When we visited Ellisa Atherton’s living room in Ajax, Ont., in early March, it was crammed – wall to wall to wall to wall – with boxes.

In the middle of the room, walled in by boxes, was the family’s Christmas tree – Atherton had put it up so it could be a ‘real Christmas’ for her youngest child, despite everything that was going on. But the room was too tightly packed for her to take it down again, so as winter turned into spring outside, there it stood.

Faced with losing the house that she had only moved into in the fall, she didn’t feel she could open the boxes and really move in.

“I can’t unpack because of the uncertainty,” she says. “I’ve been here for six months, and I can’t even call this a home.”

READ MORE: Staggering share of Canadians fear bankruptcy if interest rates rise much more

Atherton bought the house for $655,000 with a $55,000 down payment. Monthly payments of $6,000 with a mortgage rate of 11.99 per cent weren’t sustainable, but she was hoping to cut that sharply by refinancing after she moved in.

But it didn’t work out that way, and her dream of homeownership is mired in a lawsuit and a series of what she calls inflated and unexpected fees that she can’t afford. Without a lower rate, she says, she’ll lose the house to foreclosure.

She calls the situation.” … Hell, hell, hell. Depression, tears – it’s an ordeal that no one should have to go through.”

As the census showed us last fall, hundreds of thousands of Canadians painfully stretch their budgets every month to keep up with housing costs.

The census revealed that just under half a million Canadian households with mortgages spend over 50 per cent of their household incomes on shelter costs – taxes and utilities, but also mortgage payments.

WATCH: Canadians with mortgages teetering on trouble. Sean O’Shea reports.

If households are that stressed, how will they cope when interest rates push their mortgage payments higher?

Experts are not optimistic. The answers are bleak: lose the home, or severely cut spending.

It’s not surprising where homeowners are spending more than 50 per cent of their pre-tax income on shelter costs. Stressed households are concentrated in cities where real estate is most expensive – Toronto and Vancouver, but also noticeably in Barrie, Hamilton and Victoria.

Most other Canadian communities are below 8 per cent.

“The old guideline was about 30 per cent. Even if you make that 35 or 40, you’re seeing people with 10 or 20 per cent more than that,” Toronto-based insolvency administrator Scott Terrio says of his clients.

“It’s pretty scary.”

Low rates and rising real estate prices have let some homeowners get away with high debt levels – so far.

“But with interest rates rising now, and toughening mortgage rules in effect, I don’t think homeowners will be so lucky in the coming few years,” says economist David Madani of Capital Economics.

