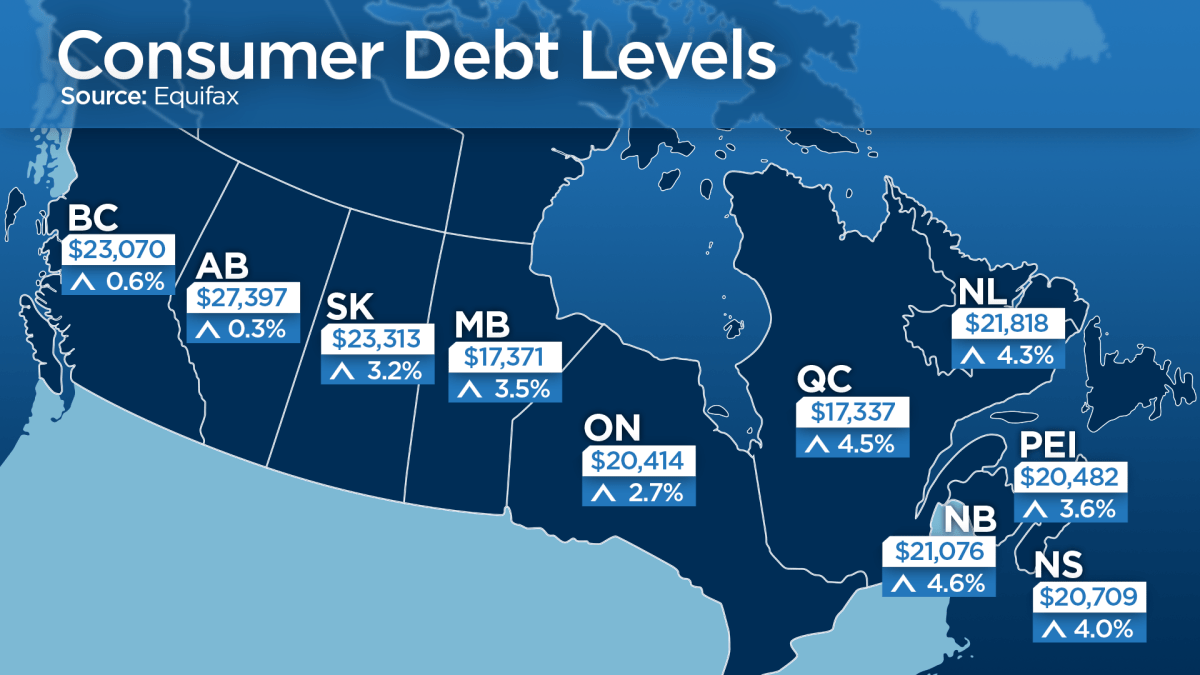

At more than $27,000 per person, Albertans have the highest levels of consumer debt in the country.

Yet there’s little danger at present of them defaulting on car loans or other outstanding credit as a result of oil’s collapse and the economic consequences that holds for the province, the head of Royal Bank of Canada said Wednesday.

“There is an ability to manage through the next year,” Dave McKay, chief executive of RBC, said.

The bank, one of the biggest lenders in the country, has nearly a quarter of its Canadian loans held by Albertans, from homeowners with mortgages to big oil firms who’ve borrowed to expand energy projects.

RBC’s outlook is for oil to hover as low $45 a barrel this year. Crude prices were trading down 1.25 per cent in New York on Wednesday, to $45.31 a barrel – a 57 per cent plunge from their June high.

Before the price collapse, Alberta — the country’s fastest-growing economy in recent years — was “overheating” in some respects, McKay said. There are some benefits to low oil taking some steam out of certain areas, such as the housing market.

MORE: Housing prices in Calgary poised to moderate

That said, the longer oil prices remain low, the more likely investment will dwindle in the oil patch, jobs will be shed and the economy will tip into recession. “It’s what is the price six to twelve months from now” that’s a concern, McKay said.

- What is a halal mortgage? How interest-free home financing works in Canada

- Ontario doctors offer solutions to help address shortage of family physicians

- Capital gains changes are ‘really fair,’ Freeland says, as doctors cry foul

- Budget 2024 failed to spark ‘political reboot’ for Liberals, polling suggests

A report from the Conference Board of Canada said a day earlier Alberta, which accounted for one in three new jobs in Canada in 2014, will contract this year – an outlook Alberta Premier Jim Prentice disputed.

Stress tests

McKay said RBC has “stress tested” its balance sheet against worst-case scenarios for the province and beyond, where job losses pile up and home prices drop dramatically. RBC will be fine even if those scenarios come to fruition, McKay said.

But he doesn’t see those outcomes happening. “We don’t see any signals right now” to be worried about, he told an investor conference.

On Tuesday, Suncor Energy Inc. announced it is cutting $1 billion from spending plans this year, as well hundreds of millions in operating costs over the next couple of years. As part of the plan, 1,000 jobs will be cut.

MORE: Suncor cuts 1,000 jobs, scales back spending plans

A day earlier, Calgary-based Canadian Natural Resources announced it was scaling back spending by $2.4 billion. Other major producers such as Cenovus and Husky Energy have also recently announced reduced capital budgets.

Energy sector experts say they will have a better indication of how low prices will affect the industry by the beginning of the next drilling season in late summer.

Consumer debt

Albertans hold highest average debt levels on credit cards, lines of credit and auto loans in the country at above $27,000 per capita, according to Equifax.

MORE: MAP — Debt levels highest in Western Canada

Asked about whether he was concerned job losses are affecting consumers’ abilities to repay those loans, McKay said the bank had monitoring mechanisms in place to help customers before they get into trouble.

“Sometimes it’s a year before a missed payment,” the executive said. “We have up to a year’s notice and we reach out to them” to develop a new repayment plan, he said.

Auto loans are one area of concern, though, according to McKay. “They’re backed by a depreciating asset … You’ve got to watch that portfolio very carefully,” he said.

Comments