A new analysis, commissioned by a group fighting real estate taxes implemented by B.C.’s NDP government, estimates Metro Vancouver shed nearly $90 billion in home value in 2018.

The analysis was commissioned by the anti-speculation tax and anti-school tax group StepUp Now, and was conducted by tax agent Paul Sullivan with Burgess, Cawley, Sullivan and Associates.

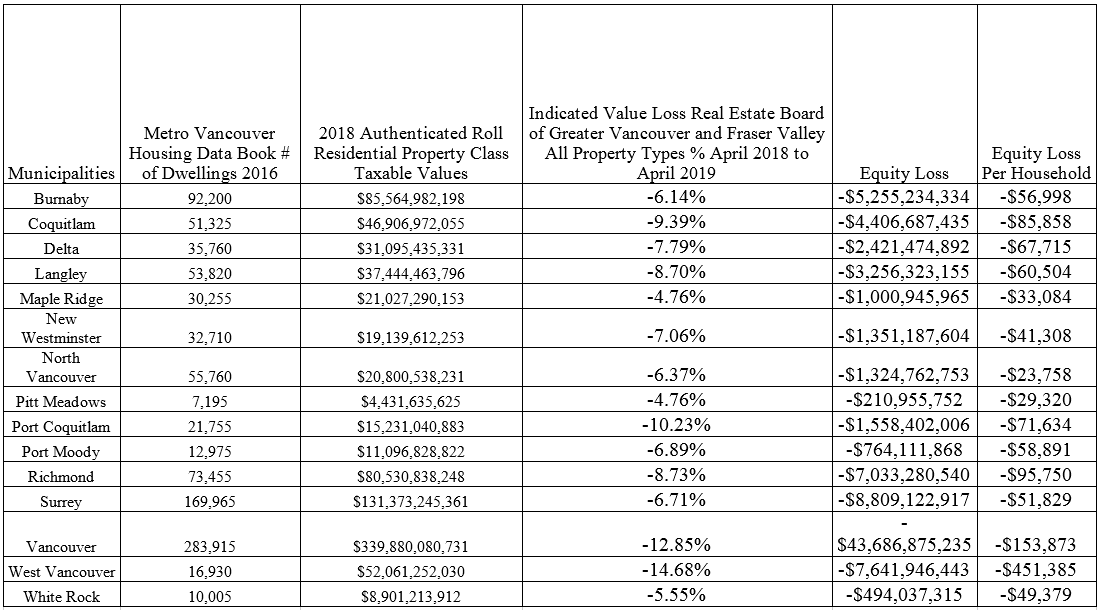

Sullivan found West Vancouver saw the biggest dip in values on a percentage basis, with a 14 per cent drop. The City of Vancouver, meanwhile, saw the biggest drop in total dollar value at $43.6 billion.

Sullivan argued that the decrease in home values is harming seniors who are relying on home equity for retirement, while potentially contributing to an economic slowdown.

WATCH: Buyer’s market as some Metro Vancouver condo prices coming down

And he rejected the assertion that the decrease in value amounts to nothing more than a loss on paper.

“That imaginary money is also people’s savings. It’s their investment in their property and that lift is the expectation you have when you put your investment, your income into a piece of real estate. These are people who aren’t putting their money into RRSPs or pension plans, they have homes.

“It’s not very imaginary when you walk into the bank and you have to refinance, and you say to the bank, ‘I put down 10 per cent when I bought this condo,’ and they say, ‘Well it’s appraising at less than what you put into it.'”

He said the decreases are also penalizing young homebuyers who recently got into the market.

“To gut a generation of their wealth — and I’m talking about all the young families who have bought homes in the last five years under the guise of affordability — and not build homes seems like a very, very unfair outcome.”

Get daily National news

StepUp Now, which was holding a rally against the speculation and school taxes on Tuesday, is arguing those taxes are the anchor dragging prices down.

READ MORE: Lower Mainland real estate cooldown continues as sales drop 42% below 10-year average

Economist Tom Davidoff with UBC’s Sauder School of Business said there’s no disputing prices have begun to fall, and that it is affecting owners’ equity.

But he said taxes aren’t the only possible reason for declines, noting the cyclical nature of real estate markets and the federal government’s new mortgage stress test — a measure the Real Estate Board of Greater Vancouver has argued is key to the softening market.

WATCH: Metro Vancouver housing sales fall to 33 year low

He also noted that while homeowners did see declines in 2018, it came after an unprecedented run-up in prices in the preceding years.

“Homeowners, of course, have done phenomenally well over the last decade. So, you know, if you bought your home 10 years ago you’re in great shape, financially,” he said.

“There are some new taxes on the $3 million-plus homes and for people who don’t make a living here. But even, net of course of a small tax increase, anybody who bought long ago is still doing very, very well.”

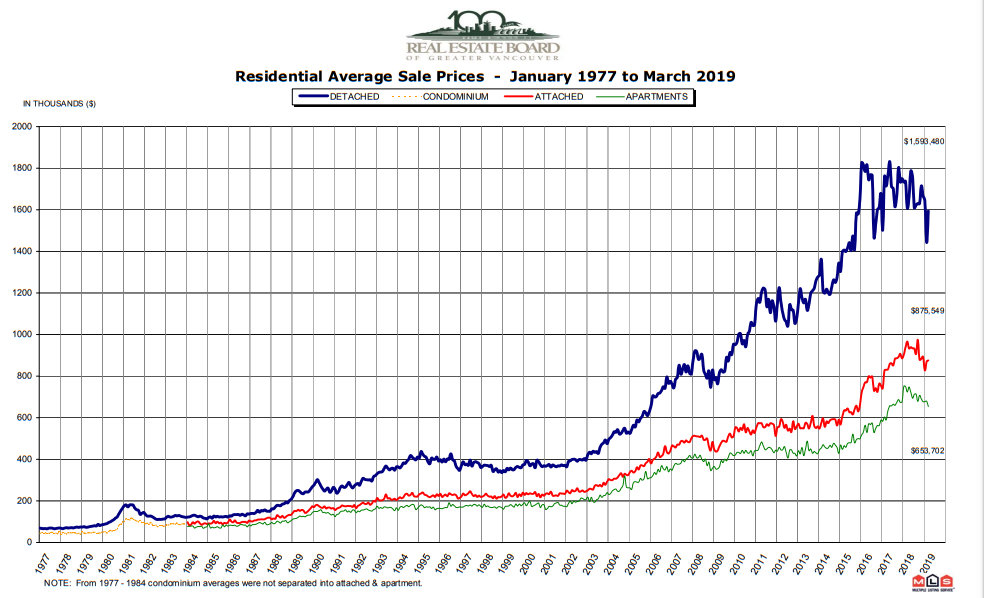

According to the latest data from the REBGV, the benchmark price of a detached home across the region has dipped roughly to the point at which it stood in 2016.

Davidoff said buyers who purchased a luxury home around that time are the biggest losers under the current market condition, though noted the situation for condo buyers from mid-2018 is also “starting to look not great.”

He added that renters and other people who felt locked out of the rapidly-appreciating housing market before 2018 are also likely to be pleased with the softening market.

“The challenge for the NDP going forward is, you know, can you stabilize a market with something like a 10 to 20 per cent decline,” Davidoff said.

“I don’t think anybody wants to see the dislocation you’d have both in terms of homeowner equity but also the general job market if we had a massive price decline.”

Comments

Want to discuss? Please read our Commenting Policy first.