Whether you pay by debit, credit, mobile wallet or smartwatch, speed and convenience are driving the way Canadians are choosing to pay, but it all comes with a price — cash as a payment option is steadily declining.

The spike in digital adoption was fuelled in part by the pandemic, as Canadians turned to virtual, mobile and online payment transactions in record numbers.

In Canada, credit cards remained the top method of payment followed by debit, with Canadians reiterating ease, speed and convenience as the reasons they opt for plastic over cash, according to Payments Canada’s most recent report.

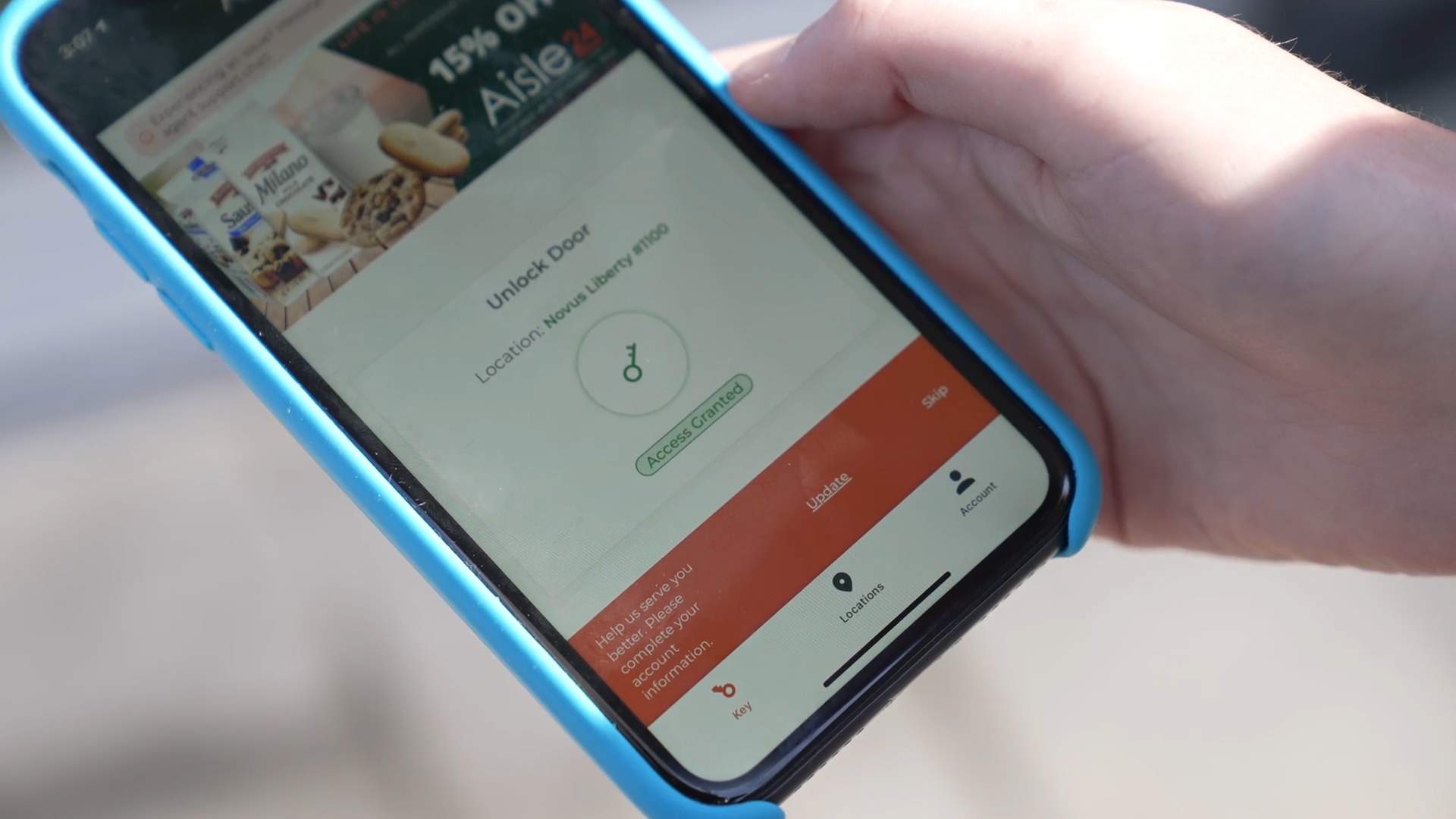

With Canadians opting for more contactless, digital forms of payments, more doors open for newer, more futuristic in-store shopping experiences, like Aisle 24.

