After years of frenzy in Canada’s housing market during the COVID-19 pandemic, 2022 saw a reversal across much of the industry as the Bank of Canada’s interest rate hikes cooled down the residential real estate sector in cities from coast to coast.

Most economists and experts who spoke to Global News say they expect that cooling to continue into 2023, citing prohibitively high mortgage rates, low inventory on the market and uncertainty about where the Bank of Canada’s interest rate cycle will finally peak.

Read more: Bank of Canada ‘still prepared to be forceful’ on interest rates if needed, official says

But where will price declines in the Canadian housing sector bottom out? And will all markets and property classes be hit evenly?

Here are the housing trends and markets to keep an eye on in 2023, according to industry experts.

Where will prices bottom out?

The latest available data from the Canadian Real Estate Association (CREA) shows that, on a seasonally adjusted basis, home prices in Canada fell 19 per cent from the peak in February to November, when the average sale price was $636,838.

When will the bottom come? RBC’s assistant chief economist Robert Hogue said in a note on Dec. 19 that he believes, with the slowing pace of decline in both home sales and prices, there are “early signs the correction is approaching its final stage.”

He said prices could eventually hit a low point in “the early part of 2023,” but cautioned the timing would vary from market to market.

Hogue suggested this bottoming out would coincide with the Bank of Canada stabilizing its benchmark interest rate — the central bank signalled in December it could be near the end of its hiking cycle — and that for those looking to break into the market, this might be where affordability is best in the year for prospective buyers.

While the spring may mark a low point for prices, Canadian brokerages are not expecting significant shifts between 2022 and 2023.

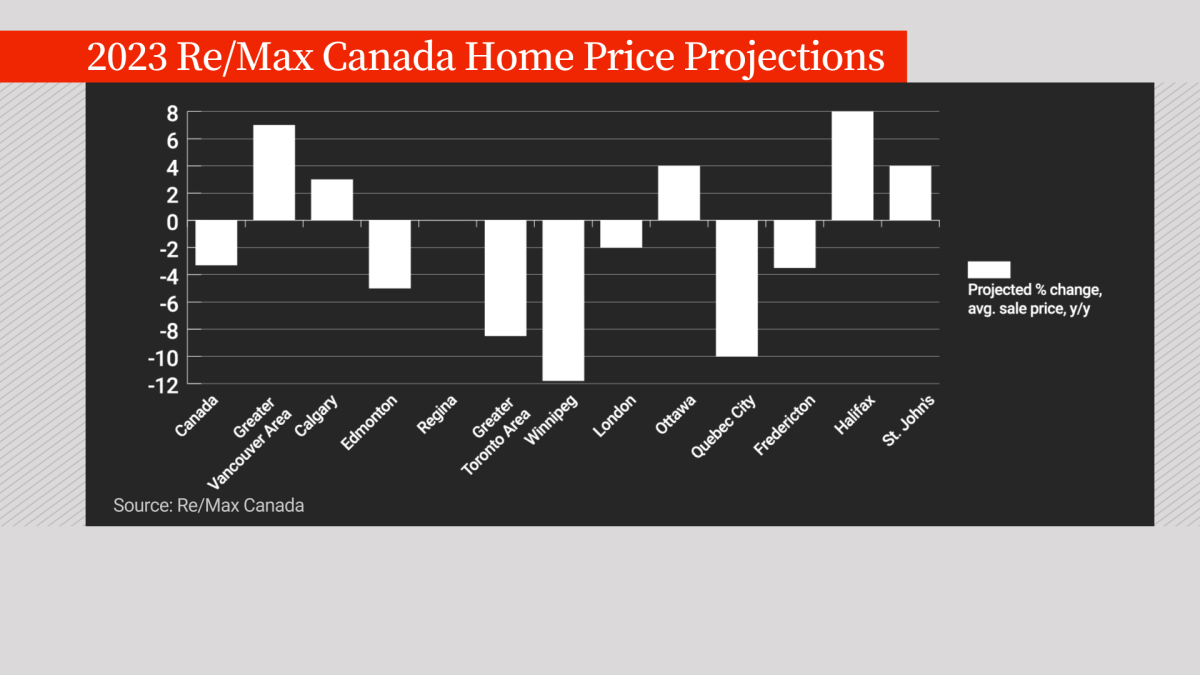

Re/Max Canada said in its housing outlook for 2023 that the aggregate price of a home is expected to drop 3.3 per cent in the year, while Royal LePage’s annual survey forecast a price drop of just one per cent.

Chris Alexander, president of Re/Max Canada, told Global News in late November that the Bank of Canada’s interest rates are the “big wild card” that will determine when buyers and sellers alike are comfortable jumping back into the market.

Some housing markets could see price growth

Some cities in Ontario are especially vulnerable heading into 2023, Re/Max projects, with steeper price drops expected for the Greater Toronto Area (11.8 per cent lower), Barrie (15 per cent lower) and Durham (10 per cent lower).

