The futuristic flying car we once imagined from The Jetsons may not be a reality, but self-driving cars are steadily making their way onto North American roads.

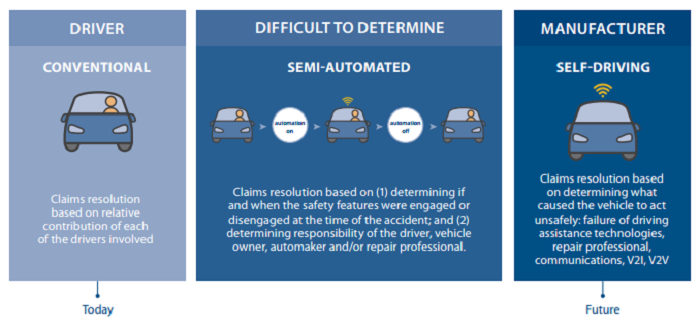

Though fully autonomous vehicles aren’t street legal in Canada, insurance companies are already grappling with the idea of how the technology will change the auto insurance industry. After all, who will be held accountable when a self-driving car crashes – the manufacturer, the driver, or both?

READ MORE: Self-driving cars are almost here, but are Canadians ready to take the wheel?

This week, a draft vehicle technology bill was tabled by the U.K. government suggesting that self-driving cars and their manufacturers should be liable for accidents, not the person sitting behind the wheel. The bill, which has yet to be debated, recommends that insurance companies offer two types of insurance for autonomous cars; one for when the car is operating on its own, and another for when the driver takes over.

WATCH: The era of self-driving cars is quickly appearing on the horizon, but not everyone is ready to give up the control

In the event the car crashed in self-driving mode as a result of a malfunction, the bill suggests the insurance company should be able to go after the car manufacturer to cover the cost.

“It is possible that the first few cases will go to court though over time we expect insurers and manufacturers will develop processes to handle subrogated claims quickly and easily,” reads the bill.

The draft bill also adds insurance companies would be exempt from paying up if the driver made unauthorized changes to the car’s software, or failed to update the software.

READ MORE: Driverless cars in Canada: What they are and how they work

Canadian insurance companies and industry experts are also keeping a close eye on the development of this technology, but most questions about liability remain unanswered.

“The evolution of autonomous vehicle technology is something we are certainly watching,” said John Bordignon, director of media relations at State Farm Canada.

Bordignon admitted that emerging technologies will pose many challenges for industry as the responsibility for accidents shifts from the driver to a hybrid of driver error and vehicle or software failure.

He said insurers will need to answer whether the manufacturer will be held accountable for vehicle failure, whether insurance companies will be allowed to access information from on-board computers to determine liability and how costs should be shared when driver error and software failure are both contributors to a crash.

“The industry will need to develop the right products and educate our customers about the correlation between the price of insurance coverage, claims costs and how that impacts insurance rates,” Bordignon added.

READ MORE: Canadians lack interest in self-driving cars, especially if they can’t drink and drive

Transport Canada, responsible for safety standards and the regulation of self-driving car technology, directed our questions to the Insurance Bureau of Canada.

Andrew Mcgrath, spokesperson for the Insurance Bureau of Canada, noted that while testing is underway in Canada, a functional driverless car is “a ways out on the horizon,” adding “insurers will need to assess the risks and determine products and pricing based on those risks.”

Similarly, the Insurance Corporation of B.C noted that if the law were to allow self-driving cars on public roads it would need to adapt insurance products to match the technology.

A 2016 report by the Insurance Institute of Canada also noted the industry will need to answer questions of liability when it comes to semi-autonomous and fully autonomous cars.

But the insurance industry still has time to come up with a plan – the Institute of Electrical and Electronics Engineers estimate it will take until 2040 for autonomous vehicles to make up 75 per cent of vehicle traffic. Ford has plans to debut fully driverless vehicles to consumers by 2021.

And, although Google has been testing its driverless cars on roads in California for over a year, Ontario recently launched a 10-year pilot project aimed at testing the safety of automated vehicles on public roads.

READ MORE: Ontario monitoring U.S. investigation into fatal collision involving driverless car

But consumers are already driving vehicles with dozens of technological safety features, from sensors and cameras designed to warn drivers of potential collisions, to automatic braking systems, which have also affected the insurance industry.

“When a vehicle equipped with such technology is damaged it costs more to fix. A bumper replacement five years ago cost the insurance company less to replace, however some bumpers today come with cameras and sensors that are very expensive,” said Bordignon.

“Costs for the insurance company rise, so the impact of vehicle automation on insurance claims costs and industry revenues are just now beginning to emerge and we continue to adjust our products and services to this new reality.”

State Farm insurance does not yet offer discounts on vehicles with these semi-automated safety features; however, Bordignon said the company is in the process of reviewing them.

Aviva Canada recently announced it would provide a 15 per cent discount for drivers of vehicles that have automatic emergency braking (AEB), citing a break in potential repair costs.

“It’s simple – our customers who choose vehicles with features that help prevent collisions, or reduce their impact, will pay less for their insurance coverage,” said Jason Storah, executive vice president of broker distribution for Aviva.

- Enter at your own risk: New home security camera aims paintballs at intruders

- Boston Dynamics unveils ‘creepy’ new fully electric humanoid robot

- Ontario First Nation calls for chemical plant to be shut down amid ‘dangerously high’ benzene levels

- Nova Scotia scraps spring bear hunt idea, public ‘very divided’ on issue

Comments