Home borrowing took a “significant” hit in Vancouver after B.C. introduced the foreign buyers tax last year.

And it’s a sign that the tax has affected more than just foreign investment, analysts say.

Coverage of Vancouver real estate on Globalnews.ca:

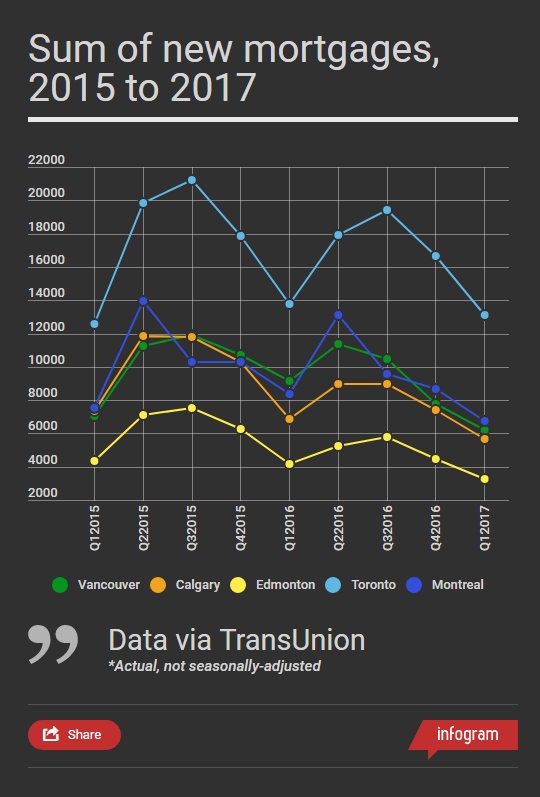

Data gathered by credit reporting agency TransUnion show that the number of new mortgages in Vancouver dropped by 32 per cent year-over-year in the first quarter of 2017.

There were 9,162 new mortgages in the first quarter of 2016. That fell to 6,226 new mortgages this year, the fewest that there have been going back to the start of 2015.

The drop in new mortgages was deeper than it was at the national level (-10.4 per cent), as well as in Toronto (-4.6 per cent), Calgary (-16.9 per cent), Edmonton (-22 per cent) and Montreal (-19.4 per cent).

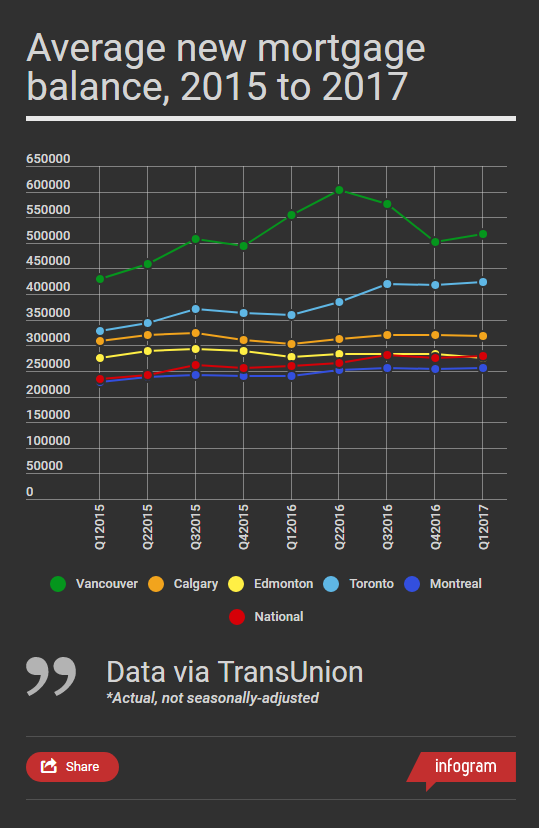

TransUnion data also showed Vancouver’s average new mortgage balance dropping by 6.6 per cent year-over-year in the same quarter.

The average new mortgage balance in Vancouver was about $517,000 in the first quarter of this year. That was down from $554,000 year-over-year.

While that wasn’t the lowest it’s been in recent years, it also represented a drop as average new mortgage balances went up nationally (7.9 per cent), as well as in Toronto (17.7 per cent), Calgary (4.6 per cent) and Montreal (6.5 per cent).

Edmonton was the only other city to record a year-over-year drop in its average new mortgage balance; it fell by 0.8 per cent.

The drop in mortgage activity was blamed on a number of factors.

