The federal government introduced new mortgage rules last October that were aimed, in part, at calming down record-setting household debt levels across Canada.

But looking at December data, it’s tough to see whether the new rules are having their intended outcomes.

Household credit has only kept growing — and that includes mortgage debt, according to numbers released by the Bank of Canada (BoC) on Monday.

The Liberals’ mortgage rules included a “stress test” for prospective homebuyers that was meant to ensure they could afford their mortgages in the event of an interest rate hike.

Not only would borrowers have to qualify for mortgages at the rates they negotiated with their lenders; they would also have to qualify at the BoC’s posted rate for a conventional five-year mortgage. That rate was 4.64 per cent on Thursday.

READ MORE: New federal mortgage rules come into effect today

The Liberals sold these rules as a way to tackle high debt and housing affordability. But the results have been decidedly mixed.

Canadian new home price growth slowed in December, but the MLS Home Price Index also shows prices growing in major housing markets like Toronto.

The picture was much clearer for household credit: Canadians’ personal debt pushed past the $2-trillion mark in December, reaching another record high after climbing 0.54 per cent from the previous one in November.

Household debt in December 2016 also represented a climb of 5.2 per cent over the same month in the previous year.

A month-over-month increase of 0.54 per cent doesn’t seem significant in isolation.

But that was above the monthly average (0.42 per cent) at which household debt grew across Canada last year.

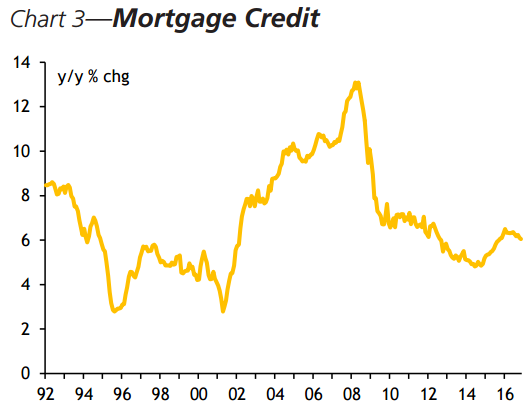

Mortgage credit kept growing, too.

Mortgage debt grew by 0.55 per cent in December (above the 0.48 per cent average for 2016) and by 5.9 per cent year-over-year.

The data was not seasonally-adjusted. But the trends nevertheless surprised Benoit Durocher, senior economist at Desjardins.

“We were expecting a slowdown at the end of 2016,” he told Global News.

But December was “likely to early to see the impacts on mortgage credit growth, particularly given that some housing activity finalized in December was potentially agreed to before the new rules were in effect,” said Department of Finance spokesman Paul Duchesne.

“Depending on broader macroeconomic developments, we would expect to see gradual impacts of the measures in the coming months as affected homebuyers save for larger down payments and/or purchase less expensive homes than they might have in the absence of the new rules.”

“It will take time for the full impacts of the measures to be evident.”

This is, however, far from the first time that changes to mortgage rules have had a questionable influence on the growth of household credit and mortgage debt.

In 2012, the Conservative government introduced mortgage rules that reduced the maximum length of a government-insured mortgage from 30 to 25 years.

That change also came in response to concerns about household credit levels.

But, save for a dip in household credit in February 2013 (which was driven more by a fall in consumer, not mortgage credit), BoC data show the rules didn’t slow debt growth very significantly.

And seasonally-adjusted data showed no dip at all.

Over-leveraged

Three months ago, Durocher issued a client note that sounded a warning about Canadian debt levels.

He noted that, at 100.6 per cent, Canadian household debt had exceeded the size of the country’s economy.

It grew even more in the third quarter, hitting 101.15 per cent of GDP, according to StatsCan data.

Canada’s second-quarter household debt-to-GDP ratio was the highest in the G7, Durocher noted.

“The high level of household debt is undermining the Canadian economy and this represents a significant risk over the medium and long terms,” he said.

One of the biggest risks is that households will have difficulty meeting their financial obligations if interest rates go up, Durocher told Global News.

But there are other issues that come with high household indebtedness, like “lower consumption and to lower GDP growth,” he said.

READ MORE: Record debt: Canadian households sink deeper and deeper into the red

He thinks that 2017 is the year in which Canadians should start ramping down their debt, as he expects an interest rate hike in 2018.

Such a hike would take some time before it really hit certain borrowers — many people, for example, have mortgage rates locked in for anywhere from three to five years.

Durocher still thinks it’s possible that the Liberals’ mortgage rules could slow credit growth sometime this year – though he doesn’t know when.

CIBC economist Benjamin Tal agrees.

In a report issued Feb. 2, he said mortgage rules are just one reason why the growth of new mortgages could cool in 2017.

This could come due to factors such as “tougher qualification criteria,” an “increased share of less expensive (condo) units in total housing sales,” higher mortgage rates and slowing activity in centres like Vancouver.

“Overall we expect mortgage debt outstanding to rise by an annual rate of around five per cent in the coming two years,” Tal said.

In other words, he doesn’t expect it to drop — only to grow at a rate that’s about 0.9 per cent slower than it was last year.

Reducing your debt

So what can individual Canadians do to manage their debt loads?

One financial coach has a few ideas.

“Debt of this sort contributes nothing to our long-term wealth and financial well-being,” Noel D’Souza, CFP®, Money Coach with Money Coaches Canada, told Global News.

“Eventually the ‘debt party’ ends — usually badly — and individuals and families are left with a large bill to pay and the substantial stress that goes with it,” he said.

In order for households to reduce their debt, “it’s crucial to get a firm understanding of your cash flow,” D’Souza said.

That means finding out how much money they have coming in, how much they’re spending and where they’re spending it before they can make any decisions about reducing their debt.

Households also need a goal to work toward — a “motivating goal that will encourage you to make necessary lifestyle changes and resist the ongoing temptation to overspend,” he said.

Comments