Aisle 24 is a cashierless, cashless, small-format grocery store in Canada, with 15 locations across the country and 75 franchises granted.

The way Aisle 24 works is simple: You take a minute to sign up for an account via its app, use the app to gain entry into one of its stores, shop for what you need, then checkout at a self-serve machine.

“We built this convenience aspect that was totally unmanned and driven by technology,” says Marie Yong, one of the co-founders and the chief operating officer of Aisle 24.

Yong says Canadians are strapped for time, meaning ease and convenience are key.

A recent Global Payments Report projects that by 2025, cash will only make up three per cent of all point-of-sales transactions in Canada — one of the lowest cash payment rates in the world. Canada is one of the leading countries when it comes to going cashless.

”The reason why we accept tap and go, and mobile pay … is because that’s where the consumer market is going,” Yong told Global’s The New Reality.

“We have people coming into our stores with nothing but their phones or nothing but their watches because that’s the trend,” says Yong, adding that most customers are in and out of Aisle 24 within five minutes.

When asked about the cashierless aspect of Aisle 24, Yong says a part of the concept was inspired by her husband’s family.

She also says the stores have gotten positive comments for their cashierless, cashless concept, but just because they don’t have any cashiers, doesn’t mean they don’t have any employees. Staff go into the stores to restock and deliver items.

What also makes Aisle 24 unique is an artificial intelligence security system. Similar to Amazon GO, Aisle 24 has technology that cannot only tell who’s in the store, but the movement within the store, which comes in handy for things like product spillage.

“We can analyze all of these things through AI technology, so if accidents were to occur, we’re able to get notified in real-time,” Yong says. “And at that time, we have somebody on call that can help and alleviate the accidents to make sure they get cleaned up in a timely fashion.”

When it comes to customers simply wanting to void an item, whether it’s because they accidentally scanned it twice or changed their minds, customers are able to do that on their own.

Both the simplicity of new payment technologies and the shopping experiences they offer Canadians are helping to influence decisions to go contactless. In fact, a report by the Canadian Bankers Association says that in the next five years, tap-and-go payment will increase by 43 per cent.

So what does this shift away from cash say about our cultural and social behaviour?

“I don’t know if we often pause to think how strange it is to just stop in the middle of the street, pay a bill on your phone … while monitoring your investments. These are both characteristically modern experiences, but also very peculiar,” says Mark Hayward, associate professor in the department of communication and media studies at York University.

Hayward, who studies the cultural and social components of how people engage in everyday finance as well as how we live with technology, says part of Canada’s success with switching to contactless forms of payment is that we trust the technology.

“We have a highly centralized, stable banking sector,” Hayward says. “They were able to cooperate, to put in place an electronic transaction system, Interac.”

He added, “This meant that Canada was able to make a tremendous amount of advances in this particular area through the 1980s that put it further ahead than the United States or countries in Europe.”

The idea of a cashless society emerged in the middle part of the 20th century as a way to deal with the large volume of paper cheques that were used in everyday economic activities, Hayward explains.

“So a cashless society arrives as a way of addressing this very real, practical, administrative problem. There is too much paperwork to be done on time,” Hayward says. “Proposed at the time were a range of solutions from automated computerized banking processing, through to credit cards, on to what we now think of as debit cards.”

That means that what we think of as a cashless society today comes from that moment.

“It’s been reappropriated and used in all sorts of different ways and evolved over time, but that’s the first iteration of it.”

He also says that this transition in Canada mostly took shape from the 1950s to the 1980s.

There was something else that helped Canadians trust these new innovations: marketing, specifically the marketing to drive how cost-effective, easy and convenient these new technologies were.

