Alberta is reducing the maximum amount payday lenders can charge to the lowest in Canada and requiring these companies to give borrowers more time to pay back the money they owe.

The provincial NDP tabled the draft legislation, An Act to End Predatory Lending, in the legislature Thursday. If passed, the bill would cut the maximum payday loan fee to $15 per $100, from $23. And that $15 would have to include any additional services such as insurance attached to the loan.

It also requires lenders to give borrowers two pay periods in which to pay back the loan; right now, a borrower has until their next payday to do so.

READ MORE: Why one woman’s leaving the payday loan business

“Interest rates that are 600 per cent or more are predatory,” Service Alberta Minister Stephanie McLean said Thursday.

“Loans that require you to take out loans to pay back loans are predatory. We are ending it.”

It’s a bold step as jurisdictions across Canada are trying to figure out how to rein in what many argue is an exploitative model that profits from people least able to pay.

And this is just step one: Alberta wants to reduce the maximum payday loan fee even more, once there are enough alternatives out there for the people who need the service.

That’s where things could get tricky.

IN DEPTH: Canada’s instability trap

As payday lenders argue, there’s significant demand for the low-cost, short-term loans they provide, often to people whose credit isn’t good enough to borrow money elsewhere.

Canadian Payday Loan Association President Tony Irwin says the proposed regulations will leave these people without options.

“It will lead to a significant reduction of the industry in Alberta. And that will mean store closures. It will mean job losses. And it will mean a restriction of access for credit,” he said.

“What Alberta has proposed is, I think, going to end up hurting a lot of the very people that the government is trying to help. … Their need for credit will not go away.”

WATCH: Alberta cracking down on payday loan rules

Albertans borrow about $500 million a year from payday loan companies, the government says. If these companies shutter stores because of the new rules — as they’ve threatened stringent regulations will make them do — the need will still exist.

The bill would require McLean to monitor the market and report back to the legislature on emerging alternatives to payday lending. The plan is to further reduce maximum payday loan fees once there are enough options for people who’ll need the cash.

But it isn’t clear how exactly the province will ensure those alternatives proliferate: First Calgary Financial and Momentum are expanding their Cash Crunch Loan, previously a pilot project, across the province in August. Servus Credit Union has another alternative program rolling out at the end of this year.

And as Servus President Garth Warner notes, credit unions have existed for ages.

But these services are still tiny compared to the payday loan industry.

CHEQUED OUT: Inside the payday loan cycle

“It’s very important that Albertans have access to short-term credit,” McLean said.

“I am confident that we will get to that point.”

WATCH: Payday loans are on the rise in Vancouver, report finds

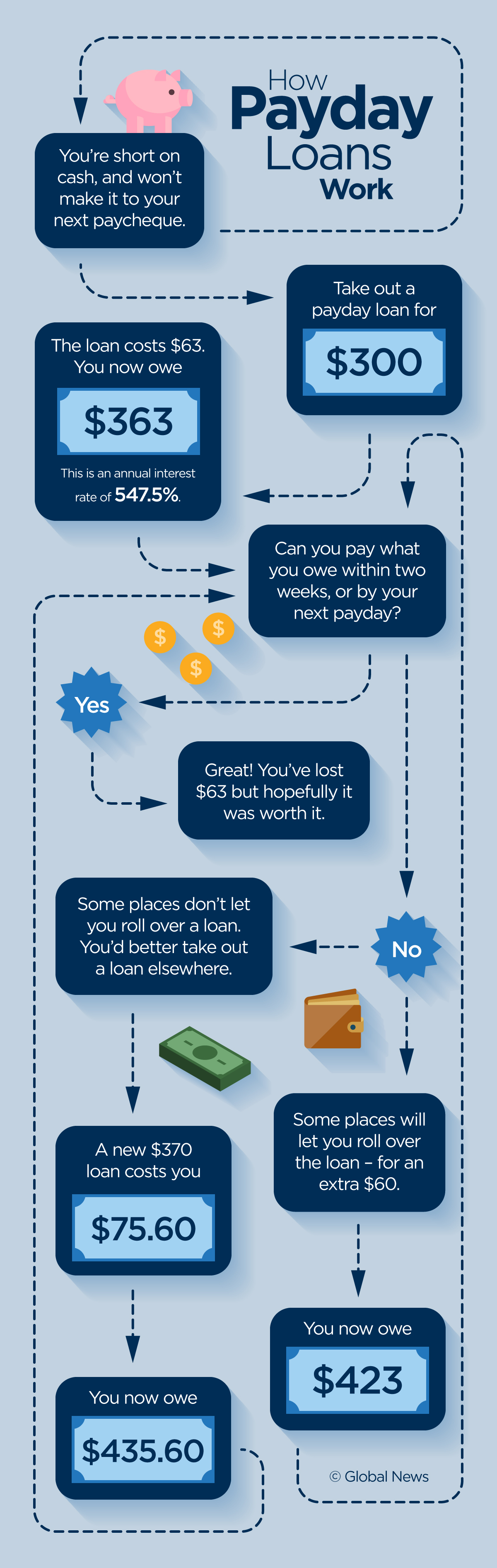

While it’s illegal in Canada to charge more than 60 per cent interest on a loan, short-term loans are exempt. Once you annualize the interest rate, a $23 fee on a $100 loan that’s due in two weeks works out to about 552 per cent interest. A $15 fee in that same period works out to 360 per cent.

The draft legislation would also require payday lenders to collect more information on their customers, and pass it on to the province so the government can get a better sense of who is borrowing money — where they live, what they make, how many loans, on average, they take out.

The law would require lenders to give customers financial literacy material and give them the option of electronic paperwork and receipts.

Payday loan companies have argued they need to charge high fees in order for their business model to function: a Deloitte study commissioned by the Canada Payday Loan Association found these companies have to charge at least $20.74 per $100.

The loans they make are just too risky, and the chance of default too high, to charge less than that, Irwin said.

“It’s an expensive product to provide. That is a simple reality in this business.”

Irwin doesn’t like the two-instalment rule, either: He says that would mean “a whole different type of lending product. It’s not a product our members offer today.”

WATCH: Nova Scotia scrutinizes payday loan rules

Shelley Vandenberg, president of First Calgary Financial, argues it doesn’t have to be that way: if small-scale loans are less onerous to pay back, she says, the default rate won’t be as high.

“I don’t see payday loans as high-risk loans,” she said.

“We’re putting skin in the game. We believe in this social issue. We believe we can make a positive impact.”

Comments