Canadians will have to devote an unprecedented amount of their incomes to debt repayments, if interest rates return to normal levels, according to a new report.

“The financial vulnerability of the average household would rise to levels beyond historical experience,” the Parliamentary Budget Officer (PBO) warned today, based on projections about interest rates, household debt and debt servicing costs.

READ MORE: Canadians have more debt than ever, but fewer are going bankrupt. Why?

According to those forecasts, if the Bank of Canada (BoC) were to raise the key interest rate from the current 0.5 percent to 3 percent, the average Canadian family would have to use 16.3 per cent of its disposable income for debt repayments by the end of 2021.

Canadians currently need 14.2 percent of their after-tax income to keep up with principal and interest payments and have never used more than 14.9 percent of their income to service debt, the PBO noted.

WATCH: Rising debt, sizzling housing markets leave Canada more vulnerable

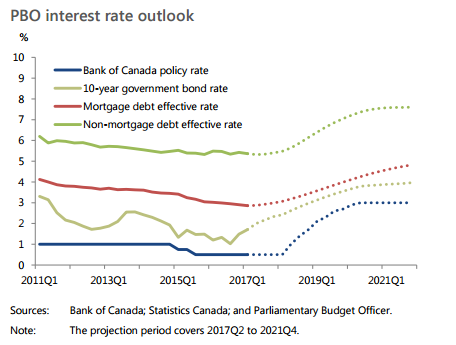

How much interest rates could rise

Here’s how much interest rates could rise over the next few years, according to the PBO:

- The BoC’s key interest rate: This is the interest rate that affects most other interest rates throughout the economy. When the BoC raises it, the cost of borrowing goes up for most Canadians. The bank uses the level of interest rates to keep inflation in check and promote economic stability and employment. As the Canadian economy heats up, the BoC has said it is thinking about finally lifting rates from the historic low levels where they’ve been for years. The first hike could happen as soon as July, according to Bank of Montreal. The PBO projected the key interest rate to rise from 0.5 per cent today to 3 per cent by mid-2020.

- Mortgages: The interest rate on mortgage debt could climb from 2.9 percent to 4.8 per cent by the end of 2021, according to the PBO. This will affect homebuyers. However, the vast majority of Canadians, who have fixed-rate mortgages, won’t feel the impact of higher rates until their loan is up for renewal. And at 4.8 percent, the interest on mortgage debt would still be below Canada’s long-term average of 5.4 percent, the PBO noted.

- Non-mortgage debt: Interest rates on debt other than mortgages — such as unsecured lines of credit and credit cards — will likely go from 5.4 percent to 7.6 percent by the end of 2021. That would leave rates at a level just shy of the historical average of 7.7 percent, the PBO reported.

Canadians won’t immediately stop loading up on debt

For a while at least, Canadians will keep borrowing, even if debt becomes more expensive, the PBO said.

“We expect household indebtedness to increase due to continued gains in real house prices and elevated levels of consumer confidence.”

READ MORE: Rising interest rates could cost the average Canadian $130 a month more in debt repayments

As a result, by the end of next year, Canadians will likely owe $1.80 for every dollar of disposable income, up from the current $1.74. The PBO expects household debt to stabilize after 2018.

Canadians have kept their borrowing in check over the past couple of years, but didn’t quite stop piling on debt, the report suggests. As a result, household debt as a share of disposable income continued to grow, even if interest rates kept falling.

Now that rates are set to rise, Canadian households are on course to become more financially stretched than they’ve ever been before.

- Canadian man dies during Texas Ironman event. His widow wants answers as to why

- ‘Shock and disbelief’ after Manitoba school trustee’s Indigenous comments

- Canadian food banks are on the brink: ‘This is not a sustainable situation’

- Invasive strep: ‘Don’t wait’ to seek care, N.S. woman warns on long road to recovery

Comments