For example, Hayward says the first automated banking machines were piloted by CIBC in 1969, but their adoption by the Canadian public was “intermittent.” By the early 1980s, when Canadians started taking on their first bank cards, as they were referred to then, there was a huge marketing push for ABMs.

In fact, in the mid-1980s TD signed on singer Johnny Cash to help with the campaign.

“And it was this way of making this new, strange thing more familiar to people,” Hayward says.

But in 2022, Hayward believes there should be conversations emerging about Canadians’ advancement towards cashlessness, whether it’s the social and cultural bonds that we grew up on, such as putting a $20 bill in a birthday card, to now sending an e-transfer, or even questioning who would have access to new financial technologies.

“We can think about this in terms of older users who don’t want to use new technology. We can think about this in terms of unhoused people who may not have bank accounts for whom access to digital commerce may be very difficult.”

Hayward says a cashless society isn’t just about the selling and purchasing of items, but it’s a much broader question about caring for everyone around us and making sure everyone has equal access to services.

“People focus on big flashy changes, but this is one of those cases where I really do think that it’s about saying, let’s have this debate and this discussion. It is an ethical question. It is a social question.”

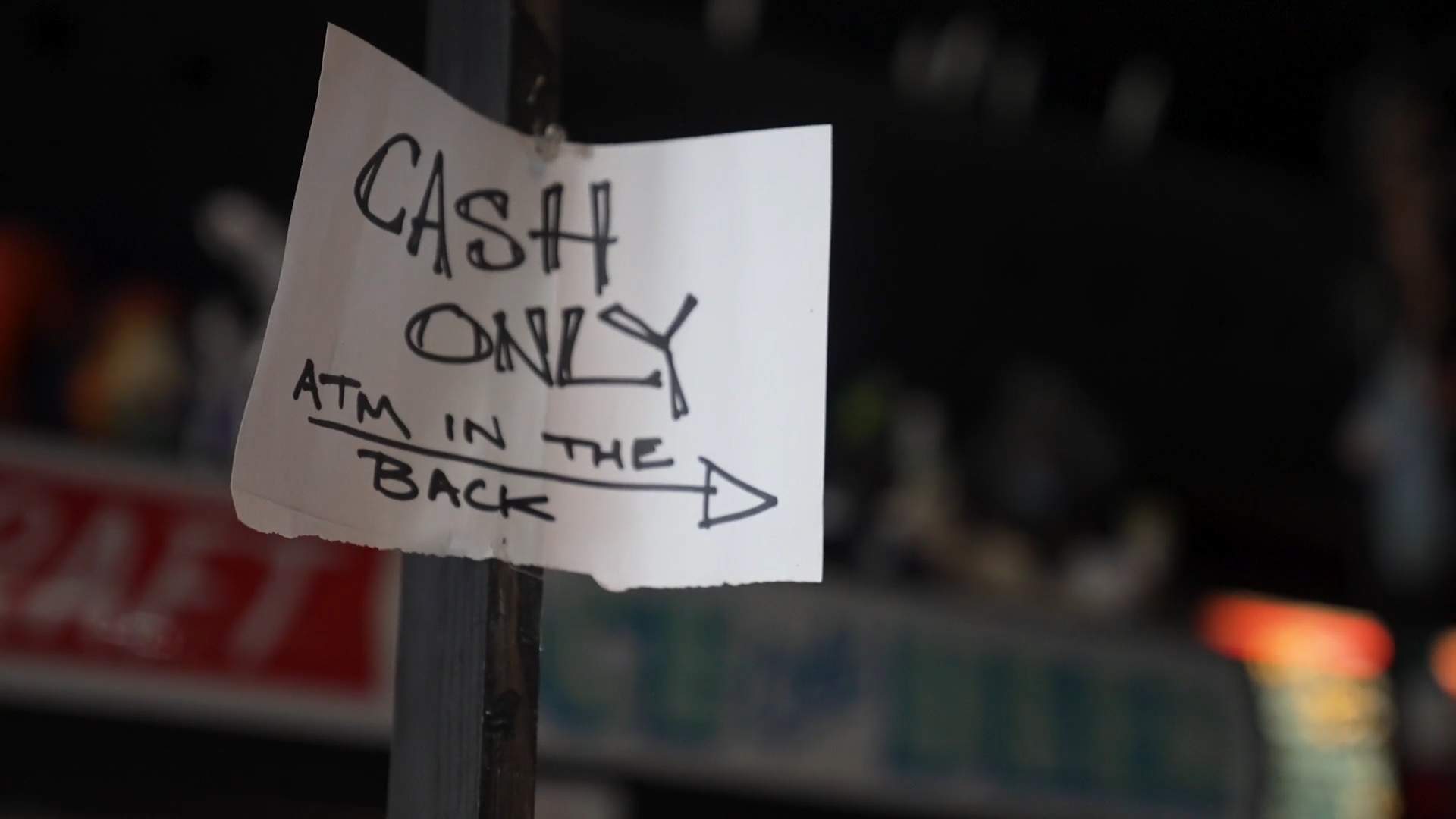

But, not everyone is jumping on the cashless bandwagon.

“We’re cash only,” says Abra Shiner, owner of Swan Dive, a proudly cash-only bar in Toronto.

“We’ve been cash only since the beginning. We had to start accepting square reader card payments for a while during the pandemic because people were so afraid of cash. But we got rid of that about as quickly as we could. It’s really inconvenient.”

Shiner says accepting only cash is more convenient for the bar because it makes the paperwork easier to do, it’s quicker to divide tips between employees, and cash actually saves her money.

“When people want to use a card to pay … that costs the business money,” she says. “So every time you go to a restaurant and pay with your card, that business is losing money.”

