If you were given a surprise $5,000 with no strings attached, what would you spend it on? A new car or kitchen renovation? Tickets to an exotic location? Or would you invest it?

As inflation remains near decades-high levels, almost half of Canadians say they’d spend such a windfall on paying down their debt or covering day-to-day expenses, according to a poll from the Angus Reid Institute (ARI) conducted in early August.

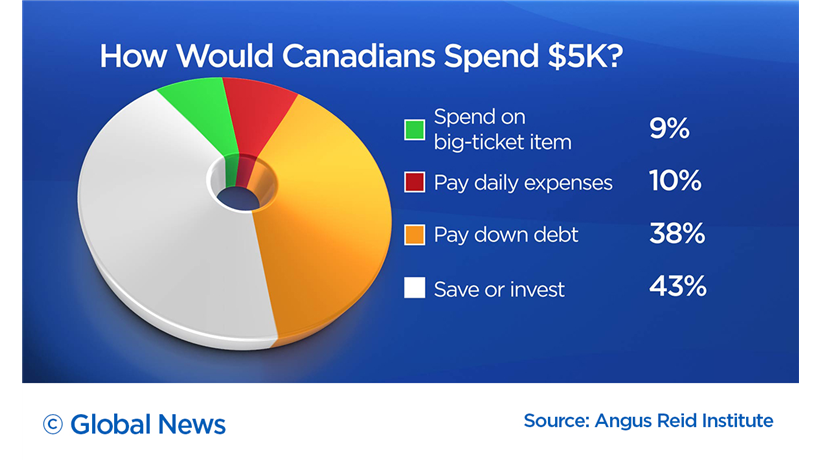

Some 38 per cent of Canadians polled said paying down debt or some other long-term financial obligation would be their first priority, while 10 per cent said such a windfall would mostly go towards paying down day-to-day expenses.

Meanwhile, 43 per cent of respondents said the money would be saved or invested and only nine per cent indicated it would go towards a “big-ticket” purchase.

The $5,000-windfall question came as part of a survey from ARI examining the “toll of inflation” and asking Canadians how they’re coping with the rising cost of living. The poll, conducted online, samples more than 2,200 members of the Angus Reid Forum.

Four out of five respondents said they’re cutting back on discretionary spending, putting off major purchases, scaling back travel, driving less or deferring saving in recent months. That figure is up from 74 per cent in February.

Since that time, annual inflation rose to nearly 40-year highs as the war in Ukraine and global supply chain constraints pushed prices up across the board. Headline inflation eased slightly in July to 7.6 per cent amid lower gas prices, but pressure remained high on staples such as food.

ARI President Shachi Kurl tells Global News that for a generation of Canadians, interest rates and inflation have been relatively low and goods have been affordable and accessible. The current inflation episode is marking a change of priorities as some households grapple with making ends meet amid a downturn.

“For the first time in their adult lives, many Canadians are experiencing moments of, ‘Huh? This is new. This is different. What are we going to do about it?’” she says.

Get weekly money news

Kurl notes that Canadians on the lower end of the income spectrum are feeling the pain of inflation the most.

Indeed, 23 per cent of respondents making less than $25,000 per year would put a sudden $5,000 windfall towards day-to-day expenses, compared with just five per cent of those with an annual income between $150,000 and $200,000.

“That is an impact that really has people counting every penny and starting to get to a point where they are dealing with trade offs and decisions around what gets paid this month, what gets deferred,” she says.

Thought experiments good for setting ‘financial priorities’

Natasha Knox, principal of Alaphia Financial Wellness in British Columbia, says that it’s hard to know what exactly has Canadians dreaming about saving and paying down debt as the ARI polling is just a “snapshot” without an earlier comparison.

But when it comes to spending a hypothetical windfall, there’s a lot that Canadians can learn about their own “mental accounting biases,” she says.

“People sometimes treat windfalls differently than other kinds of money,” she says.

To help suss out any underlying financial priorities from the windfall question, Knox would urge someone to think about the money in a different context: if it were generated in a side hustle, perhaps accumulated over a six-month timeframe rather than all at once, would it still be going to the same place?

If the answers to that question and the windfall experiment are different, it could be a sign to align your financial desires.

“If a person doesn’t have already articulated their financial priorities, now would be a time,” she says.

“A thought experiment such as this could be perceived as simply an acceleration of any of those priorities.”

Paying down high-interest debt always a good idea: experts

- IBC estimates $230M in insured damage claimed from Edmonton storms

- Alberta First Nation sues Ottawa over $5 treaty annuity, argues amount stuck in 1899

- Jobs hang in the balance as Ekati diamond mine in N.W.T. closing early

- WestJet flight attendants hold information pickets as strike vote takes place

In addition to inflation pinching Canadians’ bottom lines, the Bank of Canada’s efforts to raise interest rates and tamp down on these pressures are meanwhile raising the cost of borrowing.

Wes Cowan, senior vice-president of accounting and insolvency firm MNP LTD., says that as a result, he’s not surprised to see 38 per cent of Canadians dreaming about paying down debt with a windfall.

Half of respondents aged 35-54 meanwhile said they’d put the $5,000 towards their debt; ARI notes that group which represents a third of the adult population but holds 57 per cent of the national debt load, per Statistics Canada.

“That tells us something about the level of concern that people are carrying about the amount of debt they have and perhaps how much that debt will cost them if interest rates continue to rise,” Cowan tells Global News.

Both he and Knox agree that paying down debt is always a smart move if you come into unexpected cash.

The faster you can pay down debt, the less interest accumulates on the loan and the less you’ll owe overall, Cowan says.

“You’re going to have less debt to service going forward. And so in terms of your cash flow each month, it’s going to be better,” he says.

Importantly, Canadians struggling under the weight of debt do not need to wait for a sudden boon to get their finances in order.

Cowan recommends focusing on debt loads such as credit cards — those with the highest rate of interest or unsecured debt that responds directly to the Bank of Canada’s policy rates. Taking out a line of credit from your bank with a lower rate of credit to pay down the most expensive debt could be a starting point.

Canadians can also talk to a licensed insolvency trustee, who is regulated by the federal government, for more formal ways to get debt under control, he says.

Angus Reid Institute’s poll was conducted through an online survey Aug. 8-10. It surveyed a representative randomized sample of 2,279 Canadian adults who are members of the Angus Reid Forum. It carries a margin of error of +/- 2.0 percentage points, 19 times out of 20.

Comments

Want to discuss? Please read our Commenting Policy first.