One was the foreign buyers tax; another was the “stress tests” that the federal government imposed last year — tests that required borrowers to show they could afford their mortgage payments in the event of an interest rate hike, Matt Fabian, TransUnion’s director of research and industry analysis, told Global News.

These policy changes appear to have had an effect on speculative activity in the city’s housing market, he said.

“I think the people that were speculating on real estate seem to have stopped, and that contributed to some of the drop,” Fabian told Global News.

He also said that, due to the combination of these rules, “a lot of buyers are saving to put a larger down payment on their home, especially first-time homebuyers, to avoid a lot of those penalties and new rules.

“They’re starting to put a larger down payment, which I think is shrinking the mortgage a little bit.”

READ MORE: 3-bedroom Cambie Street home on the market for $11 million

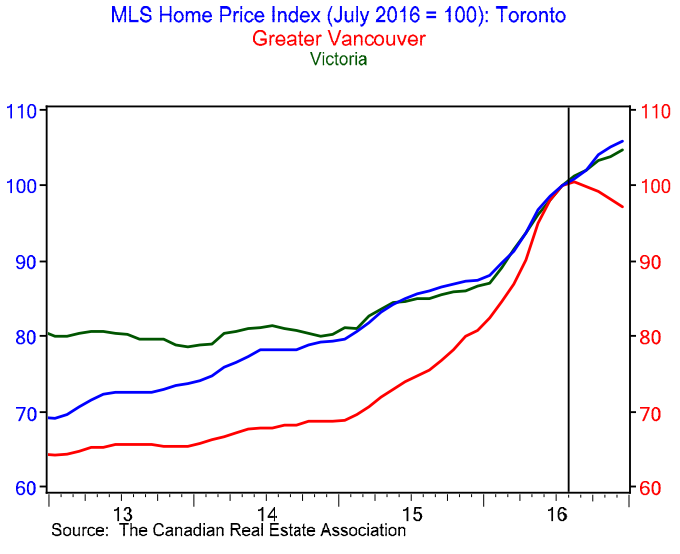

Analysts have shown skepticism in recent months that the federal government’s mortgage rules have made much of a difference on housing prices.

A chart published by BMO in January showed prices dropping in Vancouver, where a foreign buyers tax had been implemented, while they kept growing in Victoria and Toronto, where one hadn’t been imposed at the time.

The Province of Ontario has since implemented a foreign buyers tax as part of a slate of measures under its Fair Housing Plan.

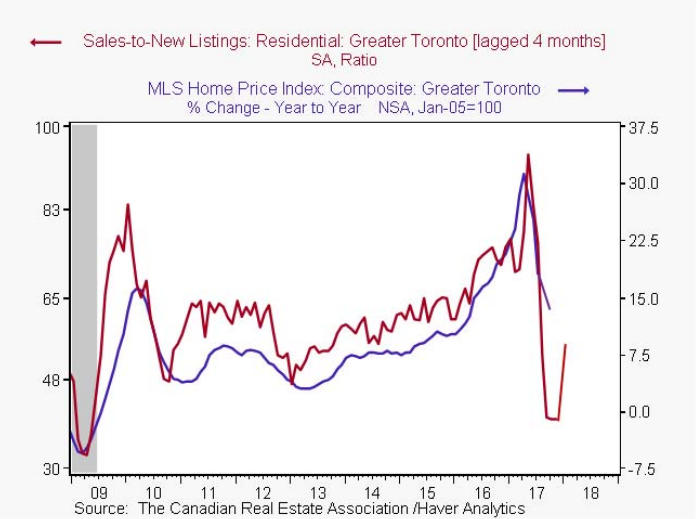

And as BMO noted in another chart released Wednesday, Toronto’s benchmark price fell two per cent month-over-month in seasonally-adjusted terms.

Year-over-year price growth fell to 14.3 per cent, down from 30 per cent in April, it added.

BMO economist Sal Guatieri told Global News that the drop in Vancouver’s average new mortgage balance “largely stems from the foreign buyers tax.”

He said the tax “quickly cooled the market” and reduced benchmark prices on single-family detached homes by 6.5 per cent over a six-month period — and that was after they accelerated by 39 per cent year-over-year in June 2016.

“The tax slashed the foreign buyers’ share of sales from above 10 per cent to the low single digits,” Guatieri said in an email.

“Moreover, it short-circuited the speculative mentality that was juicing prices.”

The federal government’s mortgage rules “likely had a much more moderate dampening effect on the market, as there was no noticeable slowing effect on Toronto’s roaring real estate market,” he added.

- With files from Erica Alini

Comments