Editor’s note: This article was updated to reflect the Bank of Canada’s 75-basis-point interest rate hike on Wednesday.

One of Canada’s major banks is arguing that while most Canadians are largely insulated from the impact of rising interest rates today, efforts to get inflation back to manageable levels could leave some debt and mortgage holders feeling the pain for years to come.

The Bank of Canada is raised its benchmark interest rate again on Wednesday, marking the fifth time it would have raised the cost of borrowing so far this year in an attempt to cool the economy and tamp down rampant levels of inflation.

CIBC deputy chief economist Benjamin Tal argues that thanks to the structure of Canadian household debt, the direct impact of rising interest rates is currently limited to roughly one in four debt holders, largely focused around homeowners with certain kinds of mortgages.

“When people hear about higher interest rates, they assume that everybody will be paying more. And that’s not the case because of the structure of debt in our economy,” Tal says.

Crunching the numbers on Canadian debt

Tal and CIBC’s Karyne Charbonneau broke down the impact of rising interest rates on Canadian household debt in an Aug. 22 report using data from Statistics Canada.

The authors note in the report that 30 per cent of Canadians are completely debt-free, meaning a more expensive borrowing rate won’t affect their payments at all.

Many people with debt don’t actually have a mortgage, meaning their household debt comes from credit cards or loans to finance a new car, for example.

But credit cards already have very high rates of interest, making the impact of Bank of Canada rate hikes largely negligible, Tal argues, and instalment-based loans usually have steady interest rates through the length of the term.

So that just leaves mortgage holders — and homeowners who take out a home equity line of credit (HELOC) on their properties — to feel the brunt of rate hikes.

Those with adjustable rates are certainly feeling the effect of higher rates, as the amount they pay on their mortgage increases immediately when the Bank of Canada hikes its policy rate. That’s the case for interest rates on HELOCs, too.

But 70 per cent of Canadians with variable-rate mortgages are on fixed payment schedules, meaning they don’t pay more each month when their rate rises. Instead, the amortization, or the overall length of their mortgage term, extends.

Tal says that since five-year, fixed-rate mortgages are “dominant” in Canada, most monthly payments are holding steady through this rising interest rate environment. Homeowners on fixed rates will only feel the sting of higher rates when they renew their mortgage in a few years’ time, he says.

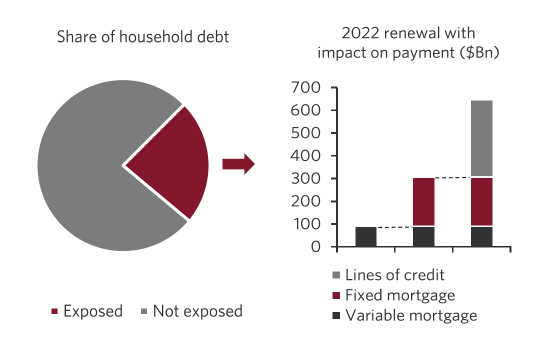

That means that for this year, it’s only one-fifth of fixed-rate mortgagers exposed to the interest rate hit, along with adjustable rate and HELOC holders.

Get weekly money news

“Putting it all together, we get that out of the total household debt of $2.7 trillion, close to $650 billion (24 per cent) face actual increase in interest payment this year,” the report reads.

Tal tells Global News that he doesn’t expect rates to continue rising past September, but that doesn’t mean other mortgage holders are out of the woods.

Rather, each year could see a wave of hits to Canadian fixed-rate mortgage holders renewing into this new higher rate environment.

“The impact is not really significant today, but cumulatively, it will be,” he says.

Those 'at the margin’ feeling pain

Tal acknowledges that even limited impact from rate hikes can mean that Canadians “at the margin” will “feel the pain significantly.”

Mortgage rate analyst Rob McLister tells Global News that Canadians who took the plunge earlier this year and jumped at an adjustable-rate mortgage before the Bank of Canada started raising rates in March could have secured an initial rate of roughly 1.45 per cent, “not far from the all-time low.”

The Bank of Canada delivered on market expectations to hike rates another three-quarter of a percentage point on Wednesday, meaning these mortgage holders have seen their rates rise 300 basis points over the course of seven months.

On an average mortgage of $300,000, that equates to about $500 more in monthly payments, McLister says.

“If you’re pushing your debt-ratio limits, then 500 bucks a month could push you over the edge,” he says.

Indeed, more than half (56 per cent) of homeowners are concerned about their ability to cover monthly mortgage payments, according to a recent survey commissioned by IG Wealth Management.

Some 43 per cent of Canadian mortgage holders polled after the Bank of Canada’s last rate hike in July said they were unsure how they are going to make ends meet, per the online survey conducted by Pollara Study.

While McLister notes that the federal mortgage stress test introduced in 2018 should mean that these Canadians are prepared to handle higher costs of borrowing, if a global supply shock or other economic disruption forces the central bank to hike rates past September to get inflation under control, mortgage rates could rise higher still.

- CIBC agrees to proposed class-action settlement over NSF fees

- California is banning ‘sell-by’ food dates. How Canada’s packaging compares

- Green light for Greenlight: Pembina, partners go ahead with gas plant for data centre

- Ontario’s new auto insurance rules now in effect, but choice comes with some risk

“Then we’re talking about materially more pain, especially for the borrowers on the fringe,” he says.

While Tal’s analysis lays the groundwork for a Bank of Canada interest rate freeze for a year after Wednesday’s probable hike, he also tells Global News there is “absolutely” a chance that the bank takes rates higher due to “external forces” in the ever-changing global economy.

Revisit your budget as rates rise

Whether you’re feeling the pain of rising rates today or see your renewal date looming on the horizon, experts say there are some steps you can take now to lessen the impact of interest rates on your budget.

That same IG Wealth Management survey found that even as rising mortgage rates push many households to their limits, only two in five respondents said they factor their mortgage into their budget calculations.

That comes as a surprise to Alana Riley, IG Wealth Management’s head of mortgage, insurance and banking.

“That’s a big piece to leave out. For me especially, that’s the first thing that’s in the budget, because that’s not something that’s really flexible,” she says.

Riley says that Canadians who got into the housing market in the past few years were likely accustomed to a low-rate environment and might be experiencing “sticker shock” when they’re coming up to renewals.

But for Canadians forced to cut on spending to accommodate growing mortgages, Riley says there are few easy choices right now.

While inflation showed signs of possibly peaking in July, the cost of living is still well above the Bank of Canada’s two-per-cent target. It’s also not a great time to take money out of the market or forego contributions to registered savings accounts, she argues, as the value of those investments might have dwindled in this year’s market downturn and losing out on compounding interest can cost a household in the long term.

A mortgage broker or financial adviser can present some options on lessening the impact of rising interest rates, she notes. A longer amortization on your mortgage could reduce monthly payments and variable-rate mortgages can be converted to fixed at any point if the fear of rising rates weighs heavily on your budgets.

As the economy and interest rates continue to shift, Riley recommends doing regular check-ins on your financial assumptions to make sure they hold up for the long term.

“As markets change, as things change in your personal situation, all the more reason why you’re wanting to get in front of your financial planner on a regular basis, just as you would your doctor or dentist,” she says. “This isn’t a one-and-done.”

Comments

Want to discuss? Please read our Commenting Policy first.