Evidence from realtors and MLS data is showing the Vancouver real estate market is in the midst of a major slowdown, with prices dropping and sales plummeting, but some experts say it’s too soon to tell.

While August is typically one of the slowest months for real estate transactions, MLS sales data from the first two weeks of the month shows what many have been hoping for during the past few years of escalating prices.

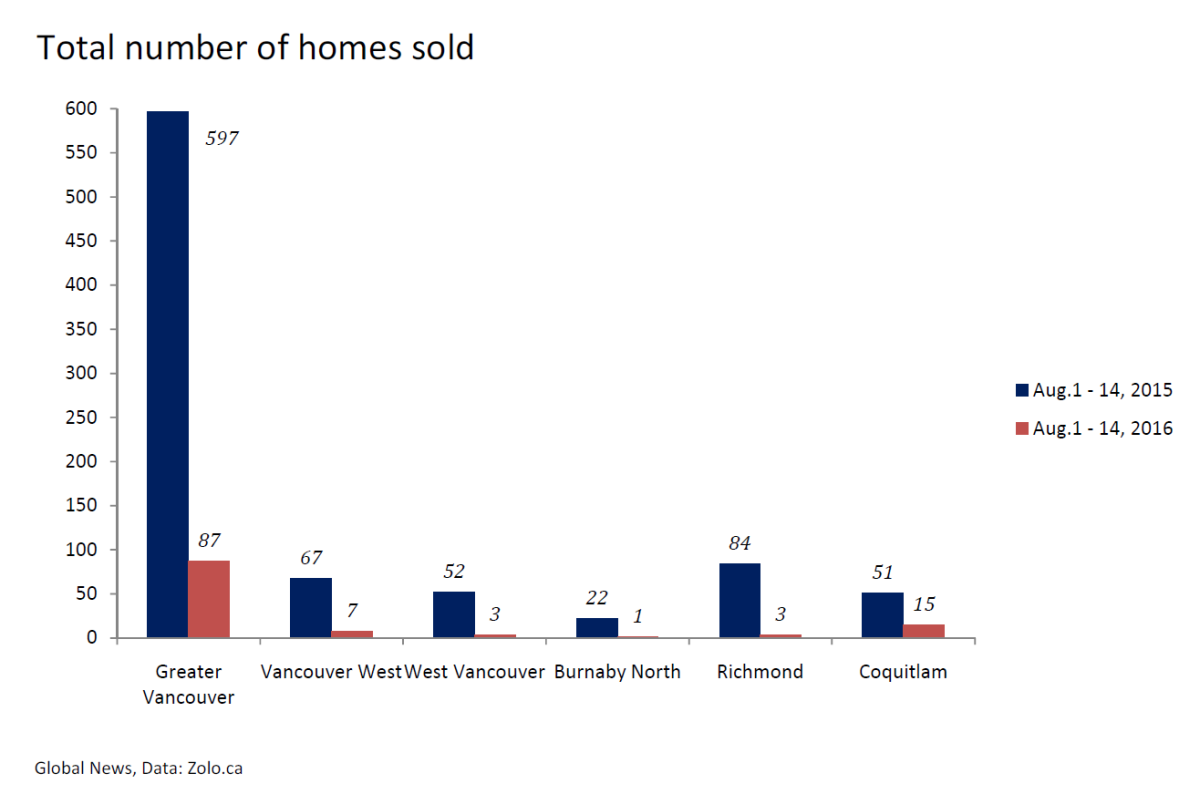

There were only three home sales in West Vancouver between Aug. 1 and 14 this year, compared to 52 during the same period last year. That’s a decrease of 94 per cent.

The numbers come from long-time realtor Brent Eilers, who’s been tracking the data with the same system since he joined the business in 1983. He studied MLS listings to count how many homes were sold so far this month.

“It’s pretty tough to go from 52 to three and pretend things are fine,” said Eilers. “That is a pattern that can’t go ignored.”

