If personal finance questions were like pop songs, then How much do I need for retirement? would be at the top of the hit parade every single year.

MORE: Sign up for the Money123 newsletter

Canadians have started losing sleep over it. Low interest rates not only made it easy to borrow money, they also made it frustratingly difficult to grow your savings and investments. It doesn’t help — when it comes to retirement money, at least — that we’re living longer and longer, which means we’ll have to stretch our dollars further and further.

So how much money do you really need for retirement? And are you saving enough to get there?

Of course, there is no one-size-fits-all strategy when it comes to figuring out your financial needs in old age. But looking at a concrete example can be a big help.

SIGN UP FOR ERICA ALINI’S UPCOMING WEEKLY MONEY NEWSLETTER:

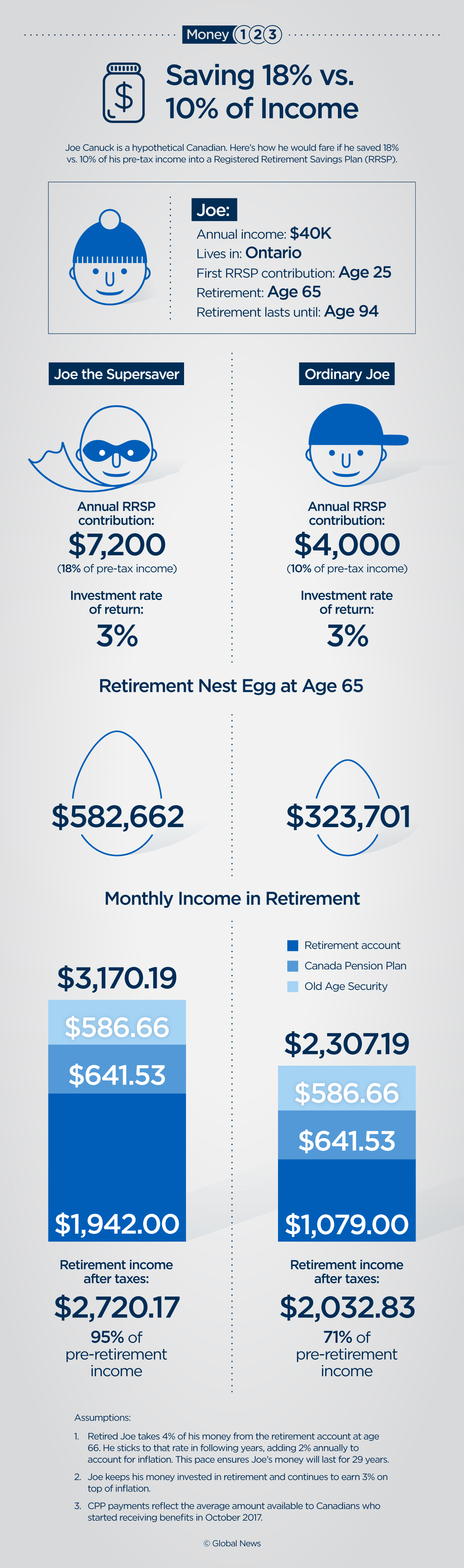

Meet Joe Canuck

Let’s look at Joe Canuck, a hypothetical Canadian facing the familiar retirement conundrum.

Let’s say that Joe lives in Ontario and makes $40,000 a year, an amount that will keep roughly steady throughout his working life (for the purposes of this example, we’re not going to worry too much about inflation). Joe’s take-home pay is $2,853.33 per month. He starts making contributions to a Registered Retirement Savings Plan (RRSP) account at age 25 with a plan to retire at 65.

READ MORE: Money123 – the easy way to be smart with your money

In our first scenario, Joe manages to squirrel away an impressive $7,200 every year, equivalent to 18 per cent of his earnings and the maximum annual contribution he can make to his RRSP. He also invests his savings, earning an average yearly return of 3 per cent.

In our second scenario, Joe puts away a respectable $4,000 a year, or 10 per cent of his pre-tax income, into his RRSP. He also earns a 3 per cent yearly return on his RRSP investments.

READ MORE: Plan to use your RRSP for a down payment on a house? Don’t do it.

Here’s how Joe ends up saving 18 per cent vs. 10 per cent, according to numbers provided by Robb Engen, a fee-only financial planner based in Lethbridge, Alta., and co-author of the popular personal finance blog Boomer and Echo.

Lessons from Joe Canuck for your retirement

Your life probably doesn’t look like Joe Canuck’s, but there are a few lessons that can be drawn from his example, Engen said.

The first step when calculating how much you’ll need is estimating your future expenses in retirement

There are many rules of thumb out there when it comes to retirement. You may have heard that you should be saving 10-15 per cent of your pre-tax income, or that you’ll need around 70 per cent of your income when you stop working.

In our example, Joe Supersaver ends up with an amount equal to almost all of his pre-retirement earnings by saving 18 per cent of his earnings.

Get weekly money news

“Joe the Supersaver is going to be fine,” Engen said. That’s true especially given that he will no longer have to set aside over $7,000 a year for retirement, which will significantly boost his disposable income. Instead of maximizing his RRSP contribution, post-retirement Joe Supersaver will likely have room to save up for routine big-ticket expenses like a new car or roof, and, maybe, a few vacations.

READ MORE: Looking for last-minute RRSP advice? Warren Buffett thinks you should buy index funds

Ordinary Joe, on the other hand, will likely be on pretty thin ice. Not having to save for retirement will free up a little over $300 a month in his cash flow compared to when he was working. That’s not much of a cushion to deal with unexpected costs, Engen said.

The 70 per cent income-replacement ratio doesn’t work well for someone with a relatively low income like Joe. For others, though, that may be plenty, especially at higher income levels.

