Can Canadians retire?

If you ask the people whose job it is to sell you savings, they’ll suggest putting 10% of your annual income toward registered retirement savings plans.

But very few Canadians do.

We mapped RRSP contributions for every urban neighbourhood in the country using tax return data for 2011, the most recent year available. What we found is fascinating – and potentially worrisome for policy-makers eyeing an ageing population.

Most don’t contribute: 5.9 million people, or 23% of tax filers, reported some level of RRSP contribution. That works out to just under a third of Canadians aged 25-64.

Those that do, don’t contribute much: The median RRSP contribution was 10% or higher (among the minority who made contributions at all) in only 55 of Canada’s 4,995 census tracts. (Nationally, the median contribution of $2,830 was about 5% of median income.)

And they contribute less than ever: Median RRSP contributions have fallen since 2001, when the median for all filers was $3,208.

The reasons will vary from person to person. Some save for retirement in other ways, like real estate or a tax-free-savings account. Some are ignoring the issue.

Others, our data implies, simply can’t afford it. Not surprisingly, both median RRSP contributions and the percentage of tax filers contributing match the pattern of high-and low-income census tracts: Richer neighbourhoods, in short, have more people investing more money.

The data comes from tax returns from 2011 (the most recent year available) supplied to Global News by Statistics Canada.

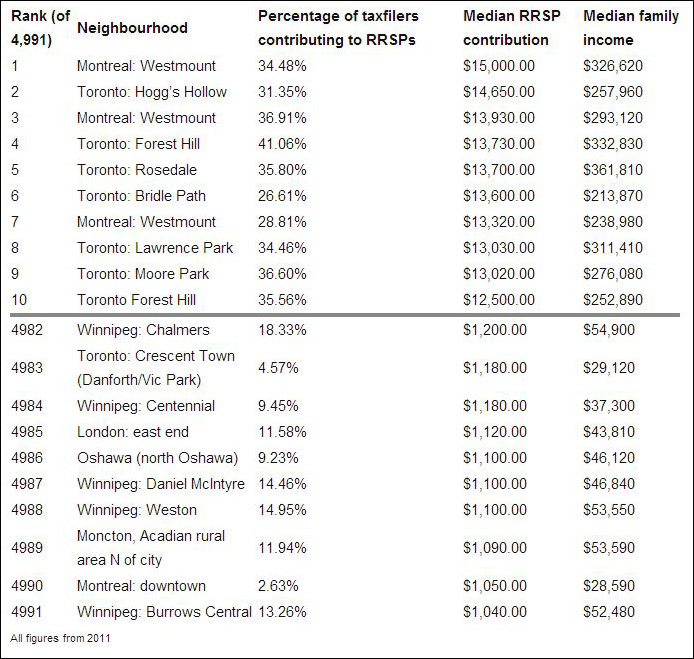

Adjusted for the presence of institutions such as retirement homes and universities, here are Canada’s top and bottom 10 tracts by median RRSP contribution:

There’s some variation between men and women: In 2011, somewhat more men make RRSP contributions than women (53:47), though somewhat more women than men filed tax returns (52:48). Men save somewhat more ($3,360 median vs. $2.390).

In 2001, the median contribution for men was $3,702, and for women, $2,715 (adjusted for inflation to 2011 values).

But in general, men and women had more pronounced proportionate differences in RRSP contributions in rural areas.

Interactives: Use the drop-down menus to select what you want to explore; click a census tract for details. Double-click to zoom; drag to move around.

Toronto’s median RRSP contribution is higher than the Canadian median – but just as with wealth, the city has polarized pockets of poverty in its inner-suburbs where RRSP savings drop.

The median Winnipeg RRSP-saver contributes less than the median Canadian – but participation is still fairly robust across much of the city.

Median Edmonton RRSP contributions sit slightly above their Canadian counterparts, but the patterns closely follow patterns of wealth and poverty:

Calgary boasts a clear east-west divide when it comes to RRSP contributions – the west gives more, and more of its population gives. But the city’s median RRSP contribution is well over Canada’s median.

In Montreal, as well, wealth polarization appears to correlate with RRSP participation. When it comes to how much the median person gives, Montreal neighbourhoods are among both the top and bottom in Canada (albeit more of them are closer to the top).

Greater Vancouver’s median contribution is higher than the Canadian median. But it drops precipitously when you leave the city proper for Surrey and Langley. Interestingly, Vancouver is also the only major city in the country where personal debt levels continue to grow – by 7 per cent between the end of 2012 and 2013, to $41,077.

Whether it’s belt-tightening or the emergence of other options, Canadians seem to be losing interest in RRSPs.

There could be two more pointed reasons, however: Shrinking incomes and expanding debt.

Households squeezed on both sides have less for retirement savings, experts say.

Shaun Darchiville, an investment adviser with Desjardins Securities, has been in the business of planning people’s retirements for the better part of three decades.

He says he’s seen a “dramatic decline” in how much average Canadians are setting aside in recent years. “These are people with decent jobs, professional jobs, two incomes in the household, a couple of children,” he said.

READ MORE: Most opt to skip RRSPs this year to pay down debt

One factor is that life just get pricier, well beyond the official inflation rate of 1.5%.

“Insurance costs are up in some cases by 25, 30 per cent. Utility costs continue to go up, electricity costs continue to go up, natural gas is nearing a recent high again,” Darchiville said. “And people are feeling that pressure.”

And then there’s the debt factor.

While rock bottom interest rates have made monthly payments manageable for many, the carrying costs on the average home loan have climbed to an uncomfortably high 43 per cent of the average home owner’s family income, according to RBC.

That credit binge has spilled into everything from auto loans to elevated levels of credit-card usage – spurred on by loyalty programs enticing consumers to put down plastic instead of cash for almost any purchase— student loans, and myriad of other outlets. The average Canadian’s consumer debt now sits at $27,368, and TransUnion vice-president of analytics Thomas Higgins doesn’t see it dropping.

“There hasn’t been any indication that there’s going to be any consistent and ongoing decrease in this number,” he said. But incomes haven’t really been keeping pace with the debt.”

Comments