Starting in October, Canadian businesses have the option to pass on some of those credit card fees to customers as a result of a class action settlement.

So, what happens if you try to pay with plastic at Swan Dive?

“We do have this ATM in the back that people use. It’s for when they walk in without cash on them,” Shiner says. “If you have an ATM, you can own one yourself or you can have a profit-share agreement like I do. And so every time someone uses the ATM, you’re supporting two small businesses. We make some money and the ATM provider makes some money.”

According to the Canadian Bankers Association, there are nearly 70,000 ABMs in Canada, with banks owning about 18,515 of them. And even though 92 per cent of Canadians are happy with the technology, only eight per cent of Canadians use them today. That’s compared with 40 per cent almost 20 years ago.

Shiner adds that even though Canadians are embracing a cashless existence, there are still a lot of businesses that rely on cold, hard cash.

“The cafe down the street is still cash only. The liquor and lounge across the street, they’re cash only. The barber shop where I get my haircut, she’s cash only,” she says. “There are a lot of cash-only places.”

At the end of the day, Shiner says she’s not against adapting; it just doesn’t concern her.

“It just isn’t necessary right now. It doesn’t affect us. We’re in a community that is very cash based.”

But it’s not just about buying things. There’s another reason Canadians can’t quite kick cash.

“The other way that we use cash is as a store of value to store wealth, to save money,” says Josh Nye, a senior economist at RBC in Toronto.

In a report, Nye wrote that even though cash transactions are declining, demand for cash was at its highest level in 60 years. Nye adds the reason why Canadians stash cash during tumultuous times is because it provides a sense of comfort and security.

“Think back to … the Y2K bug toward the end of the last century … — the global financial crisis, particularly in the U.S., where there were greater concerns about the solvency of banks. People were withdrawing cash ahead of that. And of course, during the pandemic, in the early stages in 2020, we saw a real spike in cash withdrawals in demand for currency.”

Meaning, Canadians are hoarding cash in times of crises, whether perceived or real, especially larger bank notes like $50s and $100s.

