free towards the purchase of their first property, isn’t just for prospective homeowners.

The FHSA allows for $8,000 in tax-deductible contributions annually, which are also tax-free on withdrawal when put towards a down payment, to a maximum of $40,000 over a lifetime. But if, after 15 years of saving, an individual doesn’t use the funds in an FHSA to purchase a home, the account must be closed and the money can be transferred into an RRSP as a “backdoor” strategy to maximize contribution room in the account, Heath notes.

“Even if somebody might never purchase a home, the new first home savings account could have a place in their savings strategy,” he says.

But what you do with that money once it’s inside a registered account is also critical, Small says.

Bond markets, high-interest savings accounts and fixed-income products like guaranteed investment certificates are suitable for more conservative investors or individuals with a shorter time frame to invest, he says. But Small says that particularly for younger Canadians who have a longer horizon to build their wealth, taking on some of the higher risk in the stock market is an important strategy.

Equity markets can be intimidating when viewed on a year-to-year or stock-to-stock basis, but Small notes that volatility smooths out over a longer horizon and indices such as the S&P 500 have trended towards growth over the long term.

“The odds are definitely in the investor’s favour. If you own good quality (companies) and you’re patient, you will make money,” he says.

That doesn’t mean a renter has to take on the riskiest positions to make money. Small says that a balanced portfolio can include reliable performers like banks or utilities, whose stocks also pay out dividends that can supplement a renter’s income and help pay down their monthly costs.

Socking away whatever money is available to start out in the markets and supplementing some dividend-paying stocks with one or two well-known high-tech names has the makings of a “diversified portfolio” that can pay off for a renter in the long term, Small says.

“The stock market builds wealth over time. And I think if you don’t have that real estate you definitely should be focusing on the investment markets,” he says.

Heath says the societal focus on achieving home ownership as a marker of financial success can be misguided.

It’s true that homeowners get “peace of mind” from owning their property while renters have to contend with renovations, evictions or other landlord decisions that can affect their living situation, he says.

But with today’s higher interest rates pushing mortgage costs higher, the surprises of sudden repairs and other fluctuations in the ownership market, Heath argues homeowners have no guarantee that their finances are going to be any more stable than a renter in a given year.

“It’s not a one-size-fits-all thing where it’s always bad to rent or you should always own or condos are bad investments. You need to look at the specifics of the situation,” he says. “And in certain markets and in certain situations, it’s very much a renter’s market.”

– with files from Global News’ Anne Gaviola

Comments