Parts of British Columbia are also expected to see declines, such as Greater Vancouver (five per cent lower), Kelowna (down 10 per cent) and Nanaimo (also down 10 per cent).

But some pockets of the country are set for growth in 2023, Re/Max forecasts.

Get weekly money news

Re/Max expects prices to rise in cities including Halifax (up eight per cent), Calgary (up seven per cent), Ottawa and Kingston, Ont. (up four per cent), St. John’s, N.L. (up four per cent) and Saskatoon (up three per cent).

Corinne Lyall, owner and broker for Royal LePage Benchmark in Calgary, says one of the reasons the city is set to do well in 2023 is that it didn’t see the dramatic run-up in prices over the pandemic that markets in B.C. and Ontario did.

With Calgary seeing only modest growth during that time, it’s become a more affordable option for people originally living in the more expensive provinces who are now able to work from anywhere and can purchase bigger houses for less money, Lyall says.

The benchmark cost of a single detached home in Calgary in November was $630,236, according to the local real estate board, nearly a third of the $1.86-million price tag on the benchmark detached home in Vancouver.

“Our price point is so much less for a major city,” Lyall says. “You can buy twice as much house here.”

Heading into a period of economic uncertainty, the Alberta market is also buoyed by recent strength in the oil and gas sector, Lyall adds. She believes the backdrop of the traditional energy industry, boosted by Calgary’s efforts to diversify into a tech hub in recent years, sets the city up as an attractive prospect for Canadians looking to relocate.

“I think people are still looking here as a place of opportunity,” she says.

Condos, urban centres expected to hold up well

Another part of the Canadian market primed to hold up in 2023 are condos and properties in urban cores, according to experts who spoke to Global News.

John Pasalis, president of Realosophy Realty in Toronto, says that, like Calgary, condos and downtown properties didn’t see major price inflation during the pandemic, and therefore have further to fall as the market cools.

In addition, the return to the office amid a lifting of COVID-19 restrictions is reversing the migration flows from the early days of the pandemic, when remote work enabled many to afford larger homes in suburban neighbourhoods on city outskirts and more rural areas.

- Alberta government expects $100 payouts to arrive within 2 weeks of applications

- Alberta giving $100 energy rebates to some households — is yours one of them?

- SpaceX rockets past Amazon to become world’s 5th most valuable company

- Benefit payments are coming soon to those who qualify. Here’s how much

Read more: Ontario, B.C. headed for buyer’s market despite high interest rates, RBC housing report says

“People thought this urban exodus during COVID was going to be permanent and no one would want to live downtown,” Pasalis says. “Well, that’s not happening. People are moving back to the city. They want to be kind of closer to downtown. So I suspect that market in the core will be a little bit busier.”

Nasma Ali, broker and founder of OneGroup in Toronto, says that with borrowing costs at their highest point in years, cheaper condos will be especially “desirable” in otherwise expensive markets.

“For a first-time homebuyer who’s in Toronto, the most affordable asset class is a condo,” she says.

In Calgary, Lyall says the push for condos is already on. Three years ago, she says the condo market was sitting at eight months’ worth of inventory, but heading into 2023, that’s already down to two months’ worth.

“That is the fastest growing market segment in terms of price right now and in terms of sales, it’s leading the way and we haven’t seen that for a long time.”

Pre-construction buyers showing 'some distress'

The pain of higher interest rates could hit the pre-construction market especially hard in 2023, some experts warn.

Ali says that for buyers who put money down on a home in 2020, when interest rates were low, the bar for qualifying for a mortgage is much higher after the Bank of Canada’s rapid hikes in 2022. Some of these buyers locked in their purchase at high pandemic prices and haven’t benefited from the recent cooling, she notes, and are now forced to pay peak prices at much higher interest rates.

With those homes coming up for completion in the year ahead, these buyers will be forced into difficult positions, Ali says. Some could be forced to come up with extra money to cover a home that wasn’t appraised for the mortgage they needed, or they may not be able to afford the monthly mortgage on the property with today’s higher rates, she explains.

These buyers may have to assign their sale if they can or sell at a steep loss, Ali says.

“If the dominoes fall, usually what this means is that we’re going to see finally many listings hit the market,” she says.

Pasalis agrees that the pre-construction market is looking vulnerable heading into 2023.

Prospective buyers could even find a deal if an investor is desperate to unload their pre-construction condo, he says.

“We’re starting to see some distress among pre-construction condo investors,” he says.

“There could be some opportunities as a buyer to get some value because that is the segment of the condo market where there’s a little bit more pressure.”

These units are not listed on traditional multiple listings services, however, so Pasalis says that anyone keen to scoop up a unit as it comes up for completion will have to search a little more carefully or go direct to the source in their new year housing hunts.

— with files from Global News’ Anne Gaviola and Rachel Gilmore

Comments

Want to discuss? Please read our Commenting Policy first.