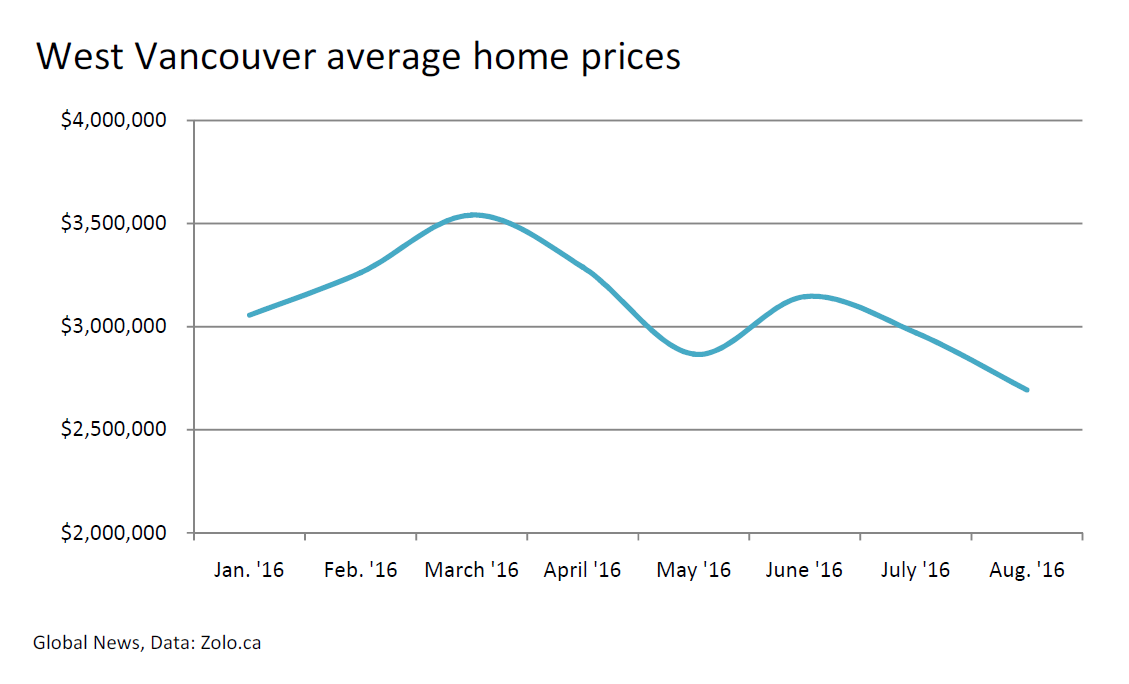

Eilers says he’s been warning of a real estate slowdown for at least a year due to the region’s unsustainable and unsupportable prices. West Vancouver, where he does a large part of his business, had a benchmark detached home price of almost $3.4 million in July according to the Real Estate Board of Greater Vancouver (REBGV).

The median household income in the region was $84,345 in 2011, according to the District of West Vancouver.

“The market in West Van is up 450 per cent since 2001. So is everyone making 600 per cent more income than they were so they can pay their taxes and buy their houses? Of course not. So how has this inflation been financed? By offshore money and record debt.”

And while Eilers says the slowdown is at least partly due to the implementation of the Metro Vancouver foreign buyer tax on July 25, which has caused a firestorm of anecdotal evidence saying it has killed the housing market, he adds sales were dropping even before the tax.

According to the data, July was another slow month in West Vancouver with only 44 sales, down from 80 in 2015. June saw 74 sales, also down from 102 the year before.

The pattern has left the market “devastated” according to Eilers.

But experts are warning that two weeks of data isn’t enough to ring the alarm bells.

Andy Yan, acting director of The City Program at Simon Fraser University, says we need more time.

“It’s really hard to say if it’s just cooling off. It could be that everybody who could or would buy at those really high prices a couple months ago are now already in, and now we just really see how the market is retracting itself,” he said.

- Posters promoting ‘Steal From Loblaws Day’ are circulating. How did we get here?

- Canadian food banks are on the brink: ‘This is not a sustainable situation’

- Is home ownership only for the rich now? 80% say yes in new poll

- Investing tax refunds is low priority for Canadians amid high cost of living: poll

Prices going down

Earlier this month, the REBGV released its statistics for the month of July, saying the data showed the market had slowed down to “normal levels.” But one thing missing from the data was evidence of any price decrease. Fortunately for buyers, real-time data proves otherwise.

READ MORE: Vancouver real estate market slows in July to “normal” levels

Zolo, a Canadian real estate brokerage, keeps track of MLS home sales in real time and reports prices as an average rather than the “benchmark price” used by the REBGV.

It currently shows a major correction underway in most Metro Vancouver markets.