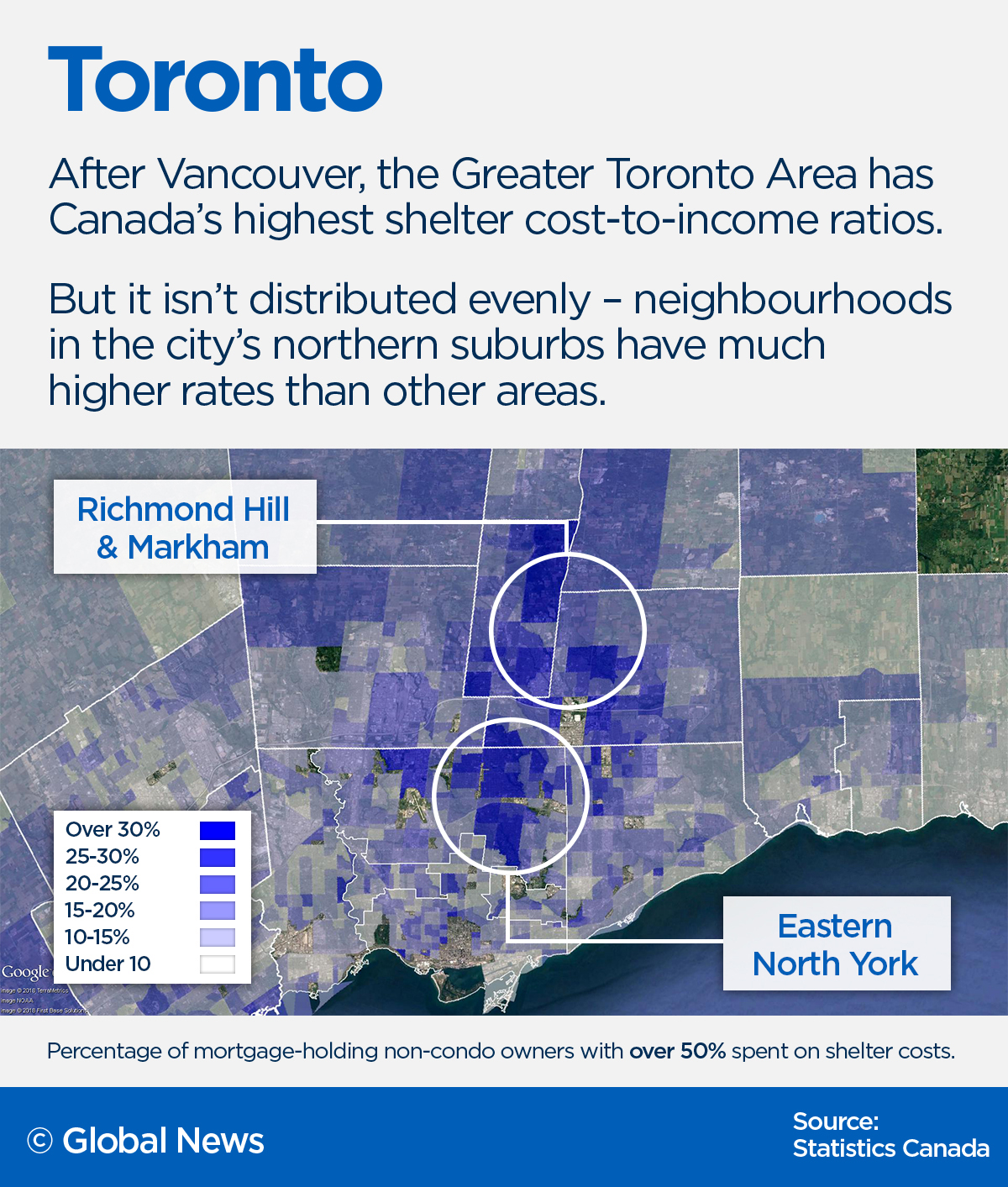

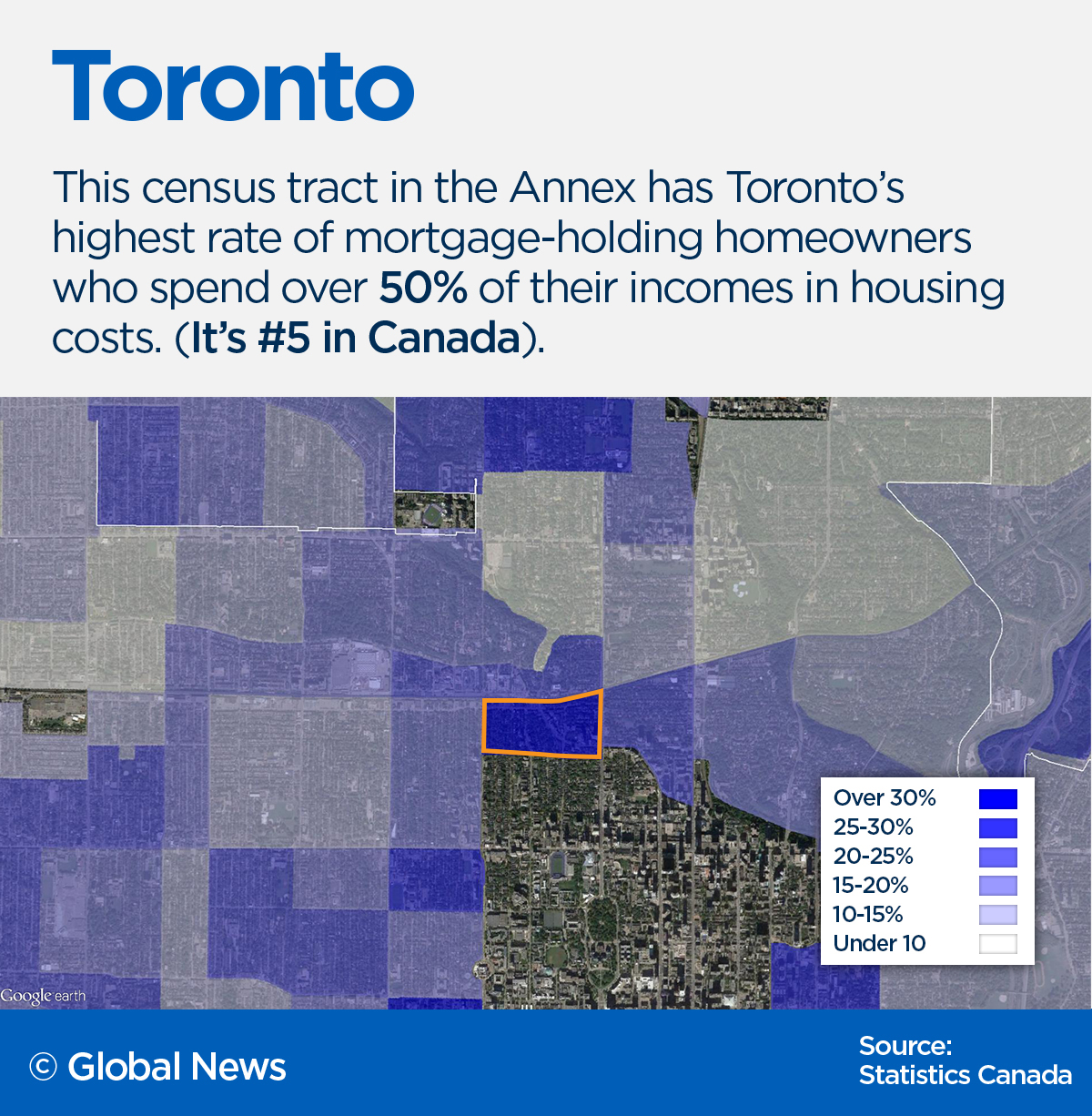

Within Toronto and Vancouver, they are clustered in specific neighbourhoods.

In Toronto, there is a strong concentration of overextended homeowners near western North York and Markham, and part of northwest Scarborough.

In Toronto, mortgage broker Ron Alphonso thinks the trouble could come from homeowners who invested heavily in their properties – often tearing down modest houses to build big ones – because they counted on values continuing to rise.

“When house prices are flat, knocking down a little house and putting up a mansion is not a good idea. They primarily did it to invest and make more money – no longer a good idea.”

“Unfortunately, it looks like the worst-case scenario might happen, and a lot of their properties will go down dramatically in value, their mortgages will remain high, and they’re going to have some serious financial problems.”

The Toronto map reflects areas that have seen many houses heavily renovated, or torn down and rebuilt, in recent years.

WATCH: Greater Toronto Area home foreclosures on the rise

In a less inflated housing market, it’s an interesting question what would happen to a glut of new large houses that have more sellers than buyers.

“All these people putting these big houses up for sale for one, two, three million, anyone that has to get a mortgage can no longer afford them. There’s not enough people with enough money to buy these big houses. What’s going to happen to them? They’re going to fall in value.”