READ MORE: Why maximizing your RRSP contribution simply isn’t enough

The bottom line is that the crucial ballpark figure you need to have before doing any retirement math is an estimate of your retirement living expenses, Engen said.

Once you have that, here’s a back-of-the-envelope calculation you can do to figure out the size of your nest egg.

- Multiply your annual retirement expenses by 25. For example, if you think you’ll need $40,000 a year in retirement, then you’d have to save $1,000,000.

- Subtract a conservative estimate of the government benefits you’ll be receiving, such as those from the Canada Pension Plan (CPP) and Old Age Security (OAS), which may provide you with an additional $10,000 or $15,000 per year, said Engen. That means your nest egg would only have to be $625,000-$750,000.

- The next step is calculate the savings rate that will get you there. You may not be able to save that much when you’re just starting out and may want to revise your estimates several times as your circumstances change, Engen said. And, naturally, a financial adviser can give you more nuanced guidelines.

WATCH: What you need to know about RRSPs

Do include CPP and OAS in your math

“One of the biggest mistakes people make is not counting on CPP and OAS,” Engen said. Those government benefits make a big difference to Joe’s bottom line in retirement, and there’s no reason to exclude them from your calculations.

“Some people are worried that CPP is a piggy bank the government can raid to pay down debt,” Engen said. But that’s not the case. CPP funds are held separately from general revenue and managed by an independent body. “CPP has been actuarially tested and is sound for the next 75 years,” Engen added.

Still, another common mistake is to assume you’re going to get the maximum CPP payout. That requires you to have worked for 40 years at relatively high income, among other things. A better rule of thumb figure is to look up the average payment going out to new retirees, which you can easily find online, Engen said. That’s the CPP figure we used for Joe.

READ MORE: How not to lose your RRSP money, in Ryan Gosling GIFs

As far as OAS, the money does come from the same pool from which the government funds everything else, but eliminating the program would be politically treacherous, to say the least, for any government, Engen told Global News.

WATCH: Experts give advice on saving more for your RRSP

- Adjustable rate cap part of ‘care-first’ auto insurance model coming to Alberta

- Carney, Smith confirm energy announcement coming Friday

- ‘Extraordinarily innovative’ oil sector can weather increased carbon price: ATCO CEO

- Trans Mountain and its federal parent see case for Ottawa owning pipeline for good

The road to retirement is much harder if you don’t invest or avoid the stock market

In both of our scenarios, Joe is investing his savings, including after retirement. His 3 per cent return is a very realistic goal for someone who puts half of their savings in stocks and half in less risky investments like bonds and Guaranteed Investment Certificates (GICs), according to Engen. But it will be very hard to achieve your retirement goal if you’re avoiding the stock market entirely, he added.

READ MORE: Thinking of putting your RRSP contribution into GICs? Stop and read this first

You can still make it if you work longer

To catch up with Joe Supersaver, Ordinary Joe would have to work until age 75. At that point, he would have saved $482,000 and could safely withdraw some $27,800 per year, roughly the same as Joe Supersaver, who has already been retired for 10 years, according to Engen.

That may be of some comfort to millennials who feel like they can’t possibly squeeze an 18 per cent RRSP contribution out of their budget but don’t mind the idea of working well after age 65.

READ MORE: Boomers, gen-X, millennials: How living costs compare then and now

Still, starting to save early pays off

In both scenarios, Joe starts saving at age 25, which is “a very good start,” Engen said, even with a saving rate of 10 per cent. For simplicity, our scenarios assume Joe’s earning stays constant. In real life, your income will probably go up as you advance in your career, giving you an opportunity to bump up the amount you squirrel away every month. If you start saving at 40, it’s harder to catch up.

WATCH: Investing tips for RRSP season

How to avoid running out of money

In our scenarios, Joe’s money lasts until he’s 94. Considering that the life expectancy for men in Canada is just over 86 years, Joe will probably be OK. But what if he were to live until 95 — or make it to 100?

If you’re healthy and you feel like you could become a centenarian, one option is to postpone taking CPP and OAS, Engen said. If you delay CPP until age 70, for example, you can count on a payout boost of 36 per cent for life.

Another option is to take out an annuity, an insurance contract that guarantees a fixed monthly payment after a certain age. While some people think annuities are a bad deal because the payment isn’t necessarily adjusted for inflation, the prospect of a regular cheque does have its upsides, Engen said.

And if you’re worried that runaway medical expenses in old age will chew away at your nest egg faster than you planned for, consider long-term care insurance, Engen told Global News.

READ MORE: Financially helping adult kids may just be a return to an old normal

Be aware that RRSPs aren’t the only saving option for retirement

The final takeaway for Engen may come as surprise to many: Joe likely shouldn’t have been saving in an RRSP at all. Given his level of income, a Tax-Free Savings Account (TFSA) might have been a better option, he told Global News.

We’ll look at how Joe would have fared with a TFSA in our next installment of the Money123 series on Tuesday.

TO CELEBRATE THE LAUNCH OF THE MONEY123 NEWSLETTER WE’RE GIVING OUT $500:

Disclaimer – Global News provides the information contained in this series for informational purposes only. It is not to be used or construed or relied upon as financial, legal, tax, accounting or other professional advice or recommendations regarding the suitability, profitability or potential value of any particular investment, product, service or course of action. The information provided does not replace consultations with professional advisors and it is recommended that you seek appropriate independent advice from qualified professional advisors before making any financial or other decisions. Global News shall not be responsible or liable in any way for any loss or damage directly or indirectly incurred as a result of, or in connection with, the use of such information by you.

Comments

Want to discuss? Please read our Commenting Policy first.