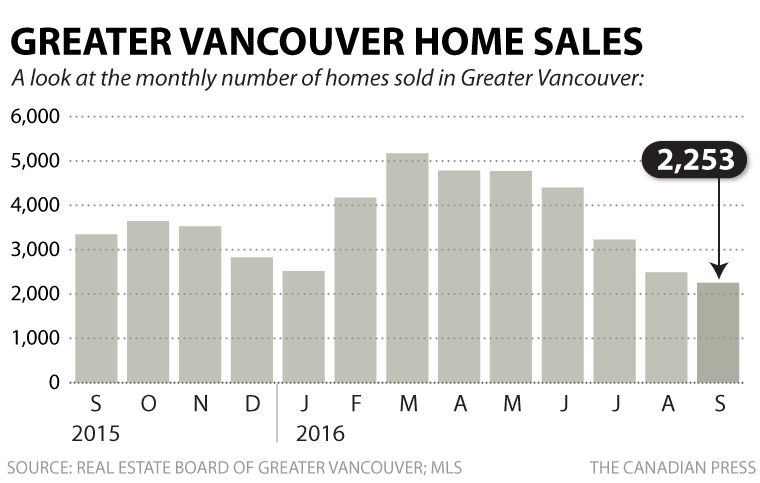

VANCOUVER – Home sales in Metro Vancouver plunged by 32.6 per cent last month compared to the same month last year, the city’s real estate board said Tuesday, a sign that one of the hottest real estate markets in the world may be rapidly cooling down.

The Real Estate Board of Greater Vancouver said there were 2,253 homes sold last month, a steep drop from the 3,345 home sales recorded in September 2015.

Last month was the second month that a 15 per cent tax applied to foreign buyers of property in the city.

READ MORE: Vancouver tops housing ‘bubble risk’: report

“There’s uncertainty in the market at the moment and homebuyers and sellers are having difficulty establishing price,” said real estate board president Dan Morrison in a news release.

The composite benchmark price for all residential properties was $931,900, a 28.9 per cent increase compared to the same month last year but a 0.1 per cent decline compared to August 2016.

The marked drop in the number of homes sold last month follows a 26 per cent year-over-year decline in August.

READ MORE: Surge in foreign buying in Metro Vancouver real estate market days before new tax took effect

Morrison said there is more demand for condominiums and townhomes than detached homes, supporting some analyst predictions that there’s still interest among first-time buyers to get into the Vancouver market.

Concerns have intensified about the city’s real estate sector. Some experts have predicted it is prone to a sharp correction.

Last week, Swiss bank UBS released a report that said the city had the greatest risk of a housing bubble when compared to 17 other high-priced large markets including London, New York and Sydney, Australia.

WATCH BELOW: Many observers were watching the month closely after the provincial government implemented a foreign buyers’ tax, but one local realtor says the market was already slowing down before the change in legislation.

- B.C. Conservative leader pledges not to ‘reopen the abortion debate’

- A look inside the now-sidelined ‘floatel’ meant to house LNG workers near Squamish

- South Surrey restaurant forced to close after suspicious fire, more criminal acts reported

- Canfor to shutter B.C. sawmill, curtail Prince George pulp mill

Comments