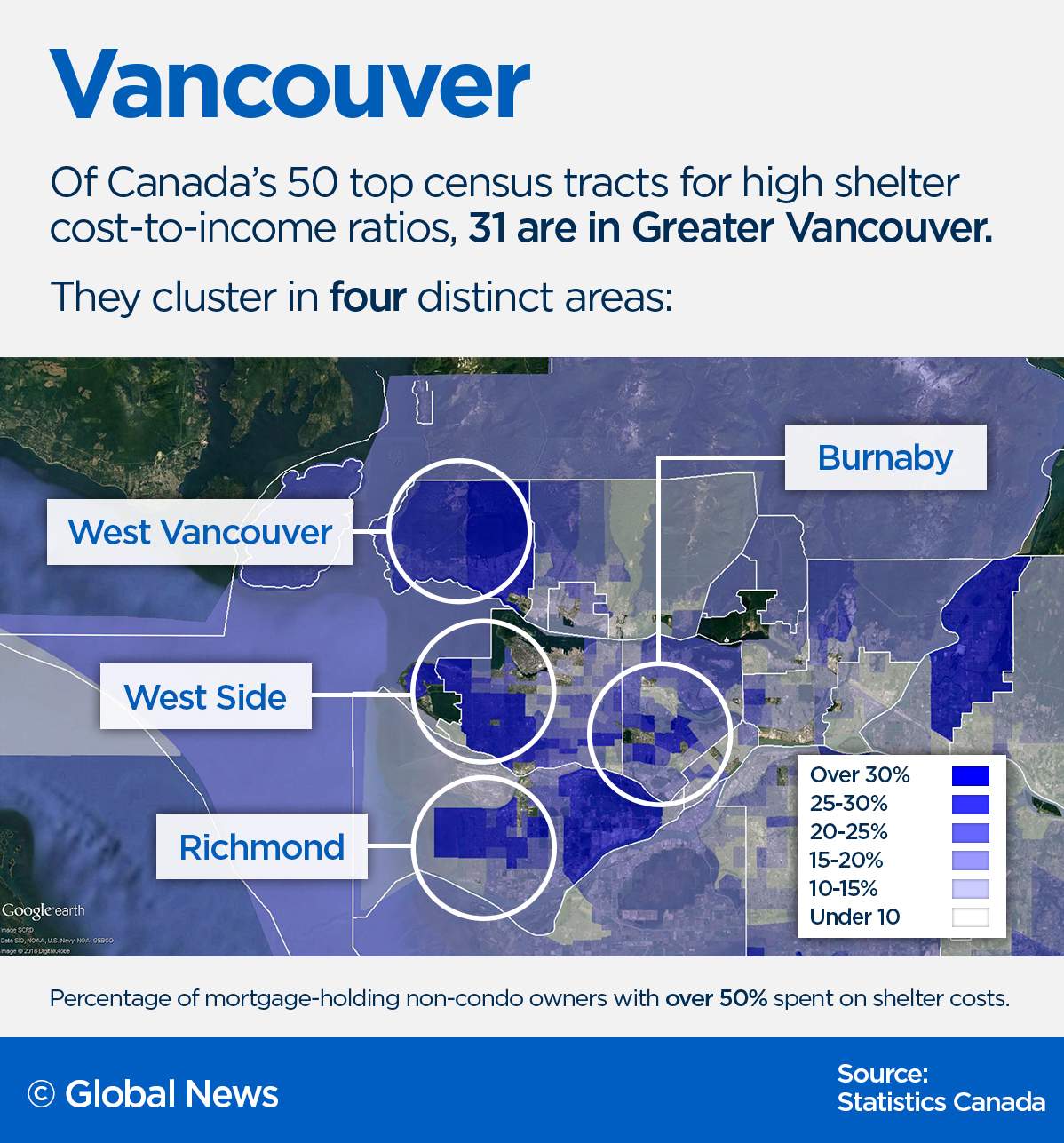

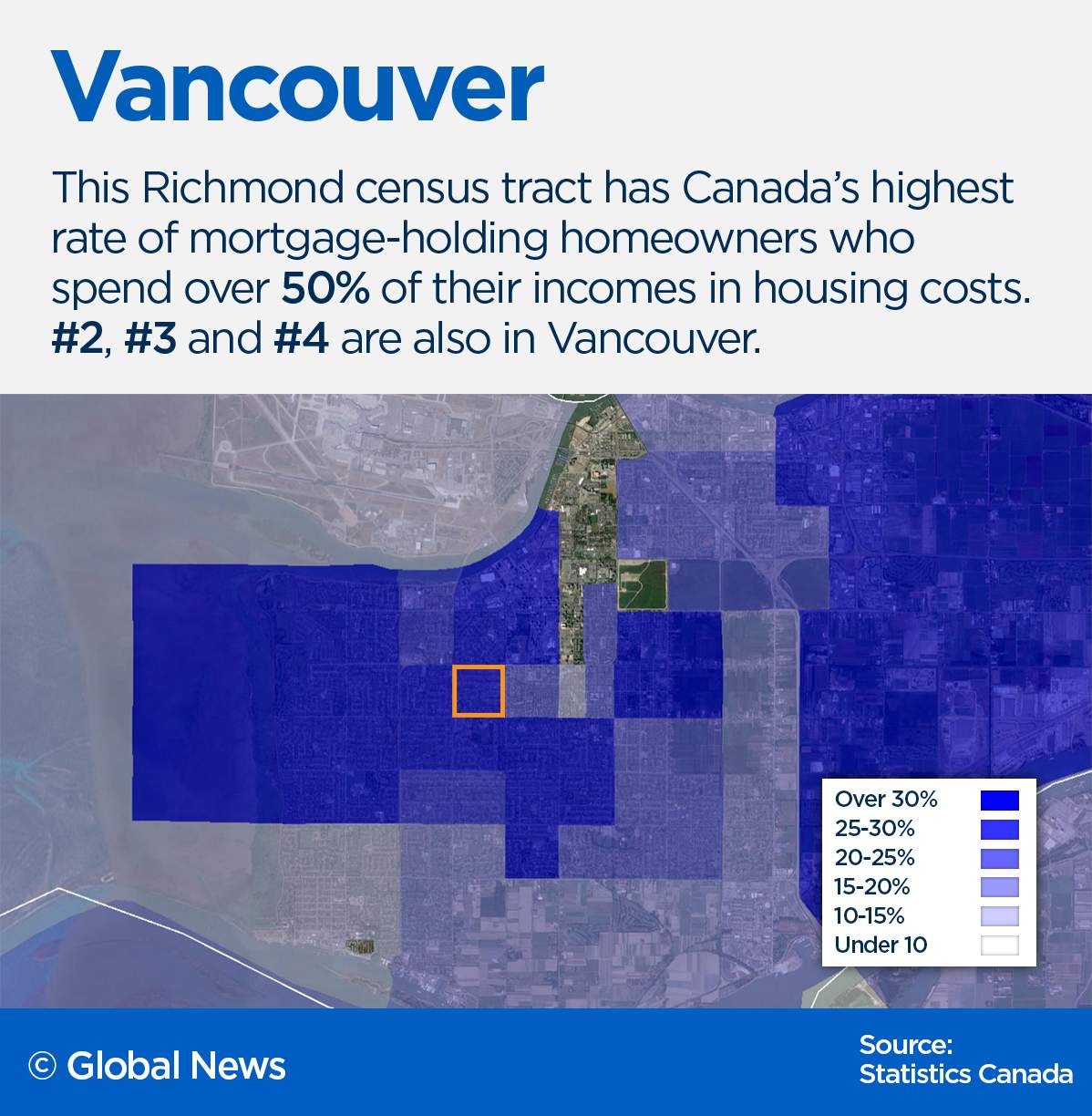

The census tracts with the highest number of households with very high shelter cost-to-income ratios are in the Vancouver area.

