Debts are once again climbing among Canadian households, thanks to our booming housing market.

Canadians borrowed more than $27 billion in the three months up to the end of September, “principally” on new home loans as real estate prices raced higher, Statistics Canada says.

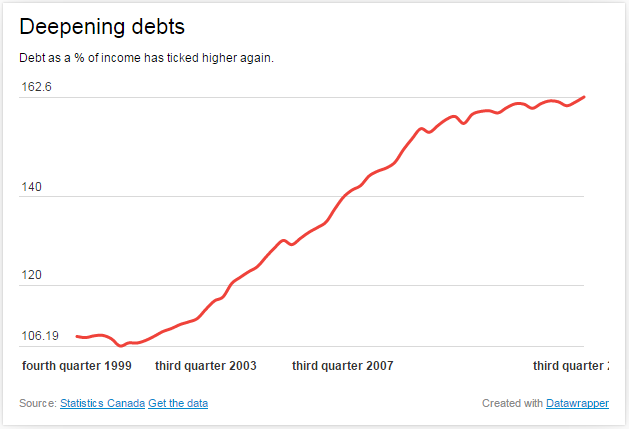

“Disposable income increased at a slower rate,” the federal statistics agency said, with debt again making up the difference.

Statistics Canada said Monday total borrowing rose 1.5 per cent. As a result, the amount of money collectively owed by Canadian households versus what we take home – the closely watched debt-to-income ratio – ticked to a new record high.

Following a big run-up dating back to before the recession, that ratio had been trending sideways in recent quarters, with economy watchers holding out hope that the gap would narrow.

It hasn’t. “Household debt risks are heating up once again,” TD economist Leslie Preston said.

- Michael Kovrig reflects on ‘brutally hard’ Chinese detention: ‘You’re totally alone’

- U.S. moves to ban Chinese software, hardware from all vehicles in America

- After controversial directive, Quebec now says anglophones have right to English health services

- Something’s fishy: 1 in 5 seafood products are mislabelled, study finds

Mortgage debt climbed 1.8 per cent to $1.17 trillion in the third quarter, while burdens built up on credit cards and other forms of non-mortgage debt, such as auto loans, ticked 0.9 per cent higher, to $515 billion.

Get weekly money news

On the upside, booming stock markets have (until recently) helped lift Canadians’ net worth by a “healthy” 2.8 per cent, Statscan said. But with oil’s crash leading markets lower, many households are poised to see a dip in net worth.

MORE: Here’s what’s keeping Canada’s central bankers up at night

Yet overall elevated debt levels remain a bigger worry. “More concerning in the rising level of household indebtedness after a period where it had seemed to plateau,” Preston said.

With oil prices still in freefall, economic growth is expected to take a hit across Canada next year, notably in energy reliant regions like Alberta.

Experts are torn about whether the gains from cheaper oil – inexpensive gas, better prospects for manufacturers – will offset the downsides. Most experts — including the Bank of Canada — are shaving their growth expectations for 2015.

Canada vs. US

Canadian households are now among the most indebted in the world – standing in stark contrast to U.S. households, who continue to pay down what the owe and keep overall leverage in check.

A report from the U.S. Federal Reserve last week showed debt burdens in the United States have fallen to their lowest level in over a decade, putting that country’s economy on stronger footing heading into 2015.

The report highlighted the indebtedness of several countries including Japan, France, Germany and Italy. Tops among most indebted households: Canadians.

Revised down

The Fed’s report said Canada’s debt-to-income ratio stood at 167 per cent, meaning for every dollar in income brought home, Canadians owed $1.67. Statistics Canada’s ratio on Monday stood at 162.6 per cent.

While a fresh high, the reading would have been higher had Statscan relied on values it had been using in previous national balance sheet reports. The ratio was revised downward as part of the agency’s “annual revision process,” Statscan explained.

“The revision was due to new information received that led to a downward revision to the value of mortgages owed by households.”

Comments