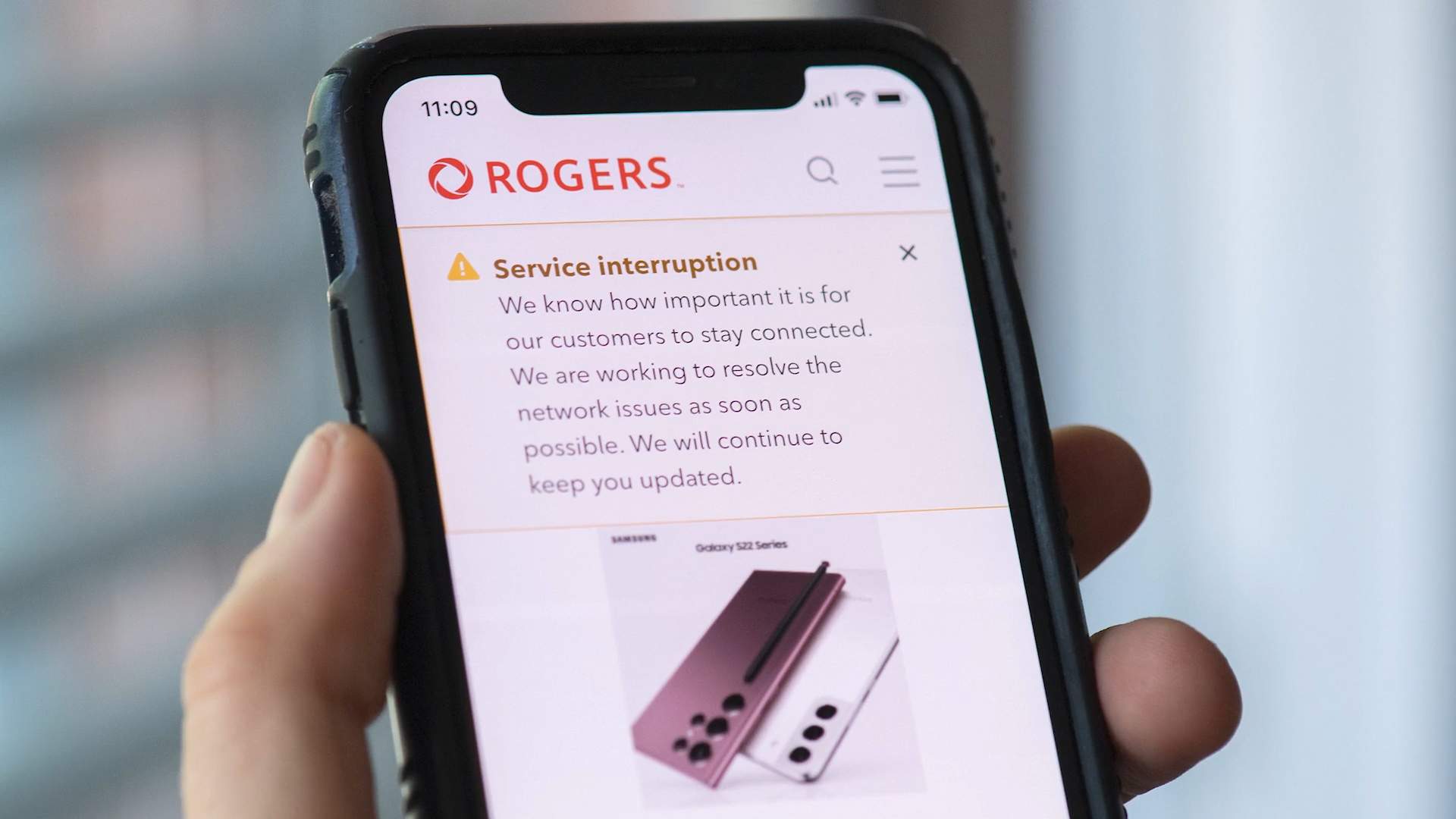

“It protects against things like cyber vulnerabilities, potential power outages, telecom outages like we saw this summer. There’s some safety that’s afforded by having access to physical cash.”

Global News learned that there was a spike in cash withdrawals following the country-wide Rogers outage in July.

Although experts like Nye believe Canada is still a long way from becoming a truly cashless society, there’s still talk of new currencies and services, such as micro-payments, buy now pay later, crypto or even central bank digital currencies, which our central bank, the Bank of Canada, is studying.

So as we move toward a more digital and convenient future, physical cash has not lost its appeal but its role is still unknown in an increasingly cashless world.

Comments

Comments closed.

Due to the sensitive and/or legal subject matter of some of the content on globalnews.ca, we reserve the ability to disable comments from time to time.

Please see our Commenting Policy for more.