Of Canada’s 50 top census tracts for high shelter cost-to-income ratios, 31 are in Greater Vancouver.

In Vancouver, three areas stand out: parts of West Vancouver, Shaughnessy and Kerrisdale, and Richmond.

“When we talk about concern about rising interest rates, it’s most pronounced in British Columbia, compared to other parts of the country,” says Vancouver-based insolvency trustee Lana Gilbertson. “And that doesn’t surprise me, given the cost of housing.”

A recent Ipsos poll showed that British Columbians are edgier about their finances than people in the rest of the country.

They were more likely to be concerned about rising interest rates than Canadians in other regions (48 per cent, against 46 per cent in Saskatchewan and Manitoba and 45 per cent in Ontario).

WATCH: A local financial advisor says a rising number of Okanagan residents are drowning in debt and even the slightest rise in interest rates could take a big toll on people paying off large loans, like mortgages.

And British Columbians were less confident in their ability to cope financially if they had to stop working for three months, deal with the death of an immediate family member, or pay a substantial education bill.

“I think in British Columbia there’s a lot of nervousness about this, especially in Vancouver,” she says.

“I think in the very worst-case scenario, if we saw, for example, a significant downturn in home prices, and borrowers are faced with being underwater, they could be looking at bankruptcy.”

In late January, the Canada Mortgage and Housing Corporation warned of a “high degree of vulnerability (in) Victoria, Vancouver, Hamilton and Toronto because of the detection of price acceleration and strong evidence of overvaluation.” In Toronto, the CMHC wrote that home prices ” … still remain above rates justified by economic and demographic fundamentals such as income and population growth and continue to signal a high degree of vulnerability.”

