Recent condo buyers in Toronto should perhaps be thankful for the often maddening delays they’ve faced on the completion of their unit – it’s helped stave off a potentially sharp correction in the value of their condo.

That’s one half of a narrative painted by a new report published Tuesday on the state of the country’s closely watched condo market where fears of a bubble hover over some bigger cities.

According to national real estate firm Royal LePage, “bottlenecks” in construction in markets like Toronto, Montreal and Vancouver have kept the number of completed towers in check in recent years despite a surge in demand from investors and first-time buyers.

READ MORE: Paying for the boom, an in-depth look at some big city real estate markets

Royal LePage expects the market to swing at least somewhat into buyer’s territory in markets like Toronto, as new units come up for sale.

The influx will create some “turbulence” in the months and quarters ahead, the report suggested, which could impact prices.

Urbanation, a market researcher in Toronto, expects the city will see 20,000 new units come onto the market next year. That number contrasts with the historical norm of about 14,500 new units a year added to the country’s biggest condo market between 2008 and 2012, according to Royal LePage.

“If you look at what’s coming on stream, there will be a short term of oversupply,” Phil Soper, president of Royal LePage said in an interview.

The report suggests the downturn will last about two years, though Soper said he didn’t anticipate prices falling.

“The developers have to be responsive… in the short term when there’s an oversupply, you’d expect some of the builders to adjust their prices — hold them firm I should say,” he said.

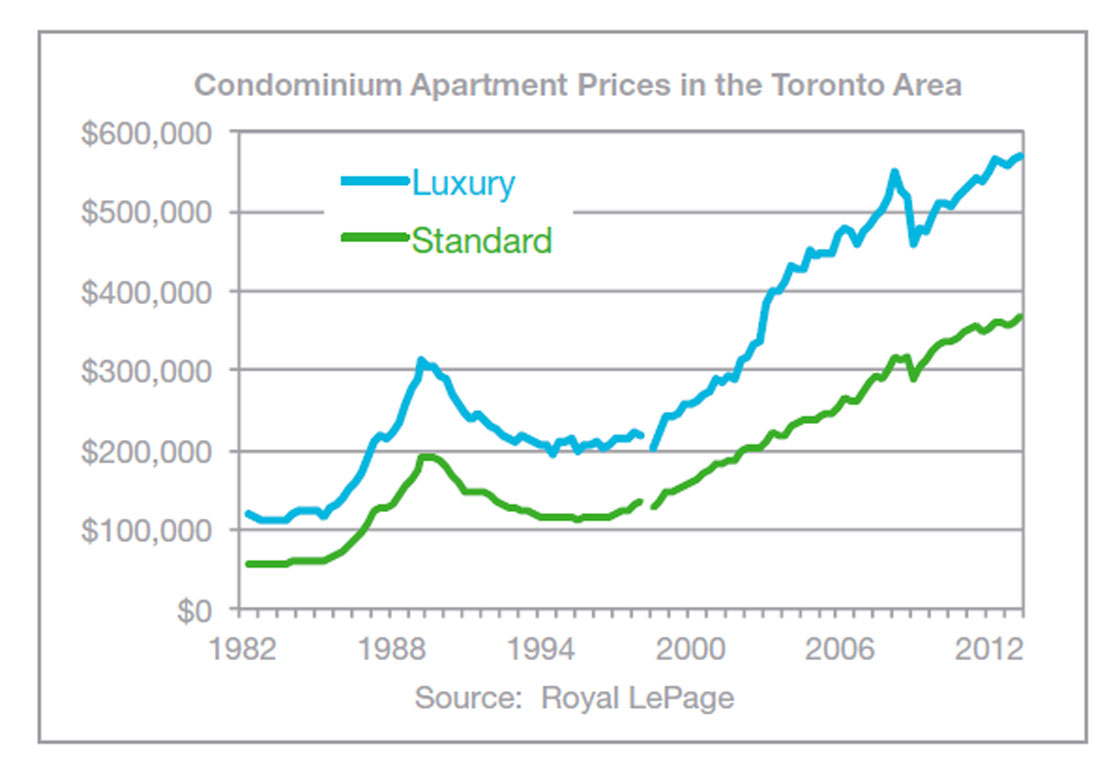

Condo prices in Toronto have appreciated about five per cent a year over the last couple of decades, industry figures show. Similar gains have been posted in Canada’s other two large condo markets of Montreal and Vancouver.

Investors won’t be able to bank on that kind of growth going forward, Soper said. “There isn’t going to be any firesales on condominiums but I don’t expect typical price appreciation in the condominium sector over the next couple of years.”

The excess supply will partially be picked up by demographic shifts, according to Royal LePage – the second half of the report’s market narrative.

Echo boomers unwilling to sacrifice hours a day commuting but unable to afford a house in the city will pick up some of the slack, as will new immigrants already accustomed to living in more densely-populated urban areas, the report suggests.

A joint report from the Pembina Institute and RBC published this week suggests younger echo boomers and millenials will shun more affordable housing in the outer reaches of the Greater Toronto Area for closer proximity to work.

“They’re not going to want to buy a house in the distant suburbs and drive two hours every day,” Cherise Burda, Ontario director for the Pembina Institute and the report’s author, said.

The Toronto Board of Trade estimates average commute times hover around 66 minutes in the GTA – putting the region at No.2 on the continent behind only New York City.

TD Bank suggests the gridlock costs the region $6 billion in lost productivity annually, a figure that jumps to as much as $15 billion by 2031 if the sprawl continues.

The Pembina Institute is calling for the Ontario government to implement new legislation that would incent developers to construct “mid-rise” developments that offer young families or second-time buyers an alternative between the suburban single-family home or a potentially cramped condo life.

READ MORE: Map — Torontonians living far from transit, and without a car

As the market cools and builders rein in projects, however, such developments appear years away at least.

“They want to time their new projects to come on stream when they can sell their inventory,” Soper said. “They don’t want to sell at below market price.”

Comments