Home sales continue to boom more than expected in the country’s two hottest markets, the national association of real estate agents said Monday morning.

But looking out into 2015, momentum is expected to diminish in Vancouver and Toronto, leading to a leaner sales environment overall.

The reason: homes in the country’s two biggest markets are climbing out of reach for most.

“Sales nationally are still expected to peak this year,” the Canadian Real Estate Association said. “In British Columbia and Ontario, activity is expected to be held in check by eroding affordability.”

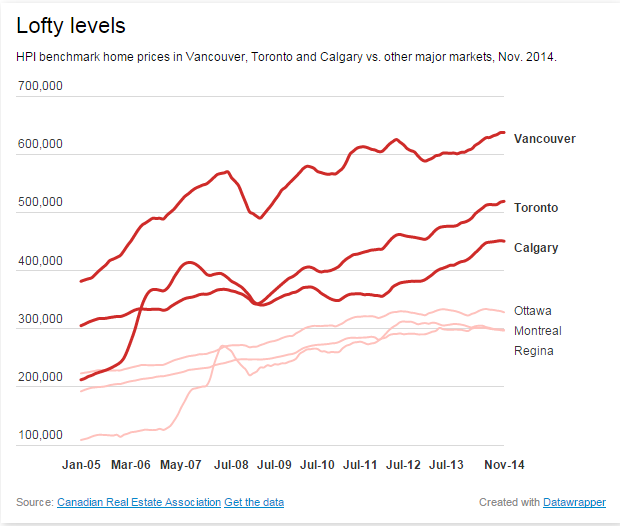

In Toronto and Vancouver, the two largest markets in the country, home prices inflated by 7.3% and 5.9% respectively in November.

Those two markets, which account for more than half of all housing activity tracked by CREA, helped stoke average home prices at the national level up 5.7 per cent last month versus November 2013, CREA said, to $413,649.

“The national average home price continues to be raised considerably by sales activity in Greater Vancouver and Greater Toronto, which are among Canada’s most active and expensive housing markets,” the association said in a release.

Get weekly money news

Excluding the two markets, the average price across Canada is a more modest $331,743, up 5 per cent.

Bank of Canada warning

Particular attention is being paid to the housing market in light of last week’s comments from the Bank of Canada suggesting homes may be overvalued by as much as 30 per cent.

The central bank said it doesn’t see a crash though because the economy is gaining momentum.

MORE: Here’s what’s keeping Canada’s central bankers up at night

Still, that could mean pressure to lift interest rates – a move that would make payments more costly for some over-leveraged home buyers in major markets like Toronto, Vancouver, and Calgary who’ve taken on big home loans at rock-bottom rates. The Bank of Canada said about 12 per cent of Canadian households held a risky amount of debt.

Capital Economics said booming real estate markets in Alberta are poised to see a slowdown as energy prices fall, as well.

“The slump in world oil prices will hit Western Canada hard, and it will only be a matter of months before housing activity and prices begin to fall significantly in Calgary,” the Toronto-based researcher said.

Comments