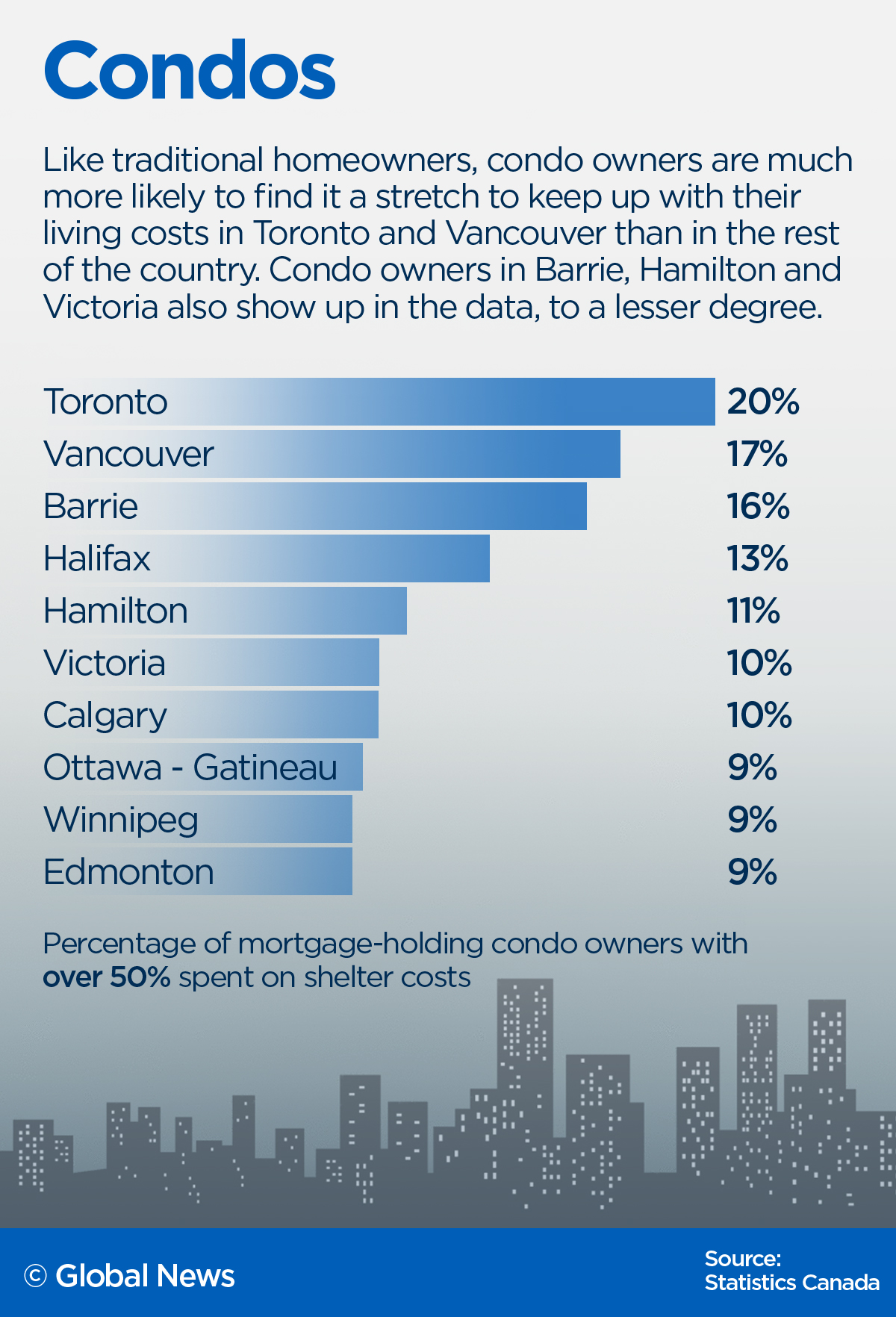

Condo owners show a similar pattern: over 20 per cent of Toronto condo owners and over 17 per cent in Vancouver pay more than 50 per cent of their incomes in housing costs, as opposed to 10 per cent or lower in Winnipeg, Calgary and Edmonton. Barrie, Hamilton and Victoria have rates above 10 per cent.

Other homeowners could respond to being squeezed by severely cutting back other expenses to keep their homes. Terrio sees homeowners who meet this profile:

“People will do everything to make that payment, and everything else is meant to be at the expense of that.”

“You can’t believe the lengths they go to. The last thing they’ll do is not pay for their home.”

“When you get into situations where people are in a lot of trouble, don’t expect to see people missing their mortgage payments until they absolutely have to.”

At a certain point, though, their frugality starts to hurt the economy, Madani says.

“For some households … that could mean that they have a bit less money to spend on other goods and services in the economy, assuming that they’re going to stay in their home, which I’m assuming most Canadians will. That could have some sort of negative side effects for the broader economy, if there’s less spending on goods and services.”

WATCH: With the average GTA home price around $1 million, a mortgage broker says he’s seeing more couples having a hard time paying the monthly bills.

Rate hikes would affect people with variable-rate mortgages first, but fixed-rate mortgages soon enough, Gilbertson says.

“Anyone who’s carrying a variable-rate mortgage will feel the effects immediately, but let’s face it – most people have no more than a five-year term, so even if you’re fixed, you’re going to have to deal with it whenever your mortgage comes up for renewal.”

In one simulation we set up, each 1 per cent rise in interest rates meant about a $400 monthly hike in mortgage payments.

In the census data, the income side is taken from tax data. That means that undeclared income that isn’t captured by the tax system isn’t visible in the statistics.

On paper, there’s a case for moving somewhere where housing is more affordable. The problem, Terrio says, is that homeowners can be professionally trapped in one or two large cities, especially if they are a couple who both have to find jobs in their fields.

“There are a whole bunch of industries where people aren’t making great money, but they’ve got to be in the city if they want to stay in that industry,” he says.

“I don’t think people are being paid higher amounts of income in Toronto or Vancouver, necessarily.”

Comments

Want to discuss? Please read our Commenting Policy first.