Countrywide housing data for February will be out Wednesday, but we already know what happened in the two biggest markets: sales continued to slump in Vancouver, while prices continued to soar in Toronto.

So what does that say about the effectiveness of the tighter mortgage rules introduced by the Ottawa last October?

WATCH: What Canada’s new mortgage rules mean for new homebuyers

A lot, according to Simon Fraser University professor Josh Gordon.

The fact that stricter mortgage rules don’t appear to be cooling Toronto prices strongly suggests that wealthy foreign and domestic investors, rather than first-time home buyers, are primarily responsible for skyrocketing prices, Gordon wrote in a paper published today by the Ryerson City Building Institute.

READ MORE: Foreign buyer tax alone won’t cool down scorching Toronto housing market: report

What the numbers show

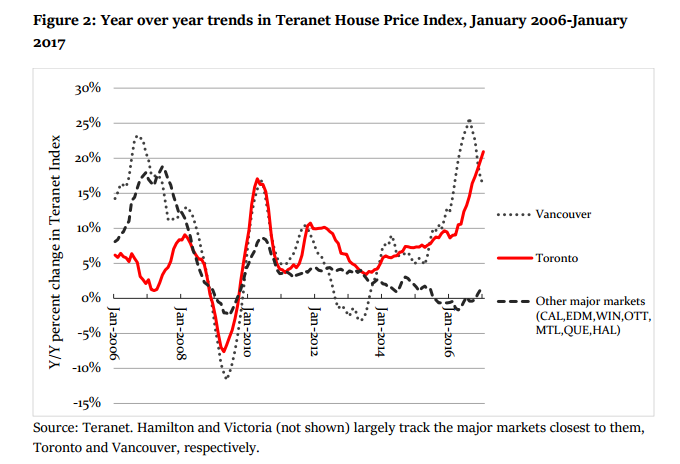

In Vancouver and Toronto

Residential home sales dropped almost 42 per cent in February compared to the same period last year, the Real Estate Board of Greater Vancouver said March 2. It was the second consecutive month of double-digit month-on-month declines. Meanwhile, home prices have been cooling roughly since the B.C. government announced a 15 per cent tax on foreign buyers in July.

READ MORE: B.C. foreign buyers tax really did yank down Vancouver home prices: BMO

In Toronto prices surged 23.8 percent in February compared to year-ago levels after a similar increase in January.

The Toronto Real Estate Board (TREB) has blamed the spike on a lack of housing supply, but Gordon and others argue that what’s truly causing the housing shortage is insatiable demand driven by wealthy buyers and a bubble mentality. No amount of residential building would be able to satiate such demand, noted Gordon.

READ MORE: Biggest factor in Ontario’s red-hot housing market is demand: finance minister

Get weekly money news

Canada has been adding new housing units at a pace that surpasses new household formation for the past year, Bank of Nova Scotia economist Derek Holt recently wrote in a research note.

Prices that are flat-lining in Vancouver and spiking in Toronto strongly suggest that B.C.’s foreign buyer’s tax appears to have worked. The mortgage stress tests, not so much, at least in the country’s two largest cities.

READ MORE: Toronto Real Estate Board sees another year of double-digit price increases

In the rest of Canada

The jury is still out on whether the federal mortgage rules had a more meaningful impact on the rest of Canada.

“The hope was to prevent some individuals from overstretching themselves in order to buy a house — and that was fundamentally a good idea,” Gordon said.

To gauge that, one would have to look not only at housing prices, which have been cooling for a while in much of Canada, but at data like household debt and borrowing levels. And that data isn’t conclusive yet, Gordon said.

READ MORE: Ottawa’s new mortgage requirements could make it harder to secure a mortgage

What we do know, is that there at least one precedent in which similar regulation has worked. The round of mortgage rule-tightening implemented by the Harper government in 2012 did succeed in slowing down house-price growth across much of the country, noted Gordon. Back then, Ottawa reduced the maximum amortization period on residential mortgages from 30 to 25 years, lowered the amount Canadians could borrow through refinancing, and eliminated government-backed mortgage insurance on homes over $1 million.

As the chart below shows, the measures had only a temporary impact on Toronto and Vancouver, but they seem to have had a lasting effect on the rest of Canada.

- ‘It was difficult’: Residents of Clinton, B.C. recount evacuating wildfires

- B.C. community’s water system damaged by alleged vandalism during wildfire response

- Feds’ rejection of island airport plan prevents waterfront ‘destruction’: advocates

- Trump’s tariff threat already costing Canadian businesses, trade lawyer says

Around the world

Canada isn’t the only country with skyrocketing housing prices in major urban areas. Australia, New Zealand, Britain and Switzerland, to name just a few, have much the same problem and have also tried to deal with it by tweaking regulations, rather than raising interest rates, which has broad consequences on the entire economy.

READ MORE: Canadians skirting new mortgage rules with risky bundled loans

Results have been mixed, but a recent review of such efforts by the Bank for International Settlements has come to the conclusion that taxes are “the only policy tool with a discernible impact on high housing prices.”

Time for a new housing tax for Toronto?

Tackling the housing affordability crisis in Toronto requires measures that would only apply locally, as opposed to the broad-brush mortgage rules introduced by Ottawa in October, Gordon argued.

The city could use not only a Vancouver-style foreign buyers’ tax, but a surtax on high-end properties that would target buyers who are not paying much, if anything, in Canadian income taxes. The latter measure, which would also benefit Vancouver, would target both those who buy expensive homes using foreign income and domestic investors who have “aggressively evaded taxes,” Gordon wrote in the report.

“The surtax would make no distinction based on nationality or anything along those lines. Instead, the premise would be that ownership is encouraged for anyone earning income in Canadian labor markets, while ownership based on foreign wealth or illicit income is discouraged (or forced to pay a penalty),” reads the study.

READ MORE: Failed the mortgage stress test? Alternative lenders await — at a price

The Ontario government said last week it is considering a surcharge for foreign buyers but ran into opposition from TREB, which argued that worries over the impact of foreign capital in Toronto real estate market have been “widely overblown.”

Data collected by condo-research firm Urbanation show that foreign buyers make up only 5 per cent of the demand for new condos in the Greater Toronto Area.

But Ontario does not collect data on the nationality and residency status of real estate buyers, a practice B.C. started last summer. The numbers there show that about 11 per cent of real estate transactions in Vancouver involved foreigners between June 10 and July 14. In nearby Burnaby and Richmond the share of foreign buyers reached 18 per cent.

The numbers dropped after the introduction of the foreign buyer’s tax, although they appear to be edging back up.

Still, in order to gauge the true impact of foreign capital on both the Vancouver and Toronto markets, the government should be matching land-title data with income tax data, Gordon told Global News. The first would reveal who did the buying. The second whether the buyer is paying enough income taxes to support the purchase.

International buyers can get around taxes targeted specifically at them by channeling the money through Canadian residents. Pairing purchase data with income tax data would capture both the true origins of capital and help spot tax dodgers, Gordon said.

Comments

Want to discuss? Please read our Commenting Policy first.