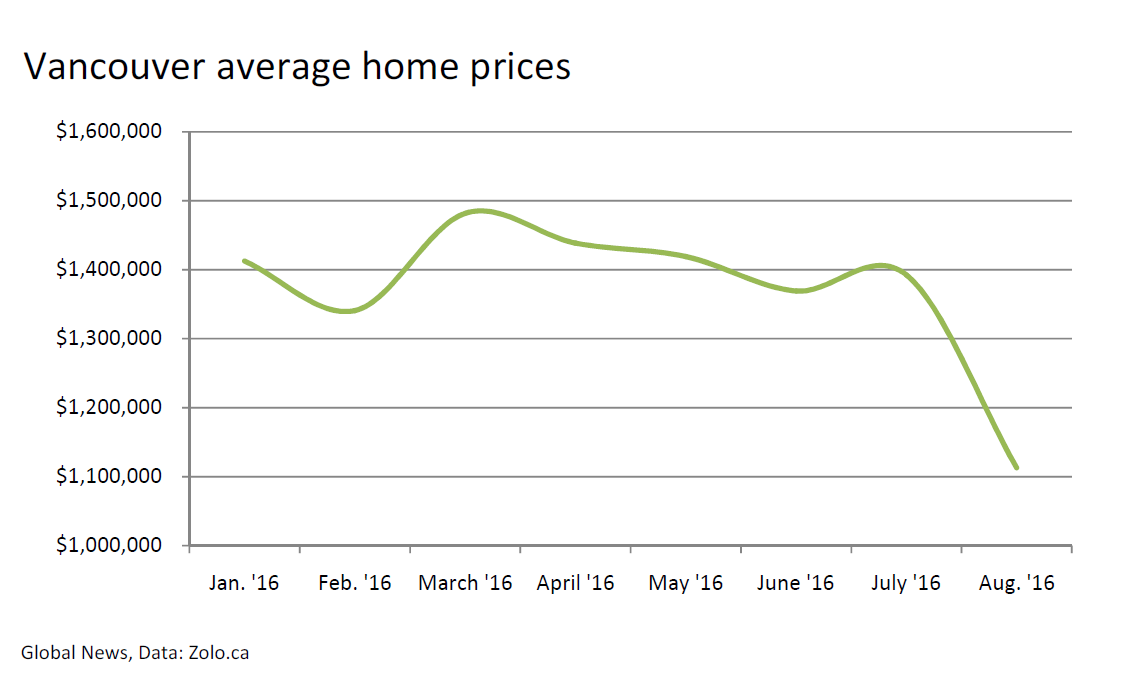

According to the website, the city of Vancouver currently has an average home price of $1.1 million, down 20.7 per cent over the last 28 days and down 24.5 per cent over the last three months.

The average detached home is $2.6 million, down seven per cent compared to three months ago.

