As Albertans begin to assess the damage inflicted by one of the worst natural disasters in the province’s history, insurance companies are bracing for their own equally unprecedented flood.

A torrent of claims.

With an estimated one hundred thousand people displaced by the bursting of the Bow and Elbow rivers’ banks – both of which cut through Calgary, forcing an evacuation of the downtown core – damages to houses, businesses, vehicles and other property are near certain to climb into the hundreds of millions of dollars.

Insurance industry representatives and experts said it’s far too early to estimate a dollar figure, but some suggested Friday they are preparing for an event at least two to three times the scale of the 2005 flooding of Calgary, which saw $275 million in insured losses, according to Environment Canada.

Alberta has been a source of concern for insurers over the last decade, with four of the six most expensive natural disasters in the country’s recent history occurring in the Western Canadian province.

- Premier Moe responds to Trudeau’s ‘good luck with that’ comment

- Drumheller hoping to break record for ‘largest gathering of people dressed as dinosaurs’

- As Canada’s tax deadline nears, what happens if you don’t file your return?

- Posters promoting ‘Steal From Loblaws Day’ are circulating. How did we get here?

Alberta, with a geography that’s bound by the towering Rockies in the west that give way to sloping lowlands in its east, has taken a handful of severe shellackings from mother nature in recent years.

So have insurers, forced to cover claims totalling $1.87 billion – an amount that significantly exceeds weather-related claims in other provinces that seemingly have less volatile environmental conditions.

The escalation in the number of powerful storms and fires, like Slave Lake in 2011 that saw claims of $753 million alone, have pressured insurance premiums, experts say.

“The two ways to deal with it are to exclude coverage or adjust the premium up to cover the risk,” Craig Brown, professor of tax law at the University of Western Ontario said.

“Insurance is a competitive market, they can shop around for various options. But insurers will set their premiums based on their claims records,” Kee said.

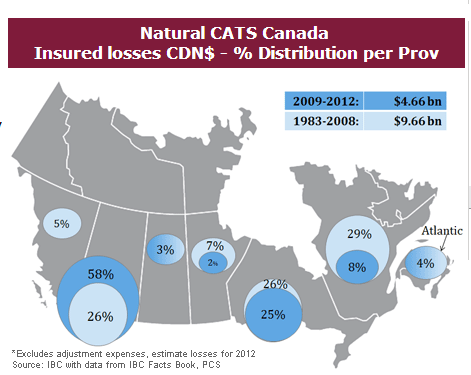

Since 2009, Alberta’s share of disaster-related claims has spiked, accounting for nearly 60 per cent of the national total, or more than double that of Ontario, the source of the second-most amount of disaster-related claims.

The figure is far above Alberta’s historical average (between 1983 and 2008) of 26 per cent of all claims made nationally, Insurance Bureau of Canada data shows.

While debate still hovers over evidence linking climate change to a higher frequency of environmental events like the one playing out in Calgary and southern Alberta at the moment, it is something insurers are growing increasingly wary of, Brown said.

“They’re very concerned about climate change generally and what that might do to claim patterns,” the professor said.

Bank of Montreal, one the country’s biggest banks, is expecting the size of the disaster to be two to three times that of the 2005 floodings, regional executive vice-president Robert Hayes said.

The bank, alongside others with insurance businesses in the province such as the Royal Bank of Canada and TD, pledged $100,000 to relief efforts on Friday. TD matched that sum while RBC, the country’s biggest bank, donated $125,000 to the Canadian Red Cross.

BMO said it will allow customers to delay mortgage payments and payments on business loans or lines of credit until after the crisis, encouraging customers to contact the bank.

“The last concern they should have is, whether they can make a payment or not, when they are trying to get in and out of their house or fix their basement,” Hayes said.

As in other provinces, insurers in Alberta do not cover damages from “overland flooding,” pretty much a blanket policy across the country due to the high risk of rivers overflowing sending water through the front doors and basement windows of homes and businesses.

Insurance companies are responsible for sewer backups, as well as the damages to vehicles and other property. In situations where there is both overland flooding and a backup of sewage, insurers may cover the latter costs if damage related to sewage backup can be shown, Kee said. “It’s going to be up the adjuster to make that decision,” he said.

Ottawa and the provinces routinely provide disaster relief under the Disaster Financial Assistance Arrangements (DFAA) program, administered by Public Safety Canada.

DFAA relief was last deployed a year ago, when the federal government gave $50 million to Manitoba to assist with flooding in the spring of 2011.

In a statement Friday, Prime Minister Stephen Harper, who left Ottawa for his home province mid-day, said the government “offered any and all possible assistance to the Province of Alberta in response to the situation.

“We remain ready to provide additional assistance if requested by provincial authorities.”

Comments