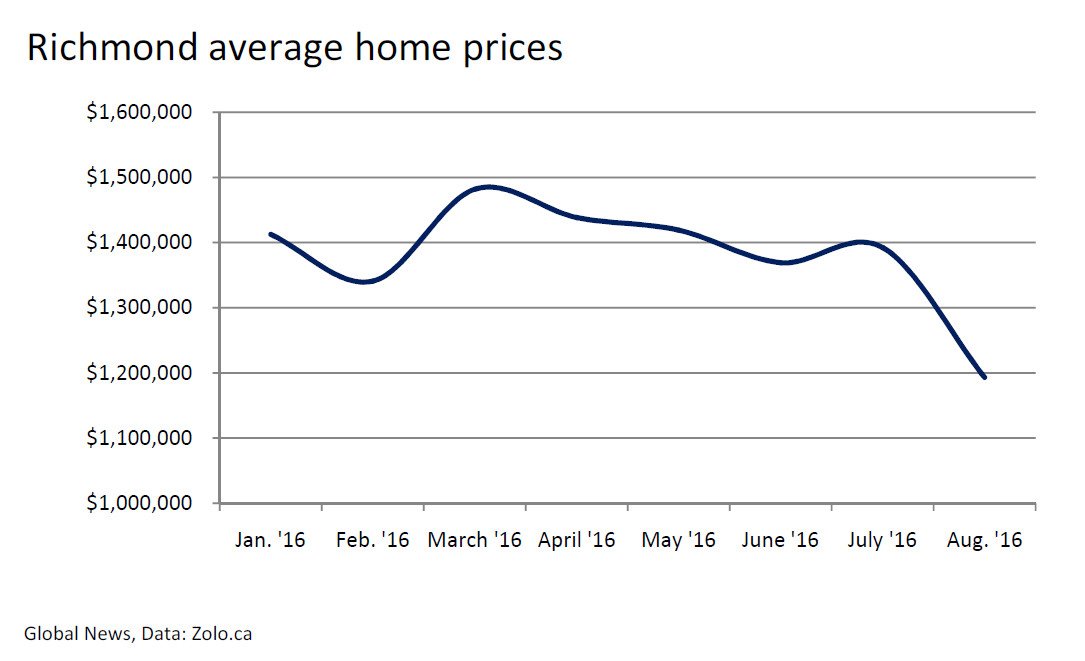

Richmond is no different. Zolo CEO Barry Allen says the market in Richmond has “gone off a cliff” with the average home now priced at $779,000, down 20.7 per cent from three months ago and 17.6 per cent from last month. Detached homes in Richmond took the hardest hit compared to other markets with a 10 per cent price correction over the last three months down to $1.7 million.

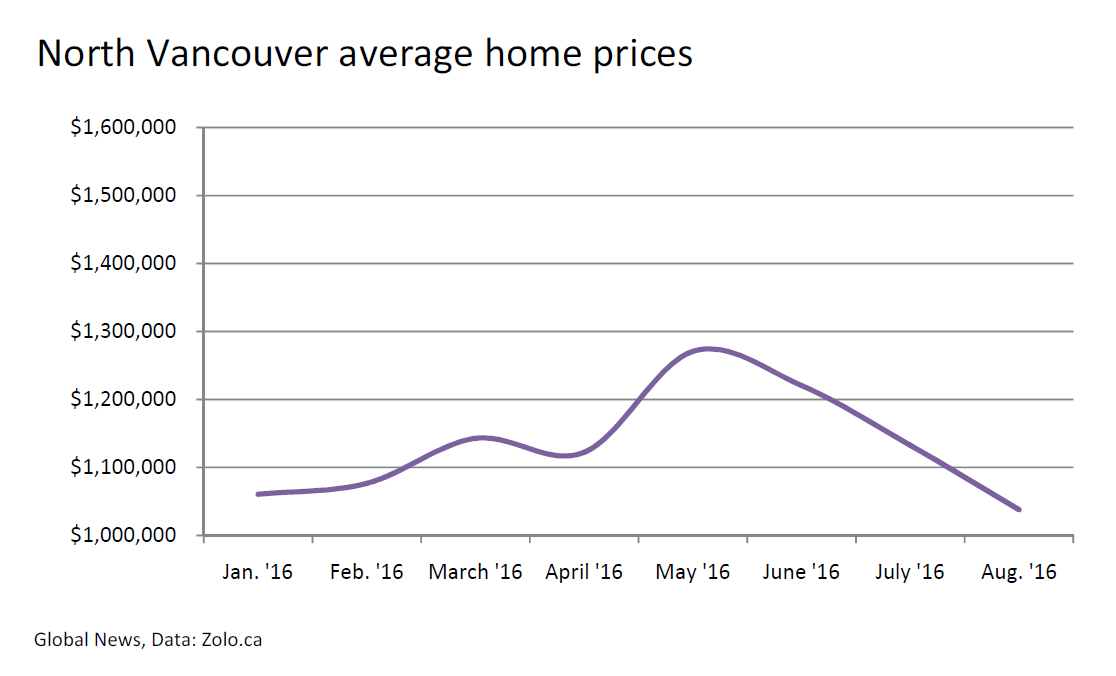

North Vancouver detached homes fell 10 per cent in price in three months down to $1.8 million. Their average home price for all properties fell 17.3 per cent in that time period to $1 million.

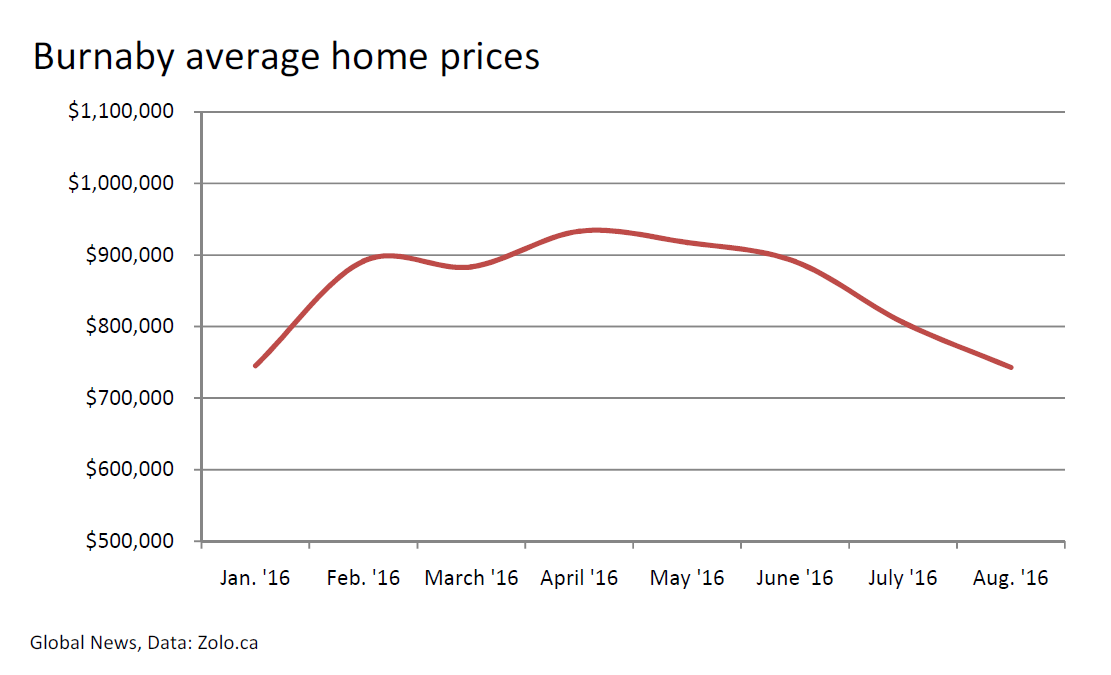

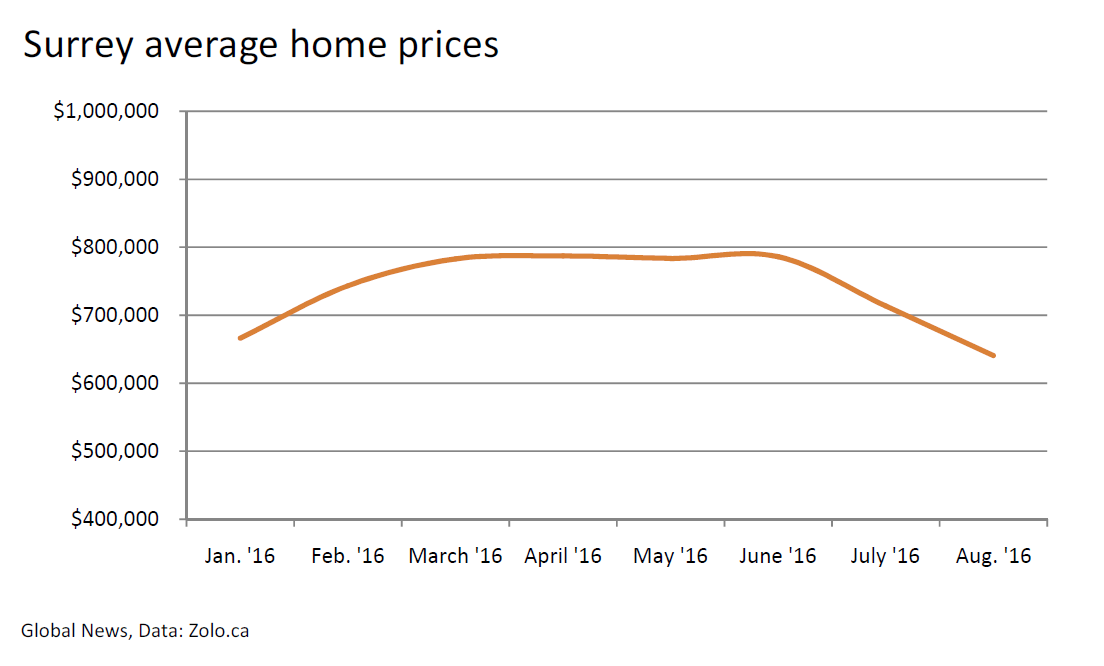

It’s more of the same in Burnaby and Surrey.

GALLERY: See just how much prices have dropped in key Metro Vancouver markets:

However tantalizing the drop in price may be, economists and experts warn that using averages in real estate prices is inherently problematic.

“That’s a really bad idea,” said UBC economist Tsur Somerville, who adds that the drop in average prices may be due to a drop in high-end home sales.

“Averages are always tricky to use, because when you have sales at the high end they have a way of skewing the value of homes that are sold, and that’s really particularly the case in Vancouver,” said Yan.

Allen says their data showed the market had already started to turn before the foreign buyer tax.

“It’s only slowing down at the top where there is uncertainty,” he said.

And that uncertainty is “diabolically dangerous,” according to Eilers, who has sold real estate during four different correction periods in Vancouver.

“When the market changes, it typically changes over night or within a couple of weeks, but it often takes two to three months for everybody to figure it out. That’s why it can be so scary,” he said.

A strong price correction often takes months to appear because sellers are unwilling to lower their prices until they have to.

According to the realtor, often sellers have their houses appraised months before they put them on the market, meaning in the climate we are currently witnessing, sellers are expecting to list their homes at record-high prices, even though the number of sales and listings indicate prices should be lowering.

“Typically what happens when the market starts to flip is all the buyers go into hibernation and all the listings come on. What are the odds on getting that seller to price his home at a fraction of where the market is now? It’s zero,” Eilers said.

What causes prices to fall is “urgency, anxiety, and fear,” according Eilers. He says a climate of financial overexposure, a treadmill of buying and selling and flipping homes, owning multiple properties, and buying before selling will test how long sellers can hold on without selling in desperation.

He points to the 1980 housing crash that dropped prices by 40 to 60 per cent within a year and took six years to recover.

“So your $2 million house became $800,000 in five months. There’s a lot of economists and a lot of wise people that believe that our financial structure is much closer to that structure from a corrections point of view,” Eilers explained.

The Bank of Canada recently warned that those invested in the Vancouver housing market are particularly vulnerable to a price correction due to the large share of “highly indebted households.”

And the Canadian Mortgage and Housing Corporation increased Vancouver’s risk rating to “high,” due to “evidence of problematic conditions” including price acceleration and overvaluation.

Lots selling, few buying

Zolo’s CEO says the foreign buyer tax has certainly stopped speculative buyers. This has caused many other buyers to take on a “wait and see” approach, which has essentially frozen the market.

East Vancouver’s Nina MacDonald echoes that belief telling Global News she hasn’t had any nibbles on her $1.28 million, 59-year-old bungalow on Napier Street that she’s owned for over 20 years. She’s even cancelled an upcoming open house because she felt like it would be pointless.

She initially wanted to sell because the real estate windfall would allow her to purchase a turnkey property and pay the down payment on houses for her grandchildren.

“I went from having a phone call every day [from realtors] to not having any,” she said.

Global News obtained MLS sales data from several key Metro Vancouver markets and found the number of homes sold during the first two weeks of August in Greater Vancouver dropped by 85 per cent on average.

Richmond experienced a 96 per cent drop in the number of sales and Burnaby North fell by 95 per cent. Vancouver’s West Side, West Vancouver, and Coquitlam also took major hits.

While the number of sales has been dropping for a couple months, August is a particularly difficult time to predict an ongoing trend as the market is generally less active, according to Somerville.

Yan agrees it will take at least three months of solid data to prove a pattern exists.

“You need a much larger data frame to say ‘aha, here’s a trend’ or ‘no, there’s no trend.'”

Somerville also points out that the timeline of the foreign buyer tax may have caused data distortion for this month.

“There’s all these sales that got rushed to be done before Aug. 2 that would have normally taken place in August, then of course they’re going to be lower,” he said.

But regardless Somerville said, “declines in sales are usually the precursor to the market slowing or even turning.”

News of the foreign buyer tax has spread to China, where Chinese real estate website Juwai now promotes other Canadian cities as foreign capital destinations.

The website used to promote Vancouver as one of the best places for wealthy Chinese to invest, but has now switched to publicizing Calgary and Alberta due to the tax.

READ MORE: 90% of Metro Vancouverites support foreign buyer tax

Juwai says Calgary offers “better value for money when compared with the inflated housing prices in Vancouver.”

Eilers says both the foreign buyer tax and the ensuing market uncertainty is a double whammy that will keep investors away, but it will likely take until October to see just how much of an effect it has on prices.

NDP MLA David Eby says the tax has caused a lot of people to hit the pause button on buying homes, but all those people might come back into the market in September.

Despite his reservations on how the tax was implemented – he would have preferred an incrementally increasing tax – he says a market slowdown is good news.

“A lot of people have said to me quietly that they hope there is a substantial housing crash.”

Yan admits the data could be pointing toward a downward trend, but it could also be a minor blip in Vancouver’s hot housing market.

“It’s part of what you’d expect out of a cycle, in terms of rapid expansion and now a small contraction. Is it an indication of a bubble bursting? Wouldn’t